- OKLO is being valued less on today’s revenue and more on the possibility that AI’s next bottleneck is electricity.

- Meta’s planned 1.2 GW Ohio project, NVIDIA collaboration, DOE progress, and HALEU fuel work have made Oklo one of the most controversial nuclear names on the market.

- The hot take: OKLO may not be the safest nuclear stock, but it may be one of the cleanest public-market ways to bet on AI-driven power demand.

Why OKLO Is Suddenly Everywhere

Oklo has become one of the most debated names in the AI infrastructure trade because investors are starting to move beyond chips and data centers. The next big question is power. AI models need GPUs, but those GPUs need electricity, cooling, grid access, backup capacity, and long-term energy reliability.

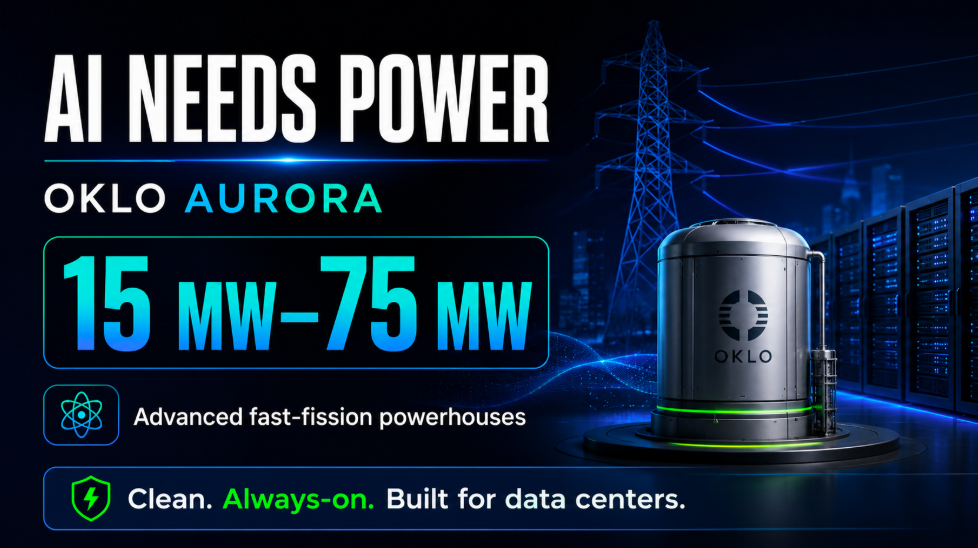

That is why OKLO has become a headline stock. Oklo is developing advanced fast-fission nuclear powerhouses designed to provide clean, always-on electricity for data centers, industrial users, government sites, and critical infrastructure.

The company’s Aurora powerhouses are often discussed in the 15 MW to 75 MW range, which makes the model very different from traditional large-scale nuclear plants. Instead of building only massive centralized reactors, Oklo is trying to commercialize smaller, advanced nuclear assets that could be deployed closer to energy-hungry customers.

That story fits perfectly with the market’s new obsession: AI needs power, and nuclear may become part of the solution.

The Hot Take

The hot take is simple: OKLO is not being valued like a normal company. It is being valued like a future infrastructure option.

The market is not paying for current earnings power. It is paying for the chance that Oklo becomes an early leader in advanced nuclear deployment at the exact moment AI data centers are fighting for reliable electricity.

That is why OKLO can look exciting and expensive at the same time.

Bulls see Meta, NVIDIA, DOE progress, domestic fuel supply, AI power demand, and a nuclear comeback. Bears see a company with a $10B+ market cap, limited current commercial power revenue, long timelines, regulatory complexity, construction risk, and a lot of future success already priced in.

Both sides have a point. That is what makes OKLO such a strong debate stock.

The Stock Snapshot

OKLO recently traded around $61 per share, with a market cap of roughly $10B+. That valuation changes the conversation.

