Gold Mining (NYSE American: GLDG) is a gold-focused royalty company offering creative financing solutions to the metals and mining industry. Its mission is to acquire royalties, streams, and similar interests at varying stages of the mine life cycle to build a balanced portfolio offering near-, medium–, and long-term attractive returns for its investors.

What is a gold royalty?

A gold royalty is a contract that gives the owner (a gold royalty company) the right to a percentage of gold production or revenue in exchange for an upfront payment. Gold royalty companies use these contracts to finance junior and established mining companies needing capital.

Unlike many financial deals, each party benefits almost equally. GLDG provides the financing for exploration and production and gets a royalty on each ounce produced, or whatever the weight unit the target commodity is measured in. GLDG keeps working with the company to ensure growth for itself and its holdings.

Here is a detailed research report on GLDR and the Corporate deck for a deep dive into the Company.

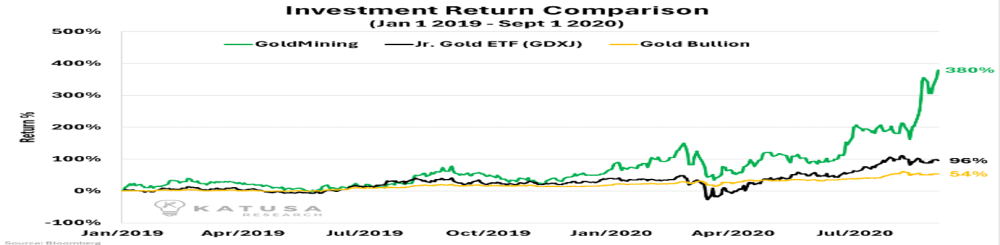

There are very few companies that employ this gold/copper (and recently uranium) per royalty concept, but the successful returns are in the graphing;

There are a million reasons a project can fail. This fact is where it gets interesting for GoldMining Inc.

GG’s vision is NOT to risk the farm on one project. It is difficult to take on the capital expense, risk, and stress of putting a mine into production.

“With a diversified portfolio, we’re less exposed to single project, high risks faced by many in the gold production business,” (CEO Alastair Still)

Instead, GoldMining Inc. takes a more ‘value investor’ approach.

To highlight the quality of the holdings, investors need to look no further than the 15% of Gold Royalty Corp (Groy), a great gold royalty company in its own right. As GROY looks to add more producing royalties or some of its advanced-stage existing royalties ramp up towards production, its value proposition improves. That’s not a guarantee; it’s just common sense at this point.

That means, very simply, that GLDG buys up mining projects when gold markets are relatively low, holds onto them until the right moment… and buys them when no one else wants them.

This happened 15 years ago when projects were sold at depressed prices by single-asset companies that couldn’t raise the capital required to advance the asset.

The GLDG commodity exposure is 81% Gold or equivalents, 18% Silver, and 1% Copper. Wait for Uranium to join the mix.

Royalties assets include properties in Alaska, La Mina Columbia, Tapajos Region Brazil, São Jorge, Brazil, Nutmeg Mountain (USA), and REA Uranium, Canada.

Crossing Fingers

…is what most mining investors do. ‘Drill on the property’ merde. GLDG actively manages its assets, and investors get a piece of some of the world’s premier mining sites with a higher-than-average payment surety.

With Gold, Copper and now Uranium royalties, GLDG is historically ahead of the cure before the curve rises, eventually steeply. For diehard gold investors, GLDG should find a way into your portfolio. Or GROY, as noted. Someone mentioned that Goldmining would appeal to weak investors as it appeared to be low risk. I agree with the low-risk assessment.

However, when you have some of the best gold minds in the world doing smart deals that lower volatility and present returns 4x better than the physical, you can call me weak, but you need to add smart to that sentence. Aggressive gold players could use this as a base and trade juniors or seniors to enhance profit.

GLDG is almost an Occam’s Razor situation. The in-depth research aside, the approach is simple and somewhat elegant if you’ll forgive personal feelings.

The bottom line is that GLDG provides investors with many advantages.

1. Proxy for the gold market

2. Relatively lower risk

3. Exposure to more prominent and higher quality gold companies

4. Uranium is an example of GLDG moving ahead of the herd.

5. A great example of a long-term hold.

6. Cool Logo.

Have a look. I have put several outside information assets in this piece for your perusal. The company makes sense, good times and bad.

Posted on behalf of Guerilla Capital for the issuer.

{kind=link}