- Copper Quest focus: Copper Quest Exploration Inc. (CSE: CQX / OTCQB: IMIMF / FRA: 3MX) recently traded around CA$0.09–CA$0.11, with a micro-cap valuation roughly in the CA$9M–CA$14M range.

- Sector catalyst: S&P Global projects copper demand rising from 28M metric tons in 2025 to 42M by 2040, while the IEA warns the mine project pipeline could leave a ~30% supply shortfall by 2035.

- Investor angle: CQX is far earlier and riskier than TGB, CS, HBM, and TMQ, but its valuation gives it more torque if drilling at Rip or follow-up work across its copper portfolio delivers stronger exploration results.

Copper is becoming one of the most important metals in the market because it sits at the center of electrification, grid upgrades, EVs, renewable energy, AI data centers, industrial automation, and defense infrastructure. The metal is not a futuristic concept. It is already essential to wiring, motors, power systems, construction, and high-voltage networks.

For investors, the copper trade is not just about the metal price. The better question is which companies have leverage to copper demand, enough project quality to matter, and a realistic path to value creation. That is why this watchlist combines one micro-cap explorer, Copper Quest Exploration, with four larger copper-linked names: Taseko Mines, Capstone Copper, Hudbay Minerals, and Trilogy Metals.

Market Catalyst: Copper Demand Is Outrunning New Supply

The copper market is getting investor attention because the long-term demand curve is moving higher while new mine supply remains difficult to build. S&P Global projects copper demand will rise from 28M metric tons per year in 2025 to 42M metric tons by 2040, a 50% increase driven by electrification, AI data centers, grid investment, EVs, renewable energy, and defense systems.

The supply side is the bigger issue. The IEA has warned that the current copper mine project pipeline could fall roughly 30% short of 2035 demand, due to declining ore grades, long permitting timelines, rising capital costs, and limited new discoveries.

Two numbers show why this matters for investors:

- Copper demand could increase by roughly 14M metric tons per year by 2040, according to S&P Global, which is a major amount of new supply for an industry where large mines often take more than a decade to permit and build.

- S&P Global also estimates a potential 10M metric ton supply gap by 2040 without meaningful supply expansion, showing why new exploration and development assets can become more strategically valuable.

That matters for Copper Quest because early-stage explorers are one of the highest-risk but highest-leverage parts of the copper cycle. The risk is that exploration companies need capital, time, and drilling success before the market assigns real value. That makes the key metrics clear: drill results, land position, financing strength, share count, copper price, and follow-up exploration plans.

1. Copper Quest Exploration: The Micro-Cap Discovery Angle

Copper Quest Exploration Inc. (CSE: CQX / OTCQB: IMIMF / FRA: 3MX) is the smallest and most speculative stock in this basket. The company is focused on copper, molybdenum, and gold exploration across North America, with a project portfolio that includes Rip, STARS, Kitimat, Alpine, and other critical-mineral assets.

The latest catalyst is the company’s 2026 exploration plan, beginning with a minimum 2,000-metre drill program at the Rip Copper-Molybdenum Project in British Columbia. Copper Quest has an earn-in option for up to an 80% interest in Rip, a road-accessible porphyry copper-molybdenum project spanning roughly 4,700 hectares in the Bulkley Porphyry Belt.

- Investor data point: CQX has about 118.4M issued shares, roughly 54.2M reserved for issuance, and a micro-cap valuation that can move quickly if drilling produces stronger copper-molybdenum evidence.

The company’s broader portfolio adds to the story. Copper Quest says its North American critical-mineral land package includes 8 projects spanning more than 46,000 hectares. That gives CQX multiple shots at news flow, but investors should still treat it as an early-stage exploration story where results, financing, and dilution discipline matter.

2. Taseko Mines: Producing Copper Exposure

Taseko Mines (NYSE American: TGB / TSX: TKO) gives investors more direct copper exposure through production and development assets. Unlike Copper Quest, Taseko is not just an exploration story. It has operating exposure through Gibraltar and development upside through projects such as Florence Copper.

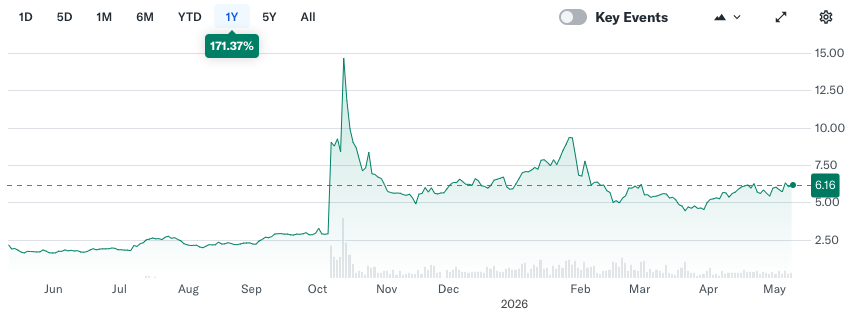

Recent market data showed TGB trading around US$6.90–US$7.40, with a market cap around US$2.5B–US$2.7B and a 52-week range of roughly US$1.89–US$9.25. The stock has already had a major move, showing how quickly copper producers can re-rate when the metal backdrop improves.