At this level, the stock is not being treated like a small speculative nuclear startup. Investors are already giving Oklo credit for becoming one of the leading advanced nuclear players in the AI power cycle.

That creates a higher bar. A company valued above $10 billion before scaled commercial power revenue needs to keep delivering meaningful milestones. The market will want to see progress on licensing, fuel, site development, customer agreements, financing, construction, and eventual power sales.

The story is strong, but the valuation means execution matters more with every new headline.

Why AI Power Demand Changes the Story

For most of the AI boom, investors focused on semiconductors, cloud providers, networking, and data centers. Now the conversation is shifting deeper into the infrastructure stack.

AI data centers need constant electricity. They cannot rely only on intermittent power sources if they want 24/7 compute availability. Solar and wind can support the grid, but they do not fully solve baseload reliability. Natural gas is flexible, but it brings emissions and fuel-price exposure. Nuclear offers always-on clean power, which explains why hyperscalers are paying closer attention.

This is where OKLO becomes interesting. The stock is not just a nuclear trade. It is a way to bet that AI demand forces large technology companies to secure long-term, clean, reliable electricity at scale.

That is the core reason the stock keeps getting attention.

Meta Is the Biggest Validation Point

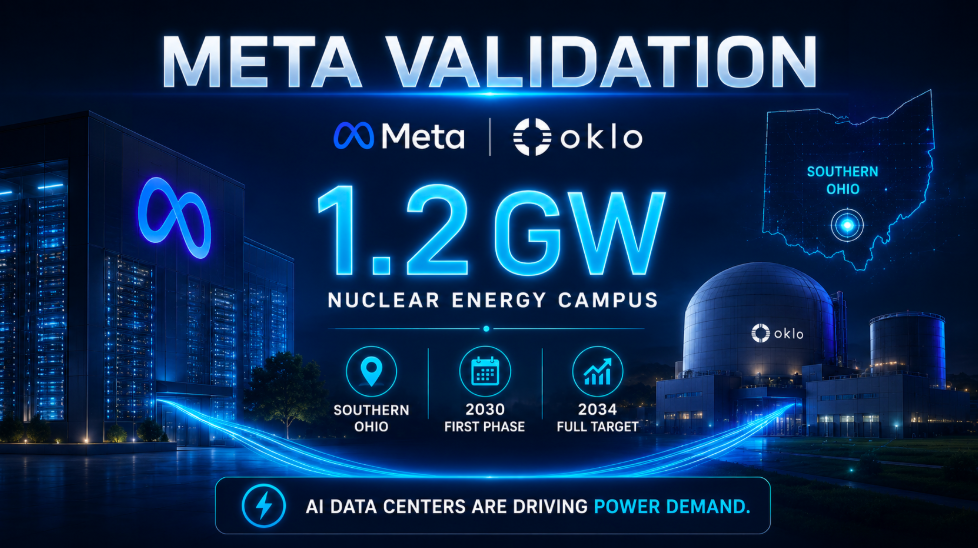

The Meta agreement is the most important commercial signal in the Oklo story.

Oklo and Meta announced support for a planned 1.2 GW nuclear energy campus in southern Ohio, intended to support Meta’s regional data-center operations. The first phase is targeted to come online as early as 2030, with expansion toward the full 1.2 GW target by 2034.

That timeline is long, but the size matters.

A 1.2 GW power campus is not a small pilot. It is a serious capacity target tied to one of the largest AI and cloud infrastructure companies in the world. For investors, the Meta agreement helps validate the idea that Big Tech is actively looking at nuclear power as part of the AI energy solution.

The key issue is timing. If the first phase does not arrive until 2030, OKLO investors are betting several years ahead of commercial proof. That makes the upside story powerful, but also increases patience risk.

The NVIDIA Angle Makes the Story More Viral

The NVIDIA connection gives OKLO a stronger market narrative.

