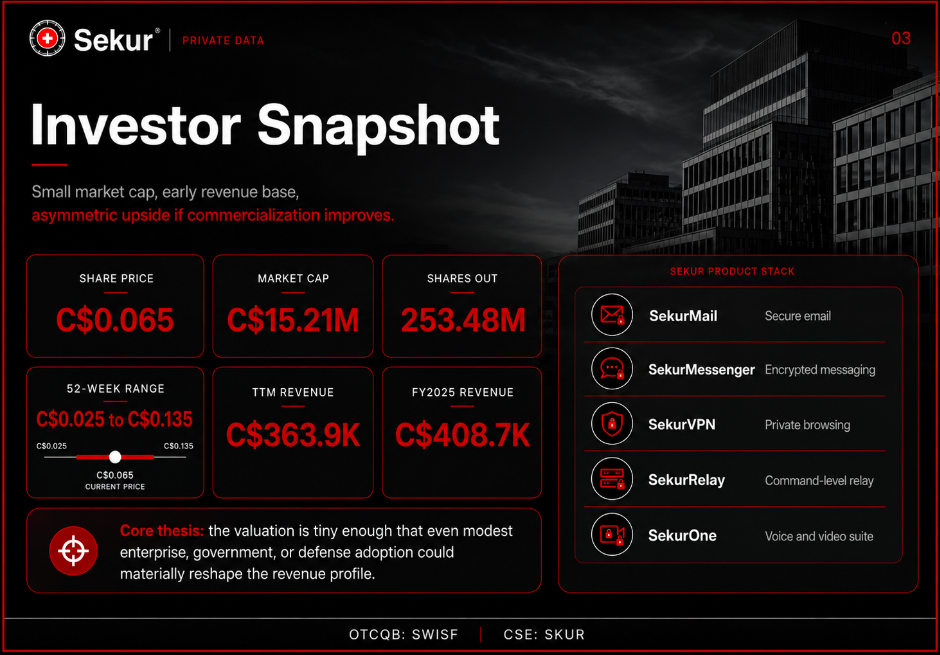

• Sekur Private Data trades at microcap levels, with a recent share price around C$0.06 and a market cap near C$15 million.

• The company is building a Swiss-hosted privacy and cybersecurity platform across secure email, messaging, VPN, and corporate/government packages.

• The investment case is not about current financial strength. It is about whether Sekur can convert its privacy positioning into higher-margin recurring revenue by 2026–2027.

Cybersecurity is no longer just an enterprise IT budget item. It has become a boardroom issue, a government issue, a defense issue, and increasingly a personal privacy issue.

That is the market Sekur Private Data Ltd. is trying to attack.

Sekur Private Data, trading on the OTCQB under SWISF, positions itself as a Swiss-hosted cybersecurity and private communications company. Its product suite includes SekurMail, SekurMessenger, SekurVPN, SekurOne, and newer corporate and premium packages aimed at businesses, high-net-worth users, governments, and privacy-conscious customers.

The core pitch is simple: communication tools have become dependent on Big Tech infrastructure, cloud platforms, data harvesting, and increasingly complex cyberattack surfaces. Sekur is trying to offer an alternative built around Swiss data privacy, proprietary infrastructure, encrypted communications, and independence from major U.S. cloud platforms.

For investors following OTCQB: SWISF, this creates a speculative but interesting microcap setup.

Sekur is not yet a proven cybersecurity compounder. It is still a small company with limited revenue and an early-stage business model. But the stock’s valuation is also small enough that even modest commercial traction could change how the market looks at the company.

