I’m re-entering the commodity space because recent market action has made it clear that a smooth macro outcome is not being priced in. When headlines alone can move commodities 10–15% in a single session, I don’t want my portfolio to rely entirely on one narrative (AI growth, rate cuts, or a so‑called soft landing).

Instead, I prefer diversified exposure to assets that react differently as investor confidence rises or breaks.

Gold and silver sit at the center of that framework, but they are not the same trade. Gold acts primarily as a monetary hedge and geopolitical barometer, while silver represents a higher‑beta expression of the same forces — capable of outperforming sharply in risk‑on phases, but also unwinding much faster when sentiment turns.

SECTOR / MACRO CONTEXT — WHAT THE TAPE IS TELLING ME

Gold is acting as a regime asset

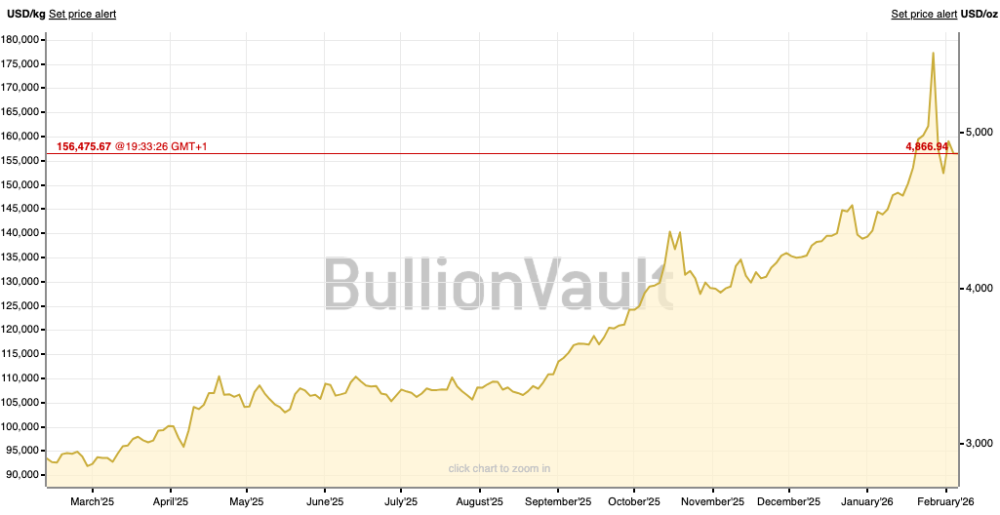

Despite experiencing some of the sharpest pullbacks in its history, gold remains elevated relative to long‑term norms. As of February 5, 2026, gold was trading around US$5,048/oz, down roughly 4.6% over 24 hours.

For context:

- 1 month ago: ~US$4,425/oz

- 1 year ago: ~US$2,856/oz

- 12‑month change: ~+68.6%

Demand has also been structurally strong. According to the World Gold Council:

- Total gold demand (2025): ~5,000 tonnes (record)

- ETF inflows: +801 tonnes (2nd‑largest year on record)

- Investment demand: ~2,175 tonnes (record)

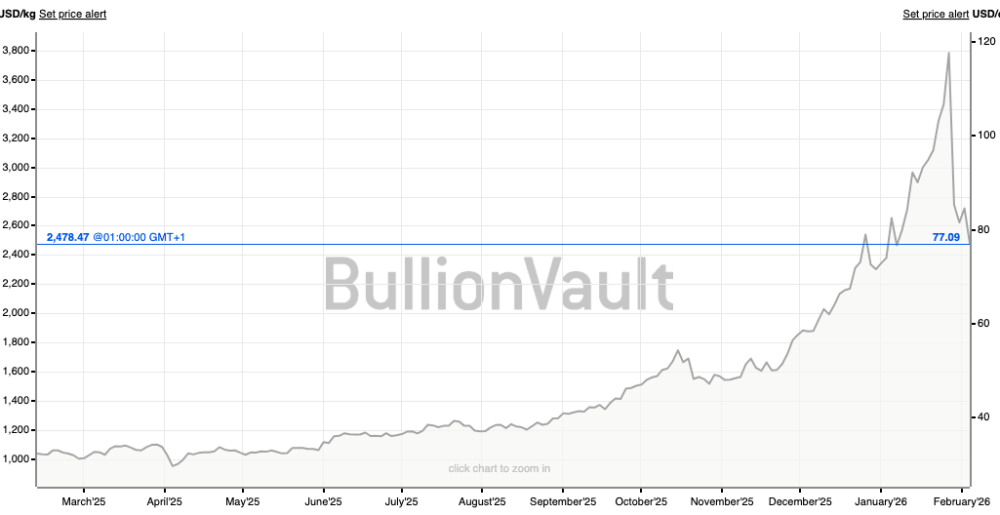

Silver is the volatility engine

Silver has been the most volatile major commodity during the recent move. According to Reuters, silver recently hit a peak near US$121.64/oz before pulling back sharply to around US$76.76/oz on February 5, 2026, representing an intraday move of roughly ‑13% while still sitting approximately +138% higher year‑over‑year. That level of volatility is precisely why I treat silver differently from gold: I keep position sizes smaller, manage risk more tightly, and view silver exposure as tactical rather than core within a broader commodities allocation.

