10X ALERTS has received compensation for the publication of this article.

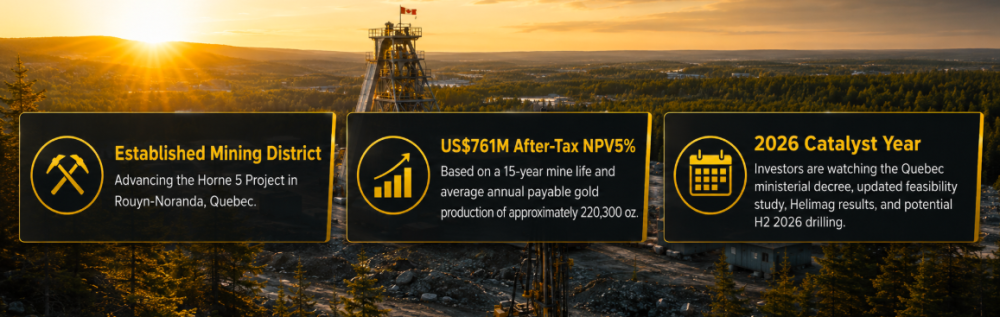

- Falco Resources Ltd. (TSXV: FPC | OTC: FPRGF) is advancing the Horne 5 Project in Rouyn-Noranda, Quebec, one of Canada’s most established mining districts.

- Horne 5 carries a 2021 after-tax NPV5% of US$761 million, based on a 15-year mine life and average annual payable gold production of approximately 220,300 ounces.

- 2026 could be a pivotal year for FPC, with investors watching for the Quebec ministerial decree, an updated feasibility study, Helimag survey results, and potential H2 2026 drilling.

Falco Resources Ltd. (TSXV: FPC | OTC: FPRGF) is not an early-stage gold explorer built around a single discovery hole. The company is positioned around a large, advanced, gold-led polymetallic development project in Quebec, backed by a published feasibility study, defined reserves, and a district-scale land package in the Noranda Mining Camp.

That matters because the current FPC story is less about proving that mineralization exists, and more about whether Falco Resources can convert a technically defined project into a clearer development pathway. With Horne 5 already carrying large-scale economics and the company moving through permitting and feasibility-update work, 2026 could become an important year for the market’s view of FPC.

The Core Asset: Horne 5 in Quebec

Falco Resources’ flagship asset is the Horne 5 Project, located in Rouyn-Noranda, Quebec. The project sits beneath the former Horne Mine, which historically produced approximately 11.6 million ounces of gold and 2.5 billion pounds of copper between 1927 and 1976.

That historical footprint gives FPC a different profile from a greenfield explorer. Horne 5 is located in a proven mining camp with a long production history, established infrastructure, and known gold-copper-zinc-silver mineralization. For investors, the key question is whether Falco Resources can turn that geological and technical foundation into a financeable mine plan.

Horne 5: The Numbers Behind the Story

The 2021 Updated Feasibility Study for Horne 5 outlined mineral reserves of approximately 80.9 million tonnes grading 2.24 g/t gold-equivalent. Over an estimated 15-year mine life, the project is expected to produce more than 3.3 million ounces of gold, 27.3 million ounces of silver, 247 million pounds of copper, and 1.19 billion pounds of zinc.

The study also outlined average annual payable gold production of approximately 220,300 ounces, an after-tax NPV5% of US$761 million, an after-tax IRR of 18.9%, and all-in sustaining costs of US$587 per ounce. For a company recently trading around a C$160M–C$170M market capitalization range, the valuation gap between FPC’s public-market value and the 2021 project NPV is the central investor setup.

Investor Snapshot

| Metric | Falco Resources Snapshot | |

|---|---|---|

| Company | Falco Resources Ltd. | |

| Tickers | TSXV: FPC | OTC: FPRGF |

| Recent share price range | Approximately C$0.47–C$0.51 | |

| Recent market capitalization | Approximately C$160M–C$170M | |

| Flagship asset | Horne 5 Project | |

| Jurisdiction | Quebec, Canada | |

| 2021 after-tax NPV5% | US$761M | |

| 2021 after-tax IRR | 18.9% | |

| Mine life | Approximately 15 years | |

| Average annual payable gold production | Approximately 220,300 oz | |

| AISC | US$587/oz | |

| Main metals | Gold, silver, copper, zinc |

Why the Updated Feasibility Study Matters

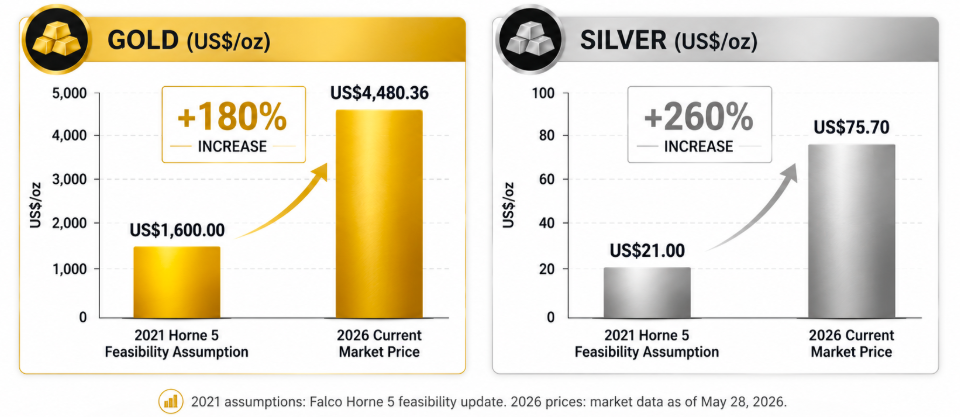

The 2021 feasibility study used metal price assumptions of US$1,600/oz gold, US$21/oz silver, US$3.20/lb copper, and US$1.15/lb zinc. Current market prices for gold, silver, and copper are materially higher than those assumptions, which makes the feasibility update one of the most important upcoming catalysts for FPC.

