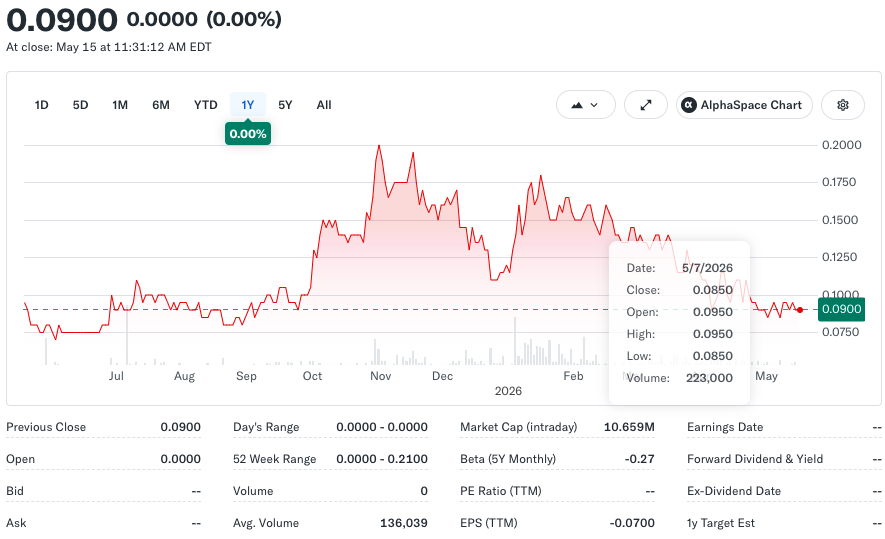

- Copper Quest focus: Copper Quest Exploration Inc. (CSE: CQX / OTCQB: IMIMF / FRA: 3MX) recently traded around CA$0.09, with market cap near CA$10.9M.

- Sector catalyst: S&P Global projects copper demand rising from 28M metric tons in 2025 to 42M by 2040, while the IEA warns of a potential 30% copper supply shortfall by 2035.

- Investor angle: Copper Quest is the speculative micro-cap explorer in this basket, while Taseko, Capstone, Hudbay, and Trilogy offer larger copper production or development exposure.

Copper is becoming one of the most important metals in the market because it sits at the center of electrification, grid upgrades, AI data centers, electric vehicles, renewable energy, industrial automation, and defense infrastructure. It is not just a construction metal anymore. Copper is increasingly being treated as a strategic input for the next phase of global infrastructure.

For investors, the copper trade is not only about today’s spot price. The more important question is which companies have leverage to a tightening copper market, enough project quality to matter, and a realistic path to value creation. That is why this watchlist combines one micro-cap explorer, Copper Quest Exploration (CQX / IMIMF), with four larger copper-linked names: Taseko Mines, Capstone Copper, Hudbay Minerals, and Trilogy Metals.

Market Catalyst: Copper Demand Is Rising Faster Than New Supply

The long-term copper thesis is built on a simple problem: demand is rising, but new supply is difficult to bring online. Large copper mines can take more than a decade to permit, finance, and build. At the same time, many older mines are facing declining grades, rising capital costs, water constraints, and political risk.

The numbers explain why investors keep coming back to the copper theme:

- S&P Global projects global copper demand rising from 28M metric tons in 2025 to 42M metric tons by 2040, a roughly 50% increase driven by electrification, AI data centers, power grids, EVs, defense, and industrial demand.

- The IEA has warned that the current copper mine project pipeline could fall around 30% short of projected 2035 demand, making exploration and development assets more important if the supply gap widens.

That backdrop does not make every copper stock attractive automatically. Producers still face cost inflation and operational risk, developers still need funding and permits, and explorers still need drill results. But it does create a stronger environment for companies with real copper exposure and credible project catalysts.

1. Copper Quest Exploration: The Micro-Cap Discovery Angle

Copper Quest Exploration Inc. (CSE: CQX / OTCQB: IMIMF / FRA: 3MX) is the smallest and most speculative name in this copper basket. The company is focused on copper, molybdenum, and gold exploration across North America, with a portfolio that includes Rip, STARS, Kitimat, Alpine, Auxer, Nekash, Stellar, and Thane.

The near-term catalyst is the Rip Copper-Molybdenum Project in British Columbia. Copper Quest recently commenced a minimum 2,000-metre drill program at Rip, targeting two porphyry Cu-Mo mineralized centres identified through geophysics, airborne magnetics, and 3D induced polarization work.

- Investor data point: CQX has roughly 118.4M issued shares, about 54.2M reserved for issuance, and a market cap near CA$10.9M, giving it higher risk but more torque if drilling strengthens the Rip discovery thesis.