Oklo announced a collaboration with NVIDIA and Los Alamos National Laboratory focused on nuclear fuel validation, AI-enabled research, digital twins, modeling, simulation, and nuclear-powered AI infrastructure.

That is why the update resonated with investors. NVIDIA is the face of the AI boom, while Los Alamos adds technical and national-lab credibility. Together, the collaboration connects Oklo to AI infrastructure, advanced nuclear development, and high-performance computing.

It does not mean NVIDIA is guaranteeing Oklo’s success. It does not mean commercial reactors arrive tomorrow. But from a market-perception standpoint, the association matters because it links OKLO directly to the broader AI infrastructure ecosystem.

DOE and Fuel: The Execution Side of the Story

Nuclear is not software. You cannot just launch a product, update it, and scale it overnight. Advanced nuclear requires regulatory progress, safety reviews, fuel availability, site readiness, construction capability, and long-term customer contracts.

That is why Oklo’s DOE and fuel milestones matter.

In June 2026, the U.S. Department of Energy approved the Preliminary Documented Safety Analysis for Oklo’s Aurora powerhouse at Idaho National Laboratory. This is not full commercial deployment, but it is an important step in the project-development pathway.

Fuel is another major piece. Oklo also announced a letter of intent with Centrus Energy for HALEU supply expected to begin in 2029, with enough fuel to support up to five Aurora powerhouses for multiple years.

That matters because HALEU supply is one of the biggest bottlenecks for advanced nuclear. If Oklo can secure reliable domestic fuel, the deployment roadmap becomes more credible. Without fuel, even strong customer demand is not enough.

The Bear Case: The Valuation Is Already Pricing a Lot

The bear case is not complicated. OKLO may have one of the best stories in the market, but the stock has already moved into a valuation zone where expectations are high.

A $10B+ market cap for a company still years away from scaled commercial power revenue means investors are paying upfront for future execution. That creates downside risk if timelines slip, regulatory approvals slow down, fuel supply becomes harder, financing becomes expensive, or customer agreements take longer to become binding.

The Meta-supported Ohio project may start site work in 2026, but the first phase is targeted for 2030, and the full 1.2 GW goal stretches toward 2034. The Centrus HALEU supply is expected to begin in 2029. That means the OKLO story is exciting, but it is also long-dated.

That is why bears argue that the company may be directionally right while the stock may still be too aggressive.

Why Bulls Still Care

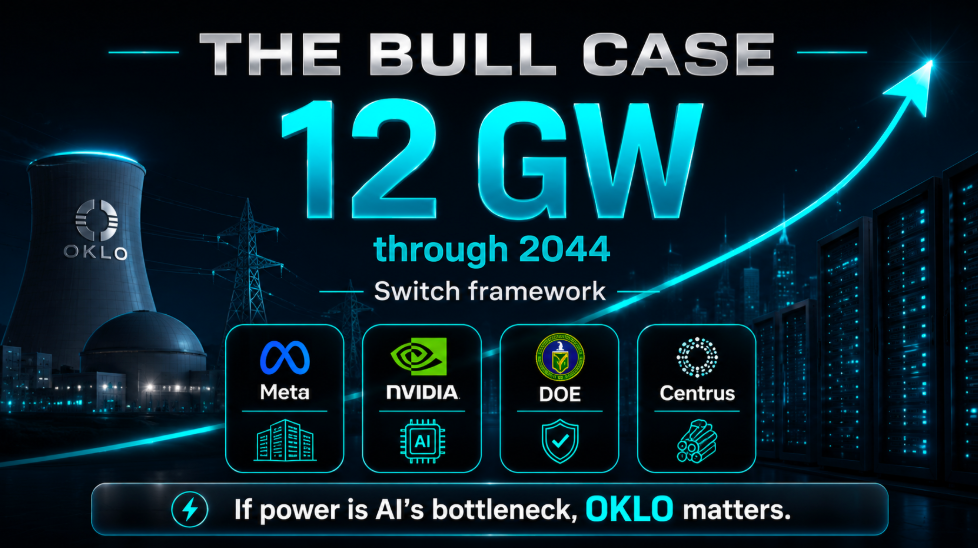

Bulls keep coming back to OKLO because the company sits at the intersection of several major market themes at once: AI electricity demand, nuclear power, energy security, Big Tech data centers, domestic fuel supply, and government-backed infrastructure.