| Metric | Recent Figure |

|---|---|

| Company | Sekur Private Data Ltd. |

| Tickers | SKUR / SWISF |

| Sector | Cybersecurity / privacy communications |

| Recent share price | Around C$0.06 |

| Recent market cap | Around C$15 million |

| 52-week range | About C$0.025 to C$0.135 |

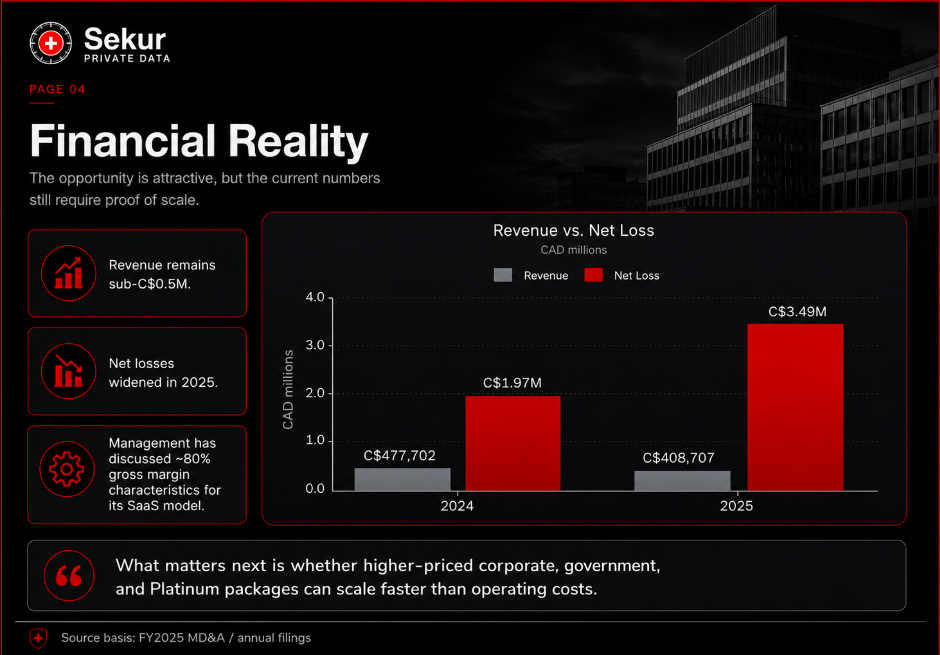

| FY2025 revenue | C$408,707 |

| FY2025 net loss | C$3.49 million |

| Main investor question | Can Sekur scale recurring revenue before dilution becomes the bigger story? |

Why This Story Exists

Sekur’s story sits at the intersection of three investor themes:

First, cybersecurity spending continues to expand as companies, governments, and individuals face more sophisticated digital threats.

Second, data privacy is becoming more valuable as users become more aware of surveillance, cloud dependency, phishing, and unauthorized data access.

Third, sovereign and jurisdiction-based technology is gaining attention. Companies that can offer non-Big-Tech infrastructure, Swiss data storage, or privacy-first communications may appeal to customers who want more control over where their data lives.

Sekur’s website emphasizes that its data is stored and processed in Switzerland, using its own encrypted private infrastructure, away from Big Tech hosting such as AWS, Microsoft Cloud, and Google Cloud. That gives the company a clear positioning angle: not just secure communications, but privacy infrastructure outside the dominant cloud ecosystem.

That is the bull case.

The challenge is that a clear positioning angle is not the same as a scaled business.

The Financial Reality

Sekur’s current financials show a company that is still early.

For FY2025, Sekur reported revenue of C$408,707, down from C$477,702 in FY2024. Net loss widened to C$3.49 million from C$1.97 million the year before.

The company’s revenue is currently very small relative to its market capitalization. That means investors are not buying Sekur because of today’s earnings power. They are buying the possibility that the company can transition from an early-stage privacy platform into a recurring-revenue cybersecurity business.

The gross-profit picture is more encouraging. FY2025 gross profit was approximately C$368,991 on C$408,707 of revenue, implying a high gross-margin profile. That is important because SaaS-style privacy tools can become attractive if customer acquisition, retention, and operating expenses are brought under control.

But the cost base is still the main issue.

In 2025, Sekur reported expenses of about C$3.79 million. Marketing alone represented approximately C$1.25 million. IT maintenance was C$620,000. Research, development, and software maintenance was roughly C$499,000. Director fees, consulting, professional services, depreciation, and other costs also contributed to the loss.

This is the key financial tension: the product model may have high gross margins, but the company needs enough revenue scale to absorb public-company costs, marketing spend, and platform development.

Until that happens, Sekur remains a speculative growth story rather than a fundamentally profitable cybersecurity investment.

The Revenue Mix

Sekur’s FY2025 revenue was still heavily dependent on direct customer purchases.

Direct customer purchases accounted for roughly C$400,130 of revenue, while business-to-business partner revenue was only about C$8,577.

That matters because the next stage of the story likely depends on larger accounts, corporate packages, government channels, distributors, partnerships, and higher-priced plans. If Sekur remains mainly a small direct-to-consumer privacy app business, scaling may be slow. If the company can shift toward enterprise, government, defense, and premium corporate packages, the revenue profile could become more interesting.

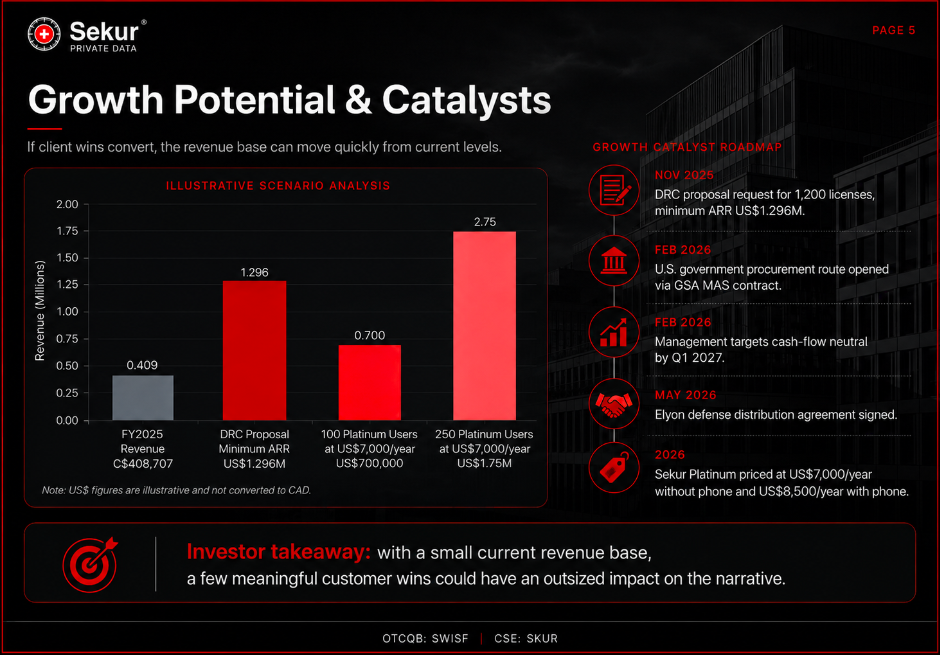

Management has already pointed investors toward this direction.

