Golden Rapture Mining (CSE: GLDR) is a Canadian junior gold exploration company offering leveraged exposure to gold in Ontario, Canada, one of the world’s most established and mining-friendly jurisdictions. With fresh capital in hand, a district-scale asset, and a supportive gold price environment, GLDR fits the classic early-stage exploration setup where valuation can move quickly on technical success.

Company Overview

Golden Rapture’s strategy is straightforward: acquire and advance geologically validated gold assets in proven districts and apply modern exploration techniques to identify extensions, depth potential, and new zones overlooked by historical operators. The company is positioned as a high-beta exploration play, meaning outcomes are driven primarily by exploration results and gold-market conditions rather than near-term production metrics.

Asset Portfolio & Project Focus — Northern Queen

Golden Rapture’s flagship asset is the Northern Queen Gold Project in Ontario. The project sits in a historically productive gold district, reducing pure greenfield risk and providing a geological framework investors already understand.

Key characteristics include:

- Documented historical gold production and mineralization

- Existing underground workings and surface infrastructure remnants

- Geological settings consistent with structurally controlled Ontario gold systems

The core thesis is that historical mining targeted near-surface, high-grade zones using limited technology, leaving meaningful upside potential at depth and along strike.

Recent Financing & Capital Structure

Golden Rapture recently completed a $500,000 flow-through and non-flow-through financing, strengthening its treasury and enabling near-term exploration activity.

Why this matters:

- Provides working capital for field programs, sampling, and technical work

- Flow-through component aligns spending with Canadian exploration incentives

- Modest raise limits dilution compared to many junior peers

- Signals continued operational momentum rather than a dormant treasury

For a company at this stage, access to capital — even at a modest scale — is a key de-risking factor.

Strategic Context, Neighbors & District Validation

In gold exploration, location is often as important as geology. Northern Queen benefits from being located in an established Ontario gold belt where:

- Historical mines confirm the presence of economic gold systems

- Regional structures and controls are well mapped

- Nearby exploration and mining activity provide district-scale validation

Ontario districts such as Red Lake, Timmins, and surrounding camps have historically produced multi-million-ounce deposits and continue to attract exploration capital. Projects located within or adjacent to these belts tend to be better understood by the market, which can accelerate re-rating when results emerge.

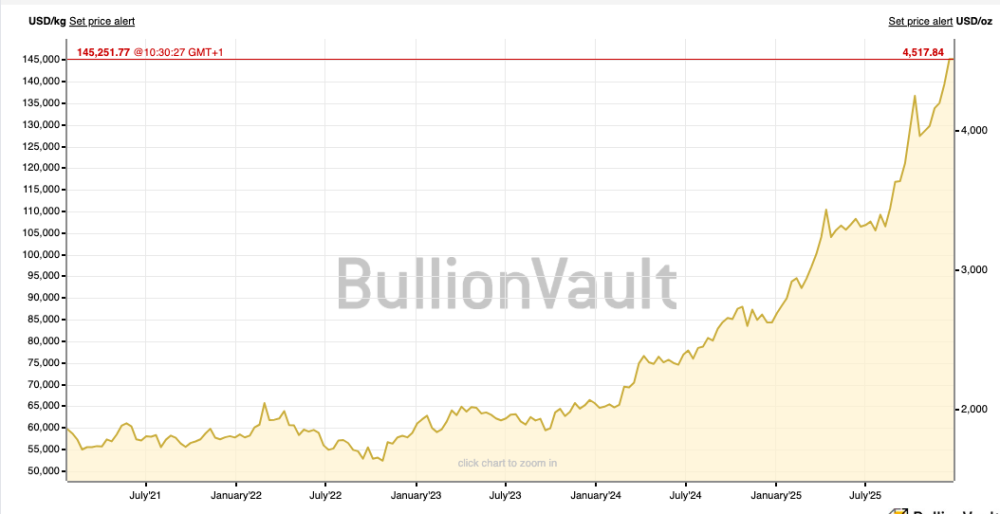

Gold Market Backdrop — Numbers First

The macro environment remains supportive for gold and, by extension, junior explorers:

- Spot gold hit fresh record highs around US$4,500/oz on Dec 26, 2025 (spot quoted near US$4,501/oz, after a session peak around US$4,531/oz).

- Gold is up ~70–72% year-to-date in 2025, marking its strongest annual performance in decades.

- Central-bank demand remains a key pillar: official-sector buying totaled 53 tonnes in Oct 2025 (+36% m/m), and purchases were reported at ~254 tonnes YTD through end-Oct 2025.

- Global public debt has surpassed US$100 trillion (2024), reinforcing gold’s role as a hard-asset hedge as fiscal and geopolitical risk stay elevated.

For early-stage explorers like GLDR, higher gold prices increase the perceived value of in-ground ounces, improve acquisition economics, and raise investor appetite for discovery-stage risk.

Key Risks & Execution Factors

Golden Rapture remains a speculative exploration company, with risks typical of the sector:

- Exploration risk: results may not confirm economic mineralization

- Financing risk: continued access to capital is required

- Market volatility: junior miners are sensitive to sentiment shifts

- Execution risk: delays in permitting, fieldwork, or interpretation

GLDR should be viewed as a high-risk, high-reward exploration vehicle, not a near-term producer.

Re-Rating Catalysts

Potential value drivers include:

- Positive sampling or exploration results

- Confirmation of grade continuity or new zones

- Follow-up drill programs

- A rising gold price environment

- Strategic interest at the project or district level

In junior gold equities, even early technical success can lead to outsized valuation moves if results exceed market expectations.

Bottom Line

Golden Rapture Mining (CSE: GLDR) offers leveraged exposure to gold exploration in a tier-one jurisdiction at a time when gold fundamentals remain strong. With fresh capital, a historically validated asset, and multiple exploration catalysts ahead, GLDR fits the classic junior explorer profile where discovery success — not production — drives valuation. As always in early-stage mining, execution and results will determine whether the story re-rates.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}