The next rate decision by the Bank of Canada on October 29, 2025 is likely to be among the most closely watched in years. Having cut the policy rate to 2.50% in September, traders now see close to a 77% chance of another cut, according to live data monitored on BankofCanadaOdds.com. With inflation remaining above target but growth slowing rapidly, markets will look for another balancing act from Governor Tiff Macklem and his team.

The Backdrop: Slowed Economy, Sticky Prices

Canada’s economy has clearly cooled. GDP contracted in Q2, and early data point to flat output in Q3. Inflation has hovered near 3.4%, above the 2% target. The BoC’s own surveys show falling business confidence and slowing wage pressures — classic preconditions for further rate relief.

Financial markets have been watching closely. The Canadian dollar recently slipped below 1.40 per USD, its weakest level in six months, reflecting soft domestic data and widening interest rate differentials with the U.S. dollar.

What the Odds Say

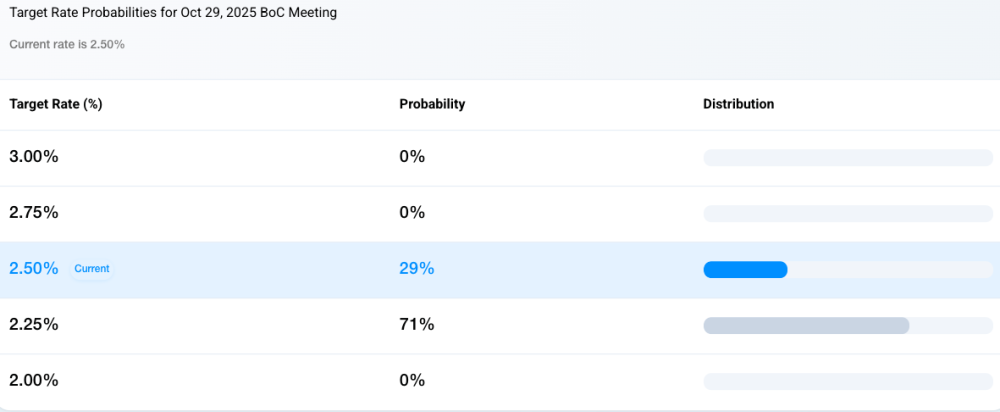

As of late October, swaps and OIS market futures suggest roughly a three-in-four (≈77%) chance of a 25-bp cut at the October 29 meeting, according to BankofCanadaOdds.com. Analysts from RBC, BMO, and CIBC are divided. RBC expects one final trim to 2.25%, calling it the last step of the easing cycle, while CIBC believes weak housing and retail data could push another cut in December.

If They Cut vs. If They Hold

If the BoC cuts, it would indicate the slowdown outweighs inflation risks. Mortgage borrowers would get modest relief on variable rates, but the broader signal would be that policy is turning more stimulative.

If the Bank holds, it would suggest policymakers remain cautious about rekindling inflation. Core measures like CPI-trim and CPI-median have proven sticky, and any energy rebound could complicate the path back to 2%. A hold at 2.50% would imply the BoC wants more data before easing further.

The Neutral Zone

The BoC’s neutral policy rate — one that neither accelerates nor slows the economy — is estimated between 2.25% and 3.25%. If a cut occurs in October, Canada would sit near the lower bound, giving policymakers space to pause while staying in the neutral zone.

What It Means for Canadians

It’s a big deal for households. Each 25-bp cut saves about $13 per $100,000 borrowed on a variable-rate mortgage. But savers would face smaller GIC returns. And for the loonie, more easing could add downside pressure unless global risk sentiment improves.

Bond markets are already pricing in a slower 2026 recovery, with five-year yields near 2.7%, down from 3.4% in July. Stocks, especially financials and REITs, could enjoy mild relief rallies if the BoC signals a near-term end to its cuts.

Looking Ahead

All eyes are now on the Monetary Policy Report released alongside the decision. The tone — whether focused on inflation risks or economic slack — will guide expectations for early 2026. Markets will also monitor November CPI and employment data for clues on when the slowdown warrants easing.

Bottom Line

The Bank of Canada’s October meeting isn’t just about another potential cut — it’s about setting the tone for 2026. A dovish stance would reassure markets that policy remains flexible; a cautious tone would reinforce that inflation is still a threat. Either way, as the daily odds tracked on BankofCanadaOdds.com make clear, every basis point now matters to households, investors, and policymakers.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}