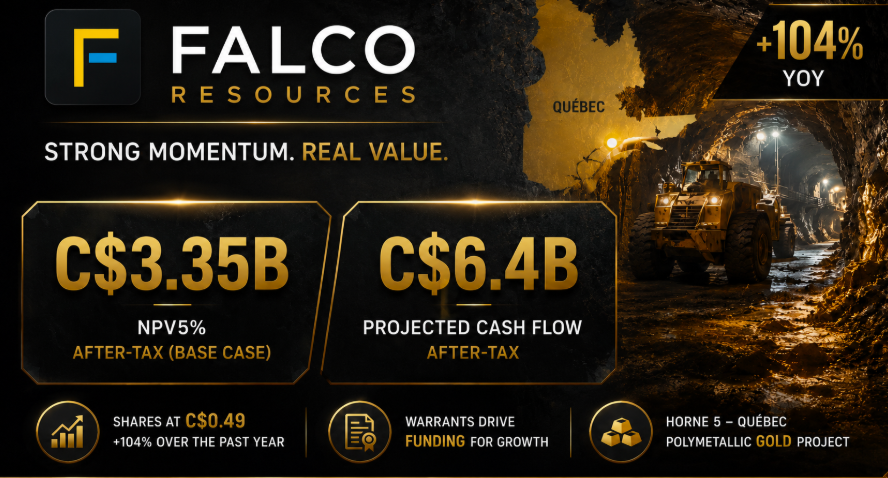

- Falco Resources has strong stock momentum, with shares recently at C$0.49, up 104.17% over the past year.

- The warrant exercise story is simple: warrant holders can buy shares at a fixed price, and when they exercise, Falco receives cash that can help fund project advancement.

- The bigger story remains Horne 5, a Québec polymetallic gold project with an updated after-tax NPV5% of C$3.35B, 28.2% IRR, and projected C$6.4B after-tax cash flow.

The Simple Version

Falco Resources has been quietly building momentum.

The stock recently traded at C$0.49, up 104.17% over the past year, with a market cap of about C$171.67M. Its 52-week range is also important: the stock has moved from a low of C$0.22 to a high of C$0.64, meaning investors have already started repricing the story.

The latest news around warrant exercise adds another layer.

For many retail investors, warrants can sound confusing. But the basic idea is simple.

A warrant gives the holder the right to buy shares at a fixed price. If the stock trades above that price, the warrant can become attractive to exercise. When the holder exercises, the company issues shares and receives cash.

So for Falco, warrant exercise is not just a technical financing detail.

It can be a signal that holders are willing to put more capital into the company, while also giving Falco additional cash to keep advancing its flagship project.

That matters because Falco is not just sitting on a small exploration story. It is advancing one of Canada’s more important undeveloped polymetallic gold projects.

What Is a Warrant Exercise?

A warrant is basically a long-dated option issued by a company.

It gives the holder the right to buy a share at a set price before a set deadline.

For example, Falco’s October 2025 bought deal financing included warrants exercisable at C$0.46 per share until April 17, 2027. With the stock recently around C$0.49, those warrants are close to being in-the-money, meaning the market price is slightly above the exercise price.

That is why warrant activity becomes relevant.

If a warrant holder exercises at C$0.46, Falco receives C$0.46 in cash for each share issued. The warrant holder receives a share. The company gets funding without having to launch a brand-new financing.

For investors, there are two sides.

- The positive side is that warrant exercises bring cash into the company.

- The negative side is that new shares are issued, which creates dilution.

But in a development-stage mining company, dilution is not always bad if the cash helps move a valuable project forward. The real question is whether the company uses that capital to unlock more value than the dilution costs.

Why the Timing Matters

The warrant news comes at an interesting moment because Falco already has momentum.

- recent price: C$0.49

- 1-year performance: +104.17%

- market cap: C$171.67M

- 52-week high: C$0.64

- 52-week low: C$0.22

- no dividend

- no P/E ratio shown

That is a strong move, but the stock is still below its 52-week high.

From C$0.49 to the 52-week high of C$0.64, the stock would need to rise about 30%. From the 52-week low of C$0.22, the stock has already more than doubled.

That makes Falco a momentum story, but not one sitting at an all-time extreme on this chart. The key reason investors are paying attention is the Horne 5 Project.