The broader portfolio also matters. Copper Quest says its North American critical-mineral land package includes 8 projects spanning more than 46,000 hectares. That gives IMIMF several possible news-flow channels, but the stock still depends heavily on drill results, financing discipline, and whether the company can turn targets into meaningful mineralized zones.

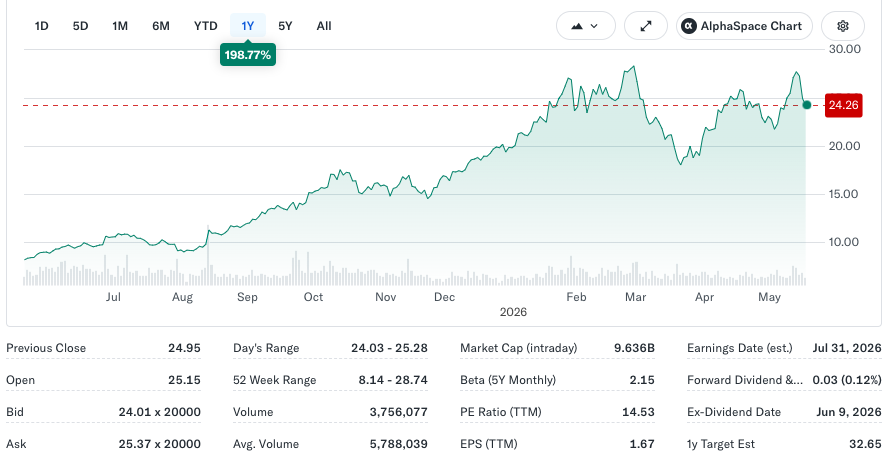

2. Taseko Mines: Producing Copper Exposure

Taseko Mines (NYSE American: TGB / TSX: TKO) gives investors more direct copper exposure through production and development assets. Unlike Copper Quest, Taseko is not only an exploration story. It owns the Gibraltar mine in British Columbia and has development upside through Florence Copper in Arizona.

Recent market data showed TGB trading in the US$6.90–US$7.40 range, with market cap around US$2.5B–US$2.7B. Taseko is useful in this basket because it gives investors a producing copper name with exposure to higher copper prices and project expansion.

- Investor data point: Taseko’s Gibraltar operation produced 98M pounds of copper and 1.9M pounds of molybdenum in 2025, giving TGB real operating leverage to copper prices.

The attraction is that Taseko offers production, cash-flow potential, and Florence Copper optionality. The risk is that producers remain exposed to operating costs, copper-price volatility, permitting, capex, and project execution.

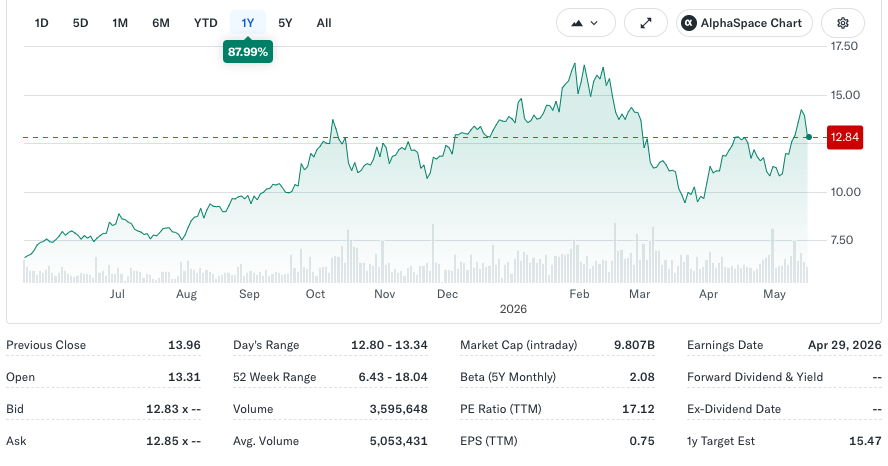

3. Capstone Copper: Mid-Cap Copper Scale

Capstone Copper (TSX: CS) is a larger copper producer with operations across the Americas. It gives investors more scale than a junior explorer, while still offering more copper sensitivity than diversified mining giants.

Recent market data showed CS trading around CA$12–CA$13, with market cap around CA$9B–CA$10B. Capstone is one of the cleaner mid-cap copper producer comparisons because it already has a meaningful revenue base and operating leverage to copper prices.

- Investor data point: Capstone’s trailing revenue has been reported around US$3.46B, with strong growth from copper operations and expansion projects.

For investors, the appeal is scale and torque. Capstone can benefit directly from higher realized copper prices, but the stock already reflects part of the copper bull case. Execution, costs, production growth, and balance-sheet discipline remain key watch items.