- Investor data point: TGB’s 52-week range shows strong copper-cycle torque, with the stock trading multiple times above its 52-week low during the recent copper rally.

The attraction is that Taseko gives investors copper production and project development leverage. The risk is that producers are still exposed to operating costs, permitting timelines, capex inflation, and copper-price volatility.

3. Capstone Copper: Scale and Operating Leverage

Capstone Copper (TSX: CS) is a larger copper producer with operating scale across the Americas. It gives investors a more established way to play copper demand than a micro-cap explorer, while still offering more copper sensitivity than diversified mining giants.

Recent market data showed CS trading around CA$12–CA$13, with a market cap around CA$9B–CA$10B and a 52-week range of roughly CA$6.43–CA$18.04. StockAnalysis data showed trailing revenue around US$3.46B, up about 38%, with net income of roughly US$593M.

- Investor data point: Capstone’s revenue base and operating leverage make it one of the cleaner mid-cap copper producer comparisons for investors who want scale rather than exploration risk.

Capstone matters because copper producers can benefit directly from higher realized prices and stronger margins. The risk is that the stock already reflects part of the copper bull case, and operating performance must keep supporting the valuation.

4. Hudbay Minerals: Growth Through Production and M&A

Hudbay Minerals (NYSE: HBM / TSX: HBM) has become one of the more closely watched copper-linked miners. The company has copper exposure across existing operations and a growing U.S. copper strategy, including its proposed acquisition of the remaining shares of Arizona Sonoran Copper Company.

Recent market data showed HBM trading around US$24–US$25, with a market cap near US$9B–US$10B and a 52-week range around US$7.94–US$28.74. A recent IBD update noted Hudbay posted 67% EPS growth in Q1 and 27% sales growth, while Reuters reported Hudbay’s Arizona Sonoran deal at about US$1.48B.

- Investor data point: HBM combines production exposure with M&A-driven growth, making it a more mature copper-cycle play than CQX but still more leveraged than diversified mega-miners.

Hudbay’s appeal is that it offers copper exposure with operating scale and a clearer production growth strategy. The risk is integration, project execution, copper-price sensitivity, and whether recent share-price strength already discounts much of the upside.

5. Trilogy Metals: The High-Beta Development Story

Trilogy Metals (NYSE American: TMQ / TSX: TMQ) is another high-beta copper-linked name, focused on mineral development in Alaska’s Ambler Mining District. It is not a producer, so the stock is more sensitive to project updates, permitting expectations, and investor sentiment toward future copper supply.

Recent market data showed TMQ trading around US$4.40–US$6.10, with a market cap in the roughly US$780M–US$870M range and a 52-week range of US$1.13–US$11.29. That wide range shows just how volatile development-stage copper names can be when sentiment shifts.

- Investor data point: TMQ’s 52-week range suggests strong upside torque but also major downside volatility, which is common for pre-production copper development stories.

Trilogy is useful as a comparison for Copper Quest because it shows how the market can assign larger valuations to copper development assets when the project scale becomes more defined. The risk is that development-stage assets require time, capital, permitting success, and strong commodity conditions.

Stock Snapshot

| Company | Ticker | Recent Price | Market Cap | Latest Key Number | Main Copper Angle |

|---|---|---|---|---|---|

| Copper Quest Exploration | CSE: CQX / OTCQB: IMIMF | ~CA$0.09–CA$0.11 | ~CA$9M–CA$14M | 2,000-metre Rip drill program | Micro-cap copper-moly exploration |

| Taseko Mines | NYSE American: TGB / TSX: TKO | ~US$6.90–US$7.40 | ~US$2.5B–US$2.7B | 52-week range: US$1.89–US$9.25 | Copper production and Florence Copper upside |

| Capstone Copper | TSX: CS | ~CA$12–CA$13 | ~CA$9B–CA$10B | Revenue TTM around US$3.46B | Mid-cap copper producer leverage |

| Hudbay Minerals | NYSE: HBM / TSX: HBM | ~US$24–US$25 | ~US$9B–US$10B | Q1 EPS +67%, sales +27% | Producer growth and U.S. copper M&A |

| Trilogy Metals | NYSE American: TMQ / TSX: TMQ | ~US$4.40–US$6.10 | ~US$780M–US$870M | 52-week range: US$1.13–US$11.29 | High-beta copper development |

Bottom Line

Copper Quest Exploration is the speculative micro-cap in this copper basket. CQX / IMIMF has a defined 2026 drill catalyst at Rip, a broader 46,000-hectare critical-mineral portfolio, and exposure to a copper market where demand could rise 50% by 2040.

The key watch items are simple: drill results, follow-up targets, financing discipline, and whether CQX can turn its land package into a more credible discovery story. If those pieces start to appear, Copper Quest could attract more attention as investors look for smaller copper names tied to the long-term supply gap.

This is sponsored content. Investors should conduct their own due diligence and consult a qualified financial advisor before making any investment decisions.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}