The Real Asset: Horne 5

Falco’s main asset is the 100%-owned Horne 5 Project in Rouyn-Noranda, Québec.

This is not just a conceptual exploration target. Horne 5 is an advanced underground gold-rich polymetallic development project located below the historic Horne mine, in one of Canada’s most established mining districts. Falco describes Horne 5 as one of the most advanced undeveloped polymetallic assets in Canada.

The updated feasibility study released in June 2026 is the main reason the story has become much more interesting.

The 2026 feasibility study showed:

- after-tax NPV5% of C$3.35B

- after-tax IRR of 28.2%

- payback period of 3.3 years

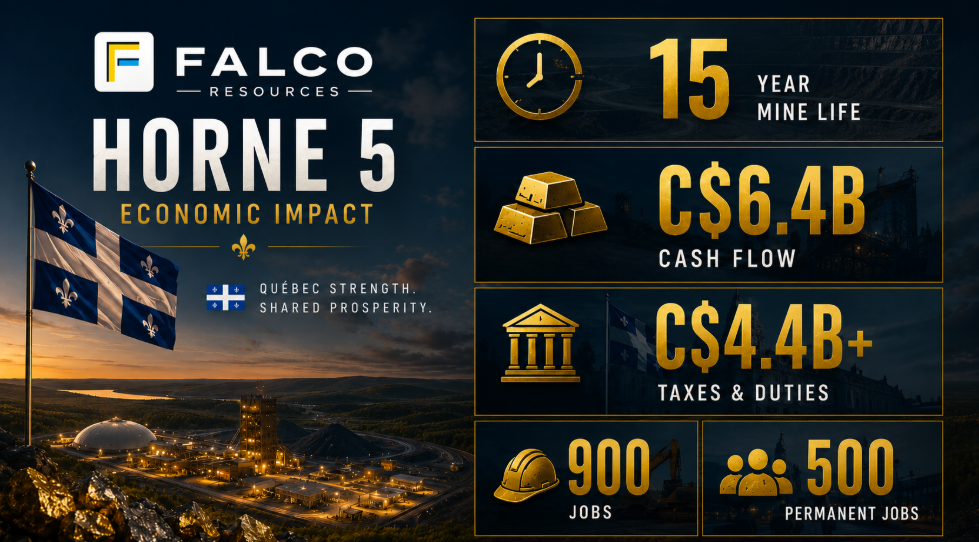

- projected after-tax cash flow of C$6.4B

- average annual after-tax cash flow of C$542.5M

- average annual gold production of 220,300 oz

- mine life of 15 years

- average AISC of US$782/oz

- forward capital and pre-production costs of C$1.75B

The economics are meaningful because Falco’s market cap is around C$171.67M. Compared with the base-case after-tax NPV5% of C$3.35B, the market cap represents only about 5% of the project’s reported after-tax NPV. Put differently, the project NPV is roughly 19.5x the current market cap.

That does not mean the stock should automatically trade at NPV.

Mining developers almost never do before financing, permitting, construction, and execution are solved.

But it does show why the valuation gap exists.

Why the Feasibility Study Changed the Story

The 2026 feasibility study made the project look much stronger than before.

Mining Weekly reported that Horne 5’s updated base-case after-tax NPV of C$3.35B represented a 244% increase compared with the 2021 feasibility study. Using spot-case assumptions, the after-tax NPV increases to C$5.1B, the IRR rises to 37.2%, and the payback period falls to 2.6 years.

This matters because Falco is not only a gold story.

Horne 5 is polymetallic.

That means the project has exposure to gold, silver, copper, and zinc. The company’s project materials say Horne 5 could produce 3.3M oz of gold, 247M lb of copper, 27.3M oz of silver, and 1.19B lb of zinc over its 15-year mine life.

That gives Falco multiple commodity drivers.

Gold brings the precious-metals angle.

Copper and zinc bring the critical-minerals and energy-transition angle.

Why the Warrant Exercise Is Actually Useful

For a company like Falco, the biggest question is not whether the project looks good on paper.

The question is how it moves toward construction.

Large mining projects require capital, permitting, technical work, community engagement, and government approvals. Horne 5’s forward capital and pre-production costs are estimated at C$1.75B, which is far larger than Falco’s current market cap.