In risk‑on phases, silver can outperform gold. When safe‑haven demand fades, the drawdowns can be severe.

GEOPOLITICS & POLITICS — WHY THESE MOVES ARE HAPPENING

Precious metals are reacting directly to shifts in tail risk. According to Reuters, the recent sell‑off followed:

- Easing U.S.–Iran tensions and plans for renewed talks

- A constructive U.S.–China leadership call

Earlier in the cycle, gold surged above US$5,100/oz as tariff risk and political uncertainty drove a safe‑haven bid.

My takeaway:

- Rising risk → gold behaves like insurance

- Falling risk → the unwind can be fast

IS THE STOCK MARKET CRASHING — OR JUST CORRECTING?

I view the current environment as a correction with fragile psychology, not a full‑blown crash.

Two drivers stand out:

- Tech & AI valuation anxiety: Reuters reported U.S. stocks falling as investors questioned whether massive AI capex will deliver near‑term returns

- Macro & growth fears: AP highlighted softening labor data and rising concern over slowing economic growth

When equity drawdowns are driven by valuation and growth fears, gold often reasserts itself as a hedge — especially when investors are unsure whether rate cuts are coming because inflation is beaten, or because growth is breaking.

HOW I PLAY GOLD EQUITIES — THE PRODUCER FRAMEWORK

If I express a gold view through equities, I prefer liquidity and operating leverage, which historically means major producers.

My simplified framework:

- Gold rises → miner revenues and margins expand

- Cash flow improves → buybacks, dividends, debt reduction become viable

- Institutional capital enters → large caps capture the first wave

Reuters highlighted this dynamic during the late‑January rally, when major miners such as Newmont, Barrick, Agnico, and Kinross jumped alongside record gold prices.

Major producers (prices as of Feb 5, 2026)

- Newmont (NEM): US$109.99

- Agnico Eagle (AEM): US$192.04

- Kinross (KGC): US$31.48

I also complement these majors with select early‑stage explorers when gold is in a favorable regime. Golden Rapture Mining (GLDR) and Colibri Resource (CBI/CRUCF) are examples I treat as modestly sized exploration investments — focused on asset advancement and geological upside, not standalone theses.

CATALYSTS I’M MONITORING

- Geopolitical escalation or de‑escalation

- U.S. rate expectations and real yields

- Equity risk sentiment

- Inflation surprises versus growth fears

RISKS

- Sustained risk‑on rebound draining safe‑haven flows

- A stronger U.S. dollar

- Silver‑driven volatility spilling into broader portfolios

- Producer‑specific risks (cost inflation, jurisdictional exposure)

BOTTOM LINE

Gold tells me the market still wants insurance. Silver tells me positioning is crowded and emotions are elevated. Equities tell me the AI‑led rally is being stress‑tested by valuation, capex, and growth risk.

In this environment, I prefer a blend of gold exposure as a hedge, major producers for liquid leverage, and silver as a high‑volatility satellite.

SOURCES (PUBLIC)

- Fortune — current gold price (Feb 5, 2026): https://fortune.com/article/current-price-of-gold-02-05-2026/

- World Gold Council — Gold Demand Trends full-year 2025: https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2025

- Reuters — gold above $5,100 record high (Jan 25–26, 2026): https://www.reuters.com/business/finance/gold-rushes-record-high-above-5000oz-2026-01-25/ ; https://www.reuters.com/business/finance/gold-races-5100-record-peak-safe-haven-demand-2026-01-26/

- Reuters — commodity sell-off / silver drop / geopolitical easing (Feb 5, 2026): https://www.reuters.com/world/china/precious-metals-oil-slide-global-tensions-ease-copper-down-2026-02-05/

- Trading Economics — silver price + YoY change (Feb 5, 2026): https://tradingeconomics.com/commodity/silver

- Reuters — miners up as gold hits records (Jan 26, 2026): https://www.reuters.com/world/africa/gold-miner-shares-jump-bullion-prices-hit-5100oz-record-high-2026-01-26/

- Reuters — Wall Street slide on tech/AI spending concerns (Feb 5, 2026): https://www.reuters.com/business/sp-nasdaq-futures-subdued-markets-digest-alphabets-ai-spending-plans-2026-02-05/

- AP — markets fall on capex + jobs data (Feb 5, 2026): https://apnews.com/article/d4ed66429ffa2f50f2feea99b0e583ed

- Live equity prices used (Feb 5, 2026): Newmont (NEM), Agnico Eagle (AEM), Kinross (KGC)

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}