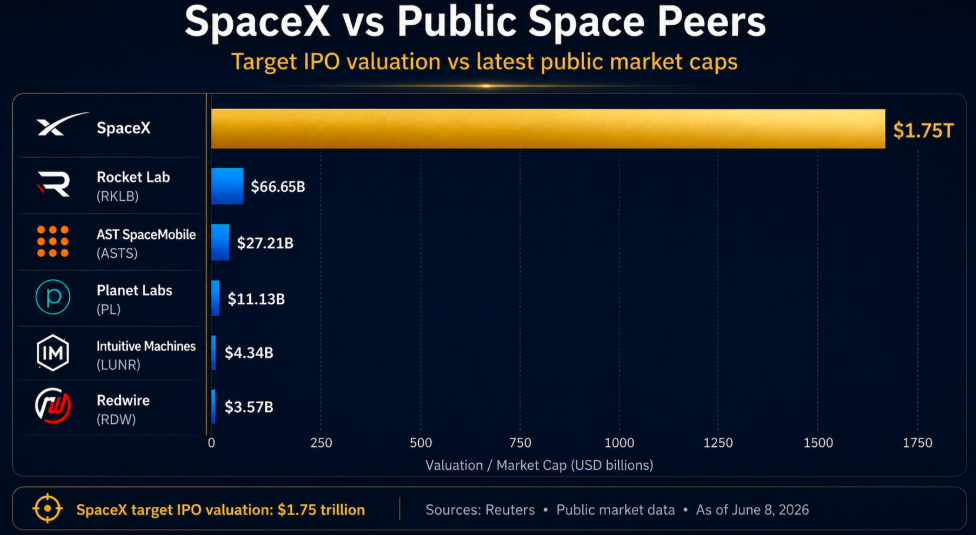

- SpaceX is reportedly targeting a $1.75 trillion IPO valuation at $135 per share.

- The bull case rests on Starlink, launch dominance, defense contracts, AI infrastructure, and Elon Musk’s founder premium.

- The bear case is simple: even great companies can become bad investments if the entry price is too high.

SpaceX may be the most important private technology company in the world.

It dominates commercial rocket launches, operates Starlink, has become deeply embedded in U.S. defense and space infrastructure, and is now positioning itself around artificial intelligence infrastructure. For years, public-market investors have asked the same question: when will SpaceX finally IPO?

Now the answer appears to be: soon.

According to Reuters, SpaceX is targeting a valuation of roughly $1.75 trillion in a record initial public offering. The deal is expected to raise at least $75 billion, with all proceeds going to the company rather than existing shareholders selling into the IPO. Reuters also reported that SpaceX plans to set the IPO price at $135 per share and sell about 555.6 million shares, with the stock expected to trade under the ticker SPCX.

That would instantly make SpaceX one of the largest public companies in the world.

But that is exactly why the IPO has sparked so much debate.

The question is no longer whether SpaceX is a great company. The question is whether public investors are being asked to pay too much, too early, for a story that still depends on several future businesses working at massive scale.

The Numbers Behind the IPO

The headline numbers are enormous.

| Metric | Reported Figure |

|---|---|

| Proposed IPO price | $135 per share |

| Shares expected to be sold | ~555.6 million |

| IPO proceeds | ~$75 billion |

| Target valuation | ~$1.75 trillion |

| 2025 revenue | ~$18.67 billion |

| 2025 net loss | ~$4.94 billion |

| Morningstar fair-value estimate | ~$780 billion |

At $1.75 trillion, SpaceX would trade at roughly 94 times 2025 revenue of $18.67 billion.

That is not a normal aerospace multiple. It is not even a normal satellite-internet multiple. It is a mega-cap technology, AI, infrastructure, space, defense, and Elon Musk premium all compressed into one stock.

This is the heart of the debate.

Bulls argue SpaceX is not a traditional aerospace company. They see it as a vertically integrated platform controlling launch, satellite broadband, defense infrastructure, AI compute, and eventually space-based data centers.

Bears argue that public investors are being asked to value not only what SpaceX is today, but also what it might become over the next 10 to 20 years. Some investors worry that IPO buyers could end up paying peak optimism prices, effectively funding expectations that may take years to materialize.

Starlink Is the Core of the Bull Case

Starlink is the cleanest part of the SpaceX IPO story.

SpaceX’s launch business is strategically important, but Starlink is the segment investors can understand most easily: recurring revenue, global subscribers, internet access, enterprise customers, aviation, maritime, and government use cases.

Reuters reported that Starlink is SpaceX’s only profitable segment, while other businesses are still burning cash. That matters because Starlink is the bridge between SpaceX as a capital-intensive rocket company and SpaceX as a scalable technology platform.

The Starlink bull case is based on several points:

- Global broadband access remains underpenetrated.

- Satellite internet can serve remote, maritime, aviation, military, and emergency markets.

- SpaceX controls launch costs better than competitors.

- More satellites can improve coverage, latency, and capacity.

- Enterprise and government contracts could increase average revenue per user.

This makes Starlink the part of SpaceX that investors can most easily value.

If Starlink becomes a global telecom-infrastructure platform, then a large valuation premium may be justified. If Starlink growth slows or margins disappoint, the $1.75 trillion IPO valuation becomes much harder to defend.

The AI Angle Changes the Story

The IPO is not only about rockets and satellites anymore.

Reuters reported that SpaceX merged with Musk’s AI startup xAI in a deal that valued SpaceX at $1 trillion and xAI at $250 billion. The filing also showed large AI infrastructure commitments, including a deal for Anthropic to pay SpaceX $1.25 billion per month for access to compute capacity through May 2029.