That is why every source of capital matters.

A warrant exercise can help in three ways.

First, it brings cash into the company without launching a new financing round.

Second, it can show confidence from warrant holders who are willing to convert their rights into shares.

Third, it helps support ongoing work around permitting, technical studies, engineering, and general corporate needs.

The trade-off is dilution.

Every exercised warrant creates a new share. But for a development-stage miner, the market may accept dilution if it moves the project closer to a value-creating milestone.

That is why the warrant exercise should be seen as a funding signal, not just a share-count issue.

The Momentum Setup

Falco’s chart now shows real momentum.

A 104.17% year-over-year move is not small. It tells investors that the market has started to recognize something in the story.

But the stock is still in an interesting zone.

At C$0.49, Falco is:

That creates a clear but risky setup.

The bull case is that Falco is still undervalued relative to the scale of Horne 5.

The bear case is that the market is applying a big discount because permitting, financing, construction, and execution risk remain substantial.

Both views can be true at the same time.

Upcoming Catalysts

Falco already laid out its key priorities for 2026.

The company said its priorities include advancing Horne 5 toward receipt of the Québec ministerial decree, completing the feasibility study update, continuing technical and permitting work, expanding institutional and analyst engagement, advancing community consultation, and maintaining transparent communication with shareholders.

The feasibility study update is now complete.

That means investors are likely watching the next steps.

Key catalysts include:

- Québec ministerial decree progress

- permitting updates

- financing strategy

- additional technical work

- institutional interest

- analyst coverage

- community consultation progress

- project financing discussions

- gold, silver, copper, and zinc price strength

- additional warrant exercises or balance sheet improvements

The biggest catalyst is the Québec authorization path.

If Falco gets closer to full approval and financing, the valuation gap could narrow.

If timelines stretch, the stock could lose momentum.

Why Investors Care About the Québec Angle

Location matters.

Horne 5 is in Rouyn-Noranda, Québec, a historic mining region with existing infrastructure, skilled labor, local suppliers, and nearby mining expertise.

Falco’s project materials also highlight that Horne 5 would use already impacted sites, including an underground mine below the former Horne mine, a mining complex at the former Quemont site, and a tailings facility at the former Norbec site.

That matters because mining projects face increasing scrutiny over footprint, permitting, social acceptance, and environmental impact.

Falco’s pitch is that Horne 5 can benefit from existing infrastructure and already impacted sites rather than starting from zero in a remote greenfield area.

The company also highlights community engagement, with more than 95 consultation and information meetings held since 2014.

That does not eliminate permitting risk.

But it gives the company a stronger narrative around social license and project integration.

The Bigger Economic Impact

Horne 5 could also become a major economic project for Québec.

The updated feasibility study says the project could contribute more than C$4.4B in taxes and mining duties over its lifetime. It could also support up to 900 direct jobs during construction and 500 permanent jobs during operations.

Those numbers matter because governments do not approve mining projects only based on geology.

They also care about jobs, taxes, regional development, environmental standards, and local impact.

A project with:

has a much stronger political and economic case than a smaller speculative exploration project.

That is part of why Falco is worth watching.

The Bull Case

The bull case is that Falco is entering a more important stage.

The stock is up more than 100% year over year, but the company’s market cap remains small compared with the reported project economics.

Horne 5 has:

- scale

- a 15-year mine life

- strong feasibility economics

- gold production above 220,000 oz/year

- polymetallic exposure

- existing regional infrastructure

- Québec mining jurisdiction

- major tax and employment potential

- upcoming permitting and financing catalysts

The warrant exercise news adds another supportive point: the market is no longer ignoring Falco, and capital is starting to matter as the company moves from study-stage valuation toward development-stage execution.

The Bottom Line

Falco Resources Ltd. (TSX-V: FPC) is a high-momentum developer with a large, valuable project but still faces key risks around permitting, financing, and execution. The opportunity lies in the valuation gap between its current market cap and the substantial economics outlined for Horne 5, while the warrant exercise highlights improving access to capital as the story advances and signals growing investor confidence.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. Mining development stocks are speculative and may involve substantial volatility, financing risk, dilution risk, permitting risk, commodity price risk, and potential loss of capital. Always conduct your own research and consult a licensed financial advisor before making investment decisions.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}