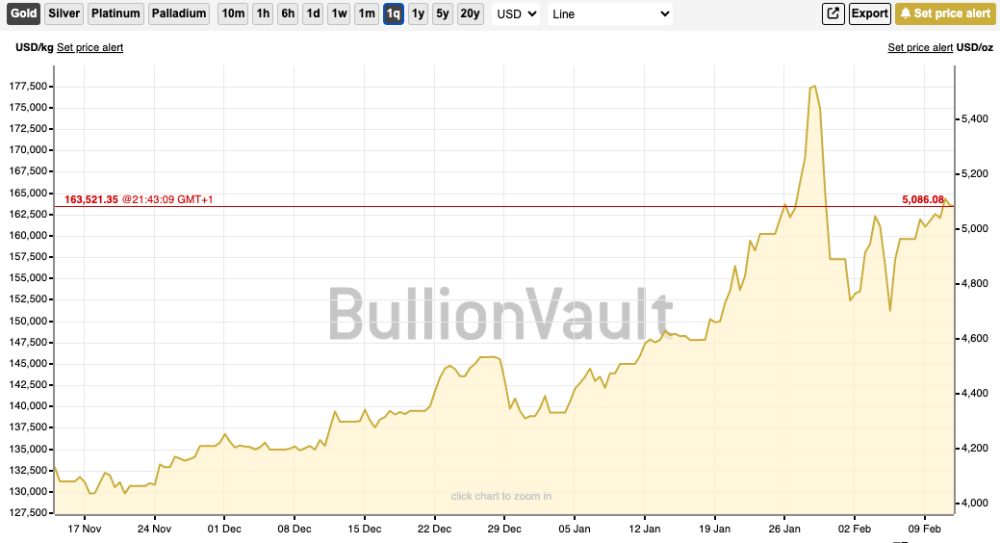

Gold’s current price, near $5,040 per ounce in early 2026, is near cycle highs. Spot gold prices are firmly above the psychologically important $5,000 per ounce. Spot gold prices have risen about 70 percent year-over-year following a strong gold price rally in 2024-25.

Importantly, gold’s current price move is supported by more than speculative buying alone. According to data from the World Gold Council, central banks purchased approximately 863 tonnes of gold in 2025, which is significantly higher than the 2010-21 annual average of ~473 tonnes. The level of central bank gold purchases also continued into late 2025, with ~230 tonnes being purchased in Q4 alone.

Central banks continue to buy gold due to ongoing geopolitical tensions, trade disintegration and currency diversification strategies. Central banks view gold as a strategic reserve asset due to its ability to provide a hedge against inflation and currency devaluation risks. Historically, gold equities have not moved in lock step. Bullion and the major producers tend to be early leaders in gold price rallies, while junior miners tend to lag behind them early in the rally but ultimately outperform them as the capital inflow to junior miners increases due to the higher-risk/higher-reward dynamics.

Historically, the valuations of junior gold miners have been very low relative to their peers. Therefore, the opportunity exists for a significant “catch-up” in the price of junior gold miners relative to the gold price and other junior gold miners.

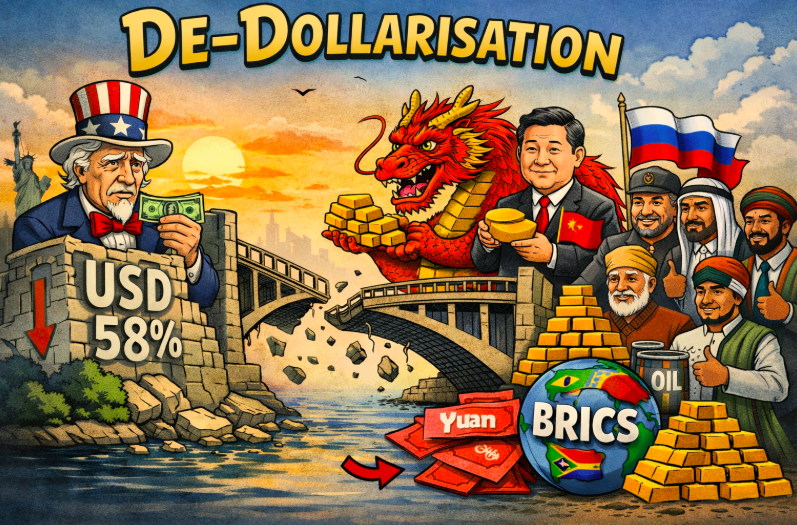

Geopolitical Map — De-Dollarisation & Strategic Gold Flows

Geopolitical realignment is becoming a major driver of gold demand rather than Western investor cycles. The rivalry between the United States and China is accelerating reserve diversification. Since 2019, China has increased its gold reserves by +300+ tonnes and now holds approximately 2,250 tonnes of gold, while it has been reducing its holding of U.S. Treasuries.