The company has discussed Sekur Corporate, Sekur Government, Sekur Platinum, market expansion, higher-priced packages, and a target of reaching cash-flow neutral by Q1 2027.

That is the key milestone.

If Sekur can show revenue acceleration in 2026, while reducing or controlling expenses, the stock could begin to trade less like a distressed microcap and more like an early-stage cybersecurity SaaS candidate.

The Product Angle

Sekur’s product stack gives the company multiple ways to monetize privacy.

SekurMail targets secure email and private communications. SekurMessenger targets encrypted messaging. SekurVPN addresses private browsing and secure network access. SekurOne appears positioned as a broader bundle or secure productivity layer. The company’s corporate and premium packages are intended to move beyond basic consumer subscriptions and into higher-value accounts.

The strongest part of the product thesis is the Swiss-hosted positioning.

Sekur is not trying to beat Microsoft, Google, Proton, Signal, VPN providers, and enterprise cybersecurity firms on scale. Instead, the company is trying to carve out a niche around privacy, jurisdiction, secure communications, proprietary infrastructure, and independence from large cloud platforms.

That niche could matter.

Governments, executives, lawyers, financial professionals, defense-linked organizations, journalists, activists, healthcare users, and international businesses may all have reasons to value privacy infrastructure that is positioned differently from mainstream communications tools.

But for investors, product positioning still needs to convert into measurable traction.

The company needs more than a strong privacy message. It needs paying customers, lower churn, larger accounts, distributor momentum, government validation, and recurring revenue growth.

What Could Drive a Re-Rating

Sekur does not need to become a large cybersecurity company to move the needle. With a market cap around the low-to-mid tens of millions of Canadian dollars, the stock is highly sensitive to signs of revenue acceleration.

The re-rating case would likely depend on six things:

• Revenue begins growing again after the FY2025 decline

• Corporate and government packages start contributing meaningful revenue

• Sekur Platinum or higher-priced packages improve average revenue per user

• Gross margins remain high as revenue scales

• Operating expenses are reduced or grow slower than revenue

• Management shows a credible path toward cash-flow neutral by Q1 2027

The strongest version of the bull case would be simple: Sekur uses its current privacy product base to move into higher-ticket business, government, and premium accounts, while keeping gross margins high and narrowing losses.

If that happens, the current valuation could look too small.

The weaker version is that the company continues spending heavily on marketing and public-company costs while revenue remains flat or inconsistent. In that case, shareholders could face more dilution before the business reaches scale.

Key Risks

Like most microcap growth companies, Sekur still faces execution challenges as it works to expand its customer base and grow recurring revenue.

The company is operating in competitive markets that include secure email, encrypted messaging, VPN services, and privacy software. Success will depend on management’s ability to convert its Swiss-hosted privacy positioning into broader commercial adoption.

Investors should also recognize that microcap stocks can experience higher volatility and lower trading liquidity than larger companies, including OTCQB-listed shares such as SWISF.

10xAlerts View

Sekur Private Data is not a safe cybersecurity stock. It is a small, speculative, privacy-focused SaaS/cybersecurity name with a potentially interesting setup if management can execute.

The company has a strong narrative: Swiss-hosted privacy, secure communications, independence from Big Tech infrastructure, and a product suite aimed at individuals, businesses, and governments.

But the financials are still early. FY2025 revenue was below C$500,000, the net loss was C$3.49 million, and the company needs to prove that new premium, corporate, and government offerings can materially change the revenue curve.

For investors, Sekur is a watchlist-style microcap, not a proven compounder.

The upside case is that a small market cap, high gross-margin product model, and new higher-ticket packages create operating leverage if revenue starts to scale.

The downside case is simply that growth takes longer than expected.

Bottom line

Sekur Private Data (OTCQB: SWISF) offers investors exposure to the growing themes of cybersecurity, privacy, and sovereign data infrastructure through a company that is still in the early stages of commercialization. While the business remains small today, management is focused on expanding recurring revenue through corporate, government, and premium offerings. For investors comfortable with microcap opportunities, SWISF is a name worth watching as the company works toward revenue growth and its stated goal of reaching cash-flow neutrality by Q1 2027.

Not financial advice. Sponsored content may involve compensation. Investors should conduct their own due diligence and consider the volatility and liquidity characteristics commonly associated with microcap securities, including OTCQB-listed stocks such as SWISF.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}