The gold price has moved into a structurally bullish position. As such, there is now a combination of factors driving the price of gold upward: macroeconomic pressures, changing central bank policies and persistent demand from sovereign entities.

Unlike previous cycles, this rally is not strictly speculative, but also includes elements of central bank action, real rate changes, and limited gold supply. The setup is favorable for sustained price appreciation and significant tail risk.

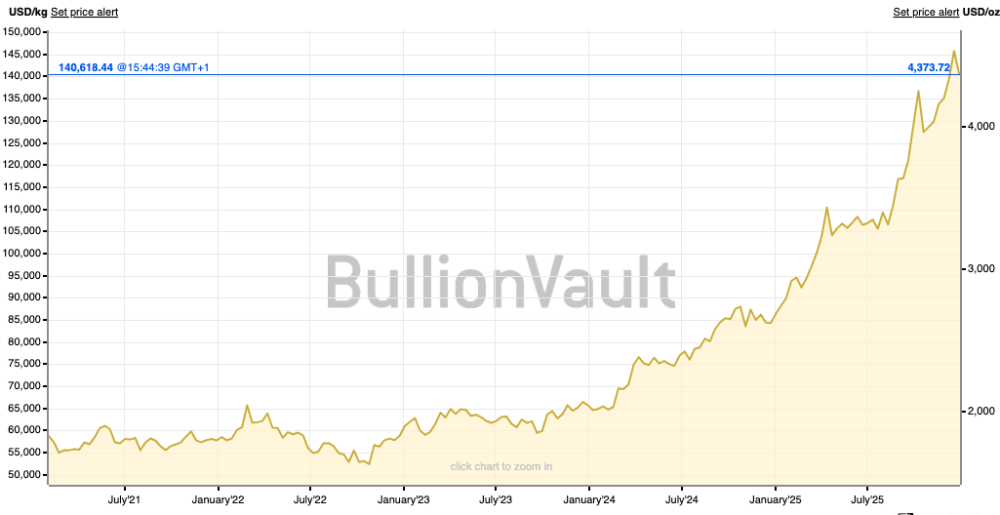

Facts and Figures (Data First)

- Current Gold Price: $4,420 – $4,550/oz (December 29, 2025 Range) — at/near record high levels

- Performance Year To Date (YTD): +70 – 72% (One of the top years for gold since 1979)

- Five-Year Performance: +135 – 140% (Spot Gold in USD)

- Total Central Bank Purchases: 2023 = 1037 tonnes / 2024 = 1045 tonnes

- Official Buyers: Broadly representative of EM-led demand (i.e., Poland is reportedly one of the biggest disclosed buyers; China reportedly added to reserves in 2024)

- Real Yields: UST 10yr TIPS — ~1.9 – 2.0% at the close of December 2025 (off previous peak)

- Interest Rate Outlook: Futures Markets — generally indicating multiple rate cuts will occur across 2026 (varies based upon data sets)

- Global Debt: Estimated ~$345.7 Trillion (IIF estimate — September 2025 End-of-period)

- Growth in Gold Mine Production: ~1 – 2% (Annual Growth Rate) — 2024 Mine Output Estimating ~3300 tonnes (versus ~3250 tonnes in 2023)

The Set Up

This bull market for gold is not due to speculative retail activity alone. Rather, it represents a collection of long-term structural factors which are increasingly recognized by policymakers, institutions, and industry experts:

- Monetary Policy: Declining real rates significantly enhance gold’s comparative advantage over cash and bonds. “Gold performs best when investors question the long-term ability of fiat currencies to maintain their purchasing power” is how one senior macro strategist at a large U.S.-based investment banking firm put it.

- Currency Dynamics: Long stretches of dollar weakness have historically correlated with multi-year gold bull markets, especially when capital seeks diversification out of dollar-denominated assets.

- Central Banks: Central banks are no longer buying gold tactically, but strategically building up gold as a reserve asset, making official sector buying a structural trend rather than a cyclical phenomenon, according to World Gold Council commentary.

- Geopolitics: Growing regional conflict and increasing fragmentation of the world create increasing demand for gold as a neutral, non-sovereign store of value.