Emerging markets are following a similar pattern. The U.S. dollar’s share of global foreign exchange reserves has declined to approximately 58 percent, down from approximately 71 percent in 1999, based on International Monetary Fund (IMF) data. During this time, gold’s role as a neutral reserve asset has increased, especially among BRICS and non-aligned economies looking to insulate themselves from the threat of sanctions and currency volatility.

This is why central bank gold buying has persisted even as Western interest rate expectations have changed. As a result, this creates a persistent demand floor for gold prices and supports longer-duration cycles for junior miners where discovery and resource growth will be rewarded in excess of short-term macro trades.

Why the Junior Miner Window Is Opening

At gold prices above $5,000 per ounce, the financial conditions for exploration companies change dramatically. At higher gold prices, lower cut-off grades become economically viable, larger mineable ounces become available and the appeal of marginal projects increases.

These are structural factors and not related to short-term trading flows. According to the World Gold Council, ~95 percent of surveyed central banks plan to either increase or maintain their gold reserves over the next 12 months and ~43 percent of surveyed central banks plan to increase their gold reserves versus their 2024 levels. These institutional bids reduce the availability of free float gold and support sustained gold prices.

- During late-cycle gold price moves, junior explorers typically exhibit 2-5X leverage to gold price movements.

- Selectively, capital markets activity has resumed with financings of junior gold miners increasingly linked to active exploration programs and not just balance sheet survival.

- Historically, M&A activity tends to accelerate when gold maintains new highs as producers look to replace declining reserves with acquisitions.

Company Overview — Golden Rapture Mining (CSE: GLDR)

Golden Rapture Mining is a Canadian junior gold explorer focused on advancing a number of properties in Ontario, Canada. The Company focuses on disciplined capital allocation, early stage exploration and minimizing dilution while leveraging discovery potential.

- Key asset: Phillips Township Gold Property (Ontario).

- Shares outstanding: Approximately 52.0 million shares post-financing.

The Company’s focus will be to advance priority targets at the Phillips Township Gold Property while preserving flexibility in the Company’s balance sheet.

Key Asset — Phillips Township Gold Property (Ontario)

The Phillips Township Gold Property is situated in a well-established gold trend in Ontario. The Property hosts numerous mineralized trends and documented historic workings and therefore provides a solid platform for systematic follow up work.

Multiple priority targets have recently been identified by the Company for further exploration and sampling. The size of the Property allows for staged exploration and development, thereby allowing the Company to pursue additional target areas without having to immediately commit large amounts of capital.

Recent Capital Markets Activity

On January 28th, 2026, Golden Rapture Mining announced that it had completed the final tranche of its non-brokered private placement for gross proceeds of approximately CAD $500,000. The financing was completed at CAD $0.04 per unit with each unit consisting of one common share and one common share purchase warrant exercisable at CAD $0.05 for a period of 24 months from the date of issue.

The net proceeds from the private placement will fund the Company’s exploration activities and provide operational runway for a number of months while limiting the need for near-term financing and maintaining the Company’s exposure to upside potential if exploration results are positive.

Why This Matters to Investors

Gold remaining above $5,000 per ounce greatly enhances the valuation model for junior explorers. Historically, in previous gold price cycles, this environment has favored companies that have active exploration programs and sufficient capital to produce news flow.

- Juniors generally outperform majors in late-cycle gold price environments as they benefit from discovery optionality.

- Recent financings indicate an improvement in risk appetite in the sector.

- As gold prices continue to rise, many junior valuations remain well below those seen during previous gold price cycles.

Risk Considerations

Investments in junior mining companies are inherently high-risk due to the uncertainty associated with exploration outcomes and the fact that positive sampling or early-stage results do not necessarily translate into a successful economic discovery. Additionally, future financings may result in shareholder dilution and stock prices of juniors may remain volatile or unconnected to fundamentals during times of poor market sentiment.

What to Remember

As gold is trading at a high of approximately $5,040 per ounce, the overall market environment for precious metal equities remains supportive. Junior gold miners are beginning the part of the cycle where operational and discovery leverage to gold prices increases at a faster rate than gold prices themselves.

Golden Rapture Mining offers exposure to this theme via a funded balance sheet, a defined flagship asset and an active exploration program. For risk tolerant investors, junior gold miners offer asymmetrical upside potential derived from both the success of discovery and/or the capital rotation to junior miners as well as the sustained strength in gold prices, and not solely as a function of market sentiment.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}