That combination is rare.

The Switch framework for up to 12 GW of advanced nuclear power through 2044 adds another long-term demand signal. The Meta agreement adds hyperscaler validation. The NVIDIA collaboration adds AI credibility. The DOE milestone adds regulatory momentum. The Centrus agreement adds fuel-supply progress.

None of these pieces alone guarantees success. But together, they create a powerful narrative that Oklo could become one of the more visible public-market names in advanced nuclear power.

That is the bull case: if electricity becomes AI’s next bottleneck, OKLO could become much more important.

Timeline: What Investors Are Watching

Oklo was founded in 2013 and went public in 2024 after completing its business combination with AltC Acquisition Corp. That same year, Oklo and Switch announced a non-binding framework for up to 12 GW of advanced nuclear power through 2044, giving investors a first major sense of the long-term scale the company is trying to target.

The story accelerated in 2026. In January, Oklo and Meta announced support for a planned 1.2 GW nuclear power campus in southern Ohio. In April, Oklo announced its collaboration with NVIDIA and Los Alamos. In June, the DOE approved the Preliminary Documented Safety Analysis for Aurora, and Oklo also announced the Centrus HALEU fuel-supply letter of intent.

The next key dates matter. Centrus fuel supply is expected to begin in 2029. The first phase of the Meta-supported Ohio project could come online as early as 2030. The full 1.2 GW target could be reached by 2034.

That gives investors a clear timeline, but also a clear warning: this is not a quick execution story.

Forecast: What Has to Go Right

For OKLO to justify the current excitement, the company needs to move from headline validation to execution validation.

The most important milestones are clear: the DOE process needs to keep moving, Aurora deployment timelines must remain credible, the Centrus fuel plan needs to become real supply, the Meta project needs to advance beyond agreement language, and Oklo needs to show how financing, construction, and commercial power sales will work.

The market will likely become less patient over time. Early-stage investors may reward big partnerships and strategic headlines. But as the valuation rises, investors will demand more detailed proof: firm contracts, customer economics, capital requirements, project timelines, and eventually operating assets.

That is the transition OKLO has to make.

Investor Debate: Nuclear Company or AI Infrastructure Stock?

The real debate is whether OKLO should be valued as a nuclear developer or as an AI infrastructure company.

If investors treat it as a pre-commercial nuclear developer, the stock can look expensive. If investors treat it as a scarce public-market way to play AI power demand, the premium becomes easier to understand.

That is why the stock divides people online.

The same numbers can support two completely different views. A $10B+ valuation with limited current revenue looks dangerous to traditional investors. But a potential role in powering AI data centers through projects measured in gigawatts looks attractive to thematic growth investors.

That disagreement is the story.

Bottom Line

OKLO is one of the most controversial AI infrastructure stocks because the company is being valued on what it could become, not what it is today.

The bullish case is powerful: AI needs massive reliable electricity, nuclear is becoming strategic again, Meta’s 1.2 GW project validates the demand story, NVIDIA adds AI credibility, DOE milestones are moving, and the Centrus fuel agreement could help address one of the biggest industry bottlenecks.

The bearish case is just as clear: OKLO already carries a $10B+ market cap, commercial deployment is still years away, the Meta timeline stretches toward 2030–2034, fuel supply is not expected until 2029, and advanced nuclear execution risk remains high.

The hot take is this: OKLO may not be the safest nuclear stock, but it may be one of the cleanest public-market ways to bet that AI’s next bottleneck is electricity.

That is why the stock keeps getting attention — and why the debate is not going away.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}