The key point is not simply that higher metal prices could improve the revenue side of the model. Investors will also be watching how updated capital costs, operating costs, development schedules, and financing assumptions affect the overall project economics. If Falco Resources can show stronger or more resilient economics under today’s market conditions, the updated study could help support a re-rating.

2026 Catalyst Path

Falco Resources has several potential catalysts that could shape the FPC investment case through 2026.

- Quebec ministerial decree: A key permitting milestone that could improve development visibility for Horne 5.

- Updated feasibility study: A potential reset of Horne 5 economics under current commodity prices and updated cost assumptions.

- Financing strategy: Investors will need clarity on how Falco plans to fund development, including the balance between debt, equity, strategic partners, streams, royalties, or other structures.

- Helimag survey results: New geophysical work could refine exploration targets across the Western Noranda Camp.

- Potential H2 2026 drilling: Follow-up drilling could add exploration news flow beyond the core Horne 5 development story.

For FPC, the re-rating path likely depends on reducing uncertainty. The company already has scale. What the market needs next is stronger visibility on permitting, economics, financing, and execution.

Western Noranda: Exploration Upside Beyond the Main Project

While Horne 5 remains the valuation anchor, Falco Resources also controls a large land position in Quebec’s Noranda Mining Camp, including rights across roughly 67,000 hectares. The broader land package includes exposure to multiple former gold and base-metal mine sites.

In April 2026, Falco announced that it had identified several priority targets for a high-resolution heliborne magnetic survey in the Western Noranda Camp. The survey covers approximately 180 square kilometres with 50-metre line spacing and follows earlier airborne gravity gradiometry work that highlighted underexplored areas with potential for volcanogenic massive sulphide systems.

This gives FPC a second layer of potential value creation. Horne 5 is the core development asset, but exploration success across Western Noranda could add discovery optionality and help investors assign more value to Falco’s broader land package.

Market Context: Gold, Copper and Multi-Metal Leverage

Falco Resources gives investors exposure to several commodity themes at once. Gold is the primary driver of the Horne 5 economics, but copper, zinc, and silver add by-product leverage and broaden the project’s relevance in a market focused on electrification, grid expansion, infrastructure demand, and critical-mineral supply.

Silver is especially relevant because Horne 5 is expected to produce approximately 27.3 million ounces of silver over its estimated 15-year mine life, according to the 2021 Updated Feasibility Study. The original feasibility case used a silver price assumption of US$21/oz, while recent market data shows silver trading roughly in the US$73–US$76/oz range in late May 2026. That price gap does not automatically flow directly into project value because costs, recoveries, payability, financing, and updated assumptions all matter, but it does strengthen the reason investors will be watching Falco’s updated feasibility work closely.

That polymetallic profile matters. By-product credits can support project economics when prices are favorable, and a large gold-led project with copper, zinc, and silver exposure may appeal to a wider investor base than a single-metal development story. For FPC, the updated feasibility work will be important because it should help investors understand how that multi-metal exposure translates into economics under today’s market conditions.

Valuation Setup: Why FPC Is Being Watched

The main attraction in the Falco Resources story is the gap between the company’s recent market capitalization and the 2021 after-tax NPV of Horne 5. A recent C$160M–C$170M market capitalization compares with a 2021 project after-tax NPV5% of US$761 million.

That does not automatically mean FPC is undervalued. Development-stage mining companies often trade at steep discounts to project NPV because investors must price in permitting risk, financing risk, construction risk, dilution risk, and commodity-price volatility. However, it does mean Falco Resources has a clear re-rating framework if the company can reduce those risks through 2026.

What Investors Should Watch Next

- Permitting progress: The Quebec ministerial decree remains one of the most important near-term milestones.

- Updated economics: Investors should compare the upcoming feasibility update against the 2021 study, especially on capex, AISC, NPV, IRR, payback, and metal-price assumptions.

- Financing structure: The market will want to see whether Falco can fund Horne 5 in a way that limits excessive dilution.

- Exploration results: Helimag targets and potential H2 2026 drilling could create additional catalysts.

- Market recognition: If execution improves, the valuation discount to project NPV could begin to narrow.

What Could Change the View

The constructive case for Falco Resources depends on execution. A positive permitting outcome, a stronger updated feasibility study, credible financing progress, and exploration momentum would strengthen the FPC thesis.

The main risks are also execution-related. Horne 5 is a large development project, and large projects require major capital, careful permitting, strong cost control, and disciplined financing. Investors should monitor capital cost inflation, funding terms, timeline changes, dilution potential, and commodity-price sensitivity as the project advances.

Bottom Line

Falco Resources Ltd. (TSXV: FPC | OTC: FPRGF) offers exposure to a large, advanced, gold-led polymetallic project in Quebec at a public-market valuation that remains well below the 2021 after-tax NPV of Horne 5. With permitting, feasibility work, and Western Noranda exploration all moving into focus, FPC has a clear 2026 catalyst path.

The opportunity is not risk-free, but the setup is straightforward: Falco Resources already has project scale, defined economics, and district exposure. If the company can convert those ingredients into permitting progress, updated economics, and a credible financing path, FPC could become a more visible name among Canadian gold developers in 2026.

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own due diligence and consider the risks associated with junior mining and development-stage companies.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}