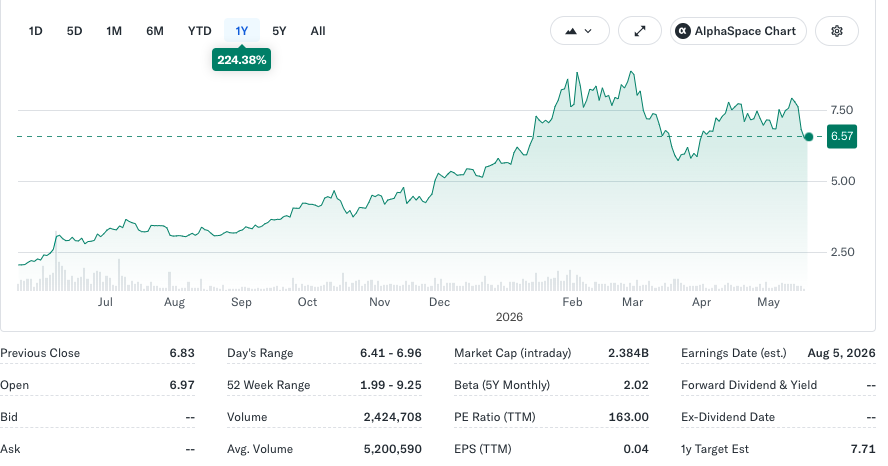

4. Hudbay Minerals: Copper Growth and M&A Leverage

Hudbay Minerals (NYSE: HBM / TSX: HBM) is another closely watched copper-linked miner. The company has copper exposure through existing operations and has been expanding its U.S. copper strategy, including the proposed acquisition of Arizona Sonoran Copper Company.

Recent market data showed HBM trading around US$24–US$25, with market cap near US$9B–US$10B. Hudbay has already had a strong move, but it remains relevant because it combines production exposure, earnings leverage, and growth through copper-focused M&A.

- Investor data point: Recent updates showed HBM posted roughly 67% EPS growth and 27% sales growth, while the Arizona Sonoran deal was valued around US$1.48B.

Hudbay’s appeal is that it gives investors a more mature copper growth story. The risk is that M&A brings integration risk, project risk, and valuation risk if copper prices cool or growth expectations move too far ahead of fundamentals.

5. Trilogy Metals: High-Beta Copper Development

Trilogy Metals (NYSE American: TMQ / TSX: TMQ) is a development-stage copper name focused on Alaska’s Ambler Mining District. It is not a producer, which makes the stock more sensitive to permitting, project updates, strategic interest, and investor appetite for future copper supply.

Recent market data showed TMQ trading around US$4.40–US$6.10, with market cap in the US$780M–US$870M range. The stock’s wide trading range shows how volatile copper development stories can be when sentiment shifts.

- Investor data point: TMQ has traded in a wide 52-week range of roughly US$1.13–US$11.29, highlighting both the upside torque and downside volatility of pre-production copper development stocks.

Trilogy is useful as a comparison for CQX because it shows how the market can assign much larger valuations to copper assets once project scale becomes more defined. The risk is that development-stage projects require time, capital, permitting success, infrastructure, and strong commodity conditions.

Stock Snapshot

| Company | Ticker | Recent Price | Market Cap | Latest Key Number | Main Copper Angle |

|---|---|---|---|---|---|

| Copper Quest Exploration | CSE: CQX / OTCQB: IMIMF | ~CA$0.09 | ~CA$10.9M | 2,000-metre Rip drill program | Micro-cap copper-moly exploration |

| Taseko Mines | NYSE American: TGB / TSX: TKO | ~US$6.90–US$7.40 | ~US$2.5B–US$2.7B | 98M lb copper produced in 2025 | Copper production and Florence Copper upside |

| Capstone Copper | TSX: CS | ~CA$12–CA$13 | ~CA$9B–CA$10B | Revenue around US$3.46B | Mid-cap copper producer leverage |

| Hudbay Minerals | NYSE: HBM / TSX: HBM | ~US$24–US$25 | ~US$9B–US$10B | EPS +67%, sales +27% in recent quarter | Producer growth and U.S. copper M&A |

| Trilogy Metals | NYSE American: TMQ / TSX: TMQ | ~US$4.40–US$6.10 | ~US$780M–US$870M | 52-week range: US$1.13–US$11.29 | High-beta copper development |

Bottom Line

Copper Quest is the speculative micro-cap in this copper basket. CQX / IMIMF has a defined drill catalyst at Rip, a broader 46,000-hectare North American critical-minerals portfolio, and exposure to a copper market where demand could rise 50% by 2040.

The larger names offer different risk profiles: TGB for production and Florence Copper, CS for mid-cap scale, HBM for copper growth and M&A, and TMQ for high-beta development exposure. For CQX, the next proof points are simple: drill results, follow-up targets, financing discipline, and whether Rip can become a more credible copper-moly discovery story.

This is sponsored content. Investors should conduct their own due diligence and consult a qualified financial advisor before making any investment decisions.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}