- Supply Constraints: New gold discoveries are consistently smaller, deeper, and more capital intensive than past discoveries, reducing the speed at which the industry can react to increased prices.

When taken collectively, these structural factors indicate gold does not need ideal macroeconomic conditions to continue to appreciate — incremental changes in policy, currency dynamics, or risk perception can result in proportionally larger price movements.

Why It Matters

Gold typically reprices in discrete jumps, as opposed to continuous curves. When certain psychological barriers are broken, the way that capital allocators behave can change very quickly:

- Previous breakout levels to all-time highs have historically resulted in subsequent price movements of 30 – 50%, as institutional participation in gold increases.

- Historically, confirmation of easing cycles has triggered re-allocation of capital from bonds into tangible assets.

- Sharp inflows into gold-backed ETFs typically follow the establishment of positive momentum in gold, and amplify the potential for continued upside in the price of gold.

- Because the supply of gold from mines is relatively inelastic, even minor increases in investment demand will result in price appreciation.

Recent commentary from European central bankers increasingly frames gold not merely as a hedge, but as a confidence asset within the global monetary system. Therefore, gold is increasingly behaving not only as protection for investors, but as a means of enhancing performance within diversified portfolios.

Major Gold Companies: Positioned for Higher Gold Prices

Newmont Corporation (NYSE: NEM) produced 1.45 million ounces of gold in Q3 2025 and generated approximately $1.6 billion in free cash flow in Q3 2025, according to its latest available filings. Newmont has generated three consecutive quarters of free cash flow in excess of $1 billion, has reduced its long term debt by approximately $2 billion year-over-year, and maintains a quarterly dividend of $0.25 per share. As of the last report, Newmont had more than $5 billion in total liquidity, enabling the company to consider returning capital to shareholders and optimize its portfolio.

Agnico Eagle Mines Limited (NYSE/TSX: AEM) generated substantial free cash flow in 2025, including greater than $1 billion in a single quarter, while maintaining production growth from its core Canadian and international assets. Agnico continues to pay a quarterly dividend of approximately $0.40 per share, and has executed share repurchases under its normal course issuer bid in addition to executing other forms of balance sheet strengthening and cash accumulation.

Barrick Mining Corporation (NYSE: B / TSX: ABX) has experienced higher margins and therefore cash generation at its Tier 1 asset base, resulting from higher average prices for gold. Public disclosures from Barrick highlight a continuing emphasis on capital discipline, shareholder returns in the form of dividends, and targeted investment in long life assets capable of generating free cash flows through commodity cycles.

Junior Leverage: Golden Rapture Mining Corp.

Golden Rapture Mining Corp. (CSE: GLDR) is a micro-cap junior gold explorer with exposure to significant leverage to gold prices.

Snapshot:

- Stock Ticker: GLDR (CSE)

- Current Stock Price: ~C$0.05 (Late December 2025 Range)

- Market Capitalization: ~C$1.8 – 2.0 Million

Phillips Township Gold Property: The Phillips Township Gold Property is a district-scale land package containing numerous historical gold occurrences and high-grade surface samples in the Rainy River District of Northwest Ontario, which is the focal point of the Company’s exploration activities.

Sampling Results: Golden Rapture has released high-grade and locally bonanza-grade gold values from surface sampling programs conducted across its project area. Although the Company is in an early exploration phase and has not yet prepared or filed a NI 43-101 compliant resource estimate for any of its properties, the sampling results provide evidence of high-grade mineralization and establish the basis for prioritizing drill-ready targets.

Financing Catalyst: The Company recently closed a C$500,000 flow-through and non-flow-through financing transaction. The proceeds from this financing are being used to advance exploration work and prioritize drill-ready targets across the Company’s Ontario assets. This type of financing provides the necessary resources to continue exploration and serves as an indicator of investor willingness to fund risk at a time when the junior mining sector faces difficult conditions. Although early-stage exploration involves inherent uncertainty, accessing capital is essential to realize any upside from discovery-based activities.

Summary

Gold’s current price rise is due to structural, and not temporary, factors. Given the involvement of central banks, low real yields, and rising global risk, gold is well-positioned for additional price appreciation. Select junior miners with an active funding program and exploration efforts present an asymmetrical opportunity for investors, however they require careful risk management.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}