This gives the IPO a new narrative: SpaceX is not just a space company; it is also becoming an AI infrastructure company.

That is powerful for market sentiment.

AI infrastructure remains one of the biggest investment themes in the market. Data centers, compute clusters, GPUs, power demand, and sovereign AI capacity have driven huge valuations across the technology sector. If investors begin to value SpaceX as a space-based AI infrastructure company, the upside narrative expands dramatically.

But this is also where the risk increases.

Morningstar valued SpaceX at about $780 billion, less than half the reported IPO target, partly because it questioned the economics of SpaceX’s AI ambitions and untested technologies such as orbital data centers. That gap between $780 billion and $1.75 trillion is the valuation debate in one number.

The Governance Risk Is Real

SpaceX is also coming public with governance issues that investors cannot ignore.

Reuters reported that SpaceX will use a dual-class share structure, with Class B shares carrying 10 votes each and Class A shares carrying one vote each. This concentrates control with Elon Musk and insiders.

Reuters also reported that the company has adopted provisions that limit shareholder rights and protect Musk’s position. In practical terms, public investors may get economic exposure, but limited control.

For some investors, that is acceptable. They are buying the Musk premium and do not want a normal committee-run company.

For others, this is a major red flag. If the stock trades poorly, if capital allocation becomes controversial, or if AI spending balloons, public shareholders may have little ability to influence the company.

Why the Market Is Split

The debate around SpaceX is intense because it sits at the intersection of several powerful themes: Elon Musk, space exploration, AI, defense technology, and the possibility of another transformational growth story.

Supporters argue that traditional valuation metrics fail to capture what SpaceX could become. Critics counter that extraordinary businesses can still be poor investments when investors pay too much upfront.

A common concern among skeptics is that IPOs often arrive at valuations designed to maximize proceeds for the company. Others worry that enthusiasm surrounding the listing could push investors to focus more on the story than on the underlying financials.

This divide matters because the IPO may trade less like a normal listing and more like a sentiment event.

If retail enthusiasm, index speculation, and Musk loyalty dominate early trading, the stock could open strong and trade above its IPO price quickly.

If institutions push back on valuation or demand fades after the initial excitement, SpaceX could become one of the most volatile mega-cap IPOs ever.

Where Could SpaceX Stand After IPO?

Using the reported $135 IPO price and roughly $1.75 trillion valuation, investors can build a rough valuation map.

| Valuation Scenario | Implied Price Range | Interpretation |

| Morningstar case | ~$60 per share | Large downside if market reprices toward fair value |

| $1 trillion case | ~$77 per share | Still a mega-cap, but far below IPO target |

| $1.25 trillion case | ~$96 per share | More balanced high-growth case |

| IPO target | $135 per share | Current reported deal price |

| Momentum case | $150–$175 per share | Hype, low float, retail demand, index speculation |

| Extreme bull case | $200+ per share | Market treats SpaceX like a Tesla-style AI/space platform |

The most realistic short-term outcome may not be based on fundamentals.

Because the float may be limited and demand is expected to be extremely high, SpaceX could trade well above $135 in the first sessions. Reuters reported strong demand and a highly unconventional IPO structure, including a large retail allocation. That can create a powerful short-term squeeze higher.

But the longer-term question is different.

If investors eventually value SpaceX based on earnings, cash flow, Starlink margins, AI economics, and capital intensity, the stock may need years of execution to justify a $1.75 trillion starting point.

Bull Case

The bull case is that SpaceX deserves to be valued unlike any other public company.

SpaceX has advantages that are extremely difficult to replicate:

- Rocket reusability and launch-cost leadership.

- Deep relationships with NASA, defense agencies, and governments.

- Starlink’s global satellite broadband network.

- Vertical integration across launch, satellite manufacturing, software, and services.

- Potential AI infrastructure upside.

- A founder premium attached to Elon Musk.

- A retail investor base that may support the stock similarly to Tesla.

In this scenario, SpaceX could trade above the IPO price and remain expensive for a long time. The company may not need to look cheap if investors believe it is building infrastructure for the next era of space, communications, and AI.

Bear Case

The bear case is that SpaceX is an incredible company at an extreme price.

At nearly 94 times 2025 revenue, the market would already be discounting massive future success. The company posted a net loss in 2025, and several of its most exciting narratives remain uncertain, especially AI compute and orbital data centers.

There are also risks around:

- Starlink competition and capacity limits.

- Heavy capital expenditures.

- AI infrastructure losses.

- Launch failures or Starship delays.

- Political and regulatory pressure.

- Musk key-person risk.

- Corporate governance.

- Retail-driven volatility.

- Post-lockup selling pressure.

The bear case does not require SpaceX to fail. It only requires the stock to be priced too aggressively at IPO.

Bottom Line

SpaceX is likely to be one of the most important IPOs in market history.

The company has real strategic assets, real revenue, launch dominance, Starlink, government relationships, and a founder who has already created one of the most powerful retail-investor stories of the last two decades.

But the valuation is the problem.

At a reported $1.75 trillion IPO valuation, public investors are not being offered a cheap entry into SpaceX. They are being asked to pay upfront for a future where Starlink scales globally, AI infrastructure works, orbital compute becomes real, launch economics keep improving, and SpaceX maintains its dominance for years.

For short-term traders, the IPO could be explosive because of hype, limited float, retail access, and index speculation.

For long-term investors, the more disciplined approach may be to watch the first few quarters as a public company, track Starlink profitability, monitor AI losses, and wait to see whether the stock offers a better entry after the initial excitement fades.

SpaceX may be a generational company.

That does not automatically make the IPO a generational buy.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}