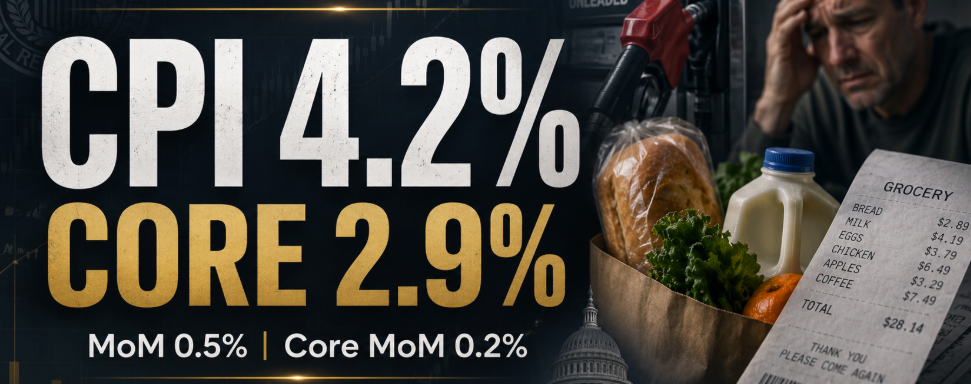

- U.S. CPI rose 4.2% year-over-year in May, with monthly inflation up 0.5%.

- Energy commodities surged 40.6% year-over-year, turning the Iran conflict into a direct inflation story.

- AI and semiconductor stocks are no longer trading in a vacuum: higher inflation, higher oil, and higher-rate risk are now testing the market’s favorite trade.

The latest CPI report did not just give investors another inflation number. It exposed the uncomfortable reality behind this market: inflation is still hot, the Fed is boxed in, Trump wants stocks higher, and the entire AI-led bull market is now depending on one dangerous assumption — that oil, war risk, and energy inflation will calm down before they spread deeper into the economy.

In May, U.S. consumer prices rose 4.2% year-over-year and 0.5% month-over-month, while core CPI rose 2.9% year-over-year and 0.2% month-over-month. Bulls immediately pointed to the calmer core number as proof that inflation is still “manageable,” but that argument becomes much harder when headline CPI is running at more than double the Fed’s 2% target and energy commodities are up 40.6% from a year ago.

The market’s problem is simple: investors want rate cuts, Trump wants a stronger stock market, consumers want cheaper prices, and the Fed wants credibility. The CPI report suggests not everyone can get what they want.

The Market Reaction: Calm on the Surface, Stress Underneath

The initial market reaction looked controlled, but the numbers tell a more fragile story. After the CPI release, major market ETFs were lower in midday trading: the QQQ was down about 0.9%, the SPY was down about 0.8%, and the DIA was down about 1.1%. That is not a crash, but it is not exactly a victory lap either.

The bigger story is what happened under the surface. Nvidia traded near $203.32, down about 2.3%, while AMD fell roughly 3.1%, Broadcom dropped about 4.3%, and the VanEck Semiconductor ETF, SMH, was down about 1.9%. Microsoft was down only 0.3%, but Amazon fell around 1.9%, Alphabet declined roughly 1.1%, and Meta was down about 1.0%.

That matters because AI and semiconductors have been the market’s leadership group. When inflation shocks hit consumer staples, nobody panics. When they hit Nvidia, AMD, Broadcom, and the semiconductor complex, investors start asking whether the most crowded trade in the market is becoming vulnerable.

Semiconductors Are the Real Stress Test

The semiconductor sector is where this CPI report becomes more than a macro story. Just days before the CPI print, U.S.-traded chipmakers suffered a brutal selloff that erased roughly $1.3 trillion in market value. The PHLX Semiconductor Index fell 10.3% in its deepest one-day drop since March 2020, and the pain hit AI-linked leaders including Nvidia, AMD, and Micron.

Yes, chip stocks rebounded afterward. The SOX jumped 5.6% on June 8 as investors tried to buy the dip and defend the AI trade. But that is exactly the point: this is now a market swinging between “AI changes everything” and “higher rates change valuations.”

That is why CPI matters so much for tech. Nvidia still carries a market capitalization near $4.96 trillion, AMD sits around $759 billion, Intel is near $545 billion, and the AI ecosystem remains priced for massive future growth. But when inflation stays sticky, discount rates stay higher, and long-duration growth stocks become harder to justify at extreme valuations.

The controversial question is whether AI is strong enough to beat inflation — or whether the market has simply convinced itself that AI stocks are immune to macro gravity.

The Iran War Premium Is Now an Inflation Premium

The most dangerous part of the CPI report is energy. Brent crude rose 1.6% to $92.90, while WTI climbed about 2% to $90 after Trump warned that Iran “must pay the price” and tensions around the Strait of Hormuz remained elevated. U.S. crude inventories also dropped by 7.2 million barrels, much more than expected, adding another layer of pressure to oil prices.

This is not just a commodity story. It is a direct CPI story.

When oil rises, it hits gasoline, trucking, airlines, shipping, food distribution, industrial costs, and household budgets. Gasoline is not some abstract input in an economist’s model; it is one of the prices voters see every week. That is why energy inflation is so politically explosive.

The market wants to believe the Iran conflict is temporary. But if the war premium stays in crude oil, inflation may stay higher for longer, and the Fed may have even less room to cut rates. That is the uncomfortable scenario investors do not want to price: geopolitical inflation colliding with an already expensive stock market.

Trump Wants Stocks Higher, But CPI Does Not Care

Trump has repeatedly treated the stock market like a national scoreboard. When stocks rise, it proves confidence is back. When stocks fall, the market is supposedly misunderstanding the economy. His recent frustration that stocks “should go up, not down” after strong jobs data fits that pattern perfectly.

But markets are not obligated to follow political slogans. The U.S. economy added 172,000 jobs in May, more than double analyst expectations, while unemployment held at 4.3%. Normally, a strong jobs report sounds bullish. In this market, it was double-edged because it reduced the case for near-term rate cuts and even pushed rate-hike probabilities back into the conversation.

That is the contradiction Trump faces. He wants lower rates, higher stocks, strong jobs, lower inflation, and geopolitical toughness at the same time. Markets want that same fantasy. But CPI, oil, and the Fed may not allow it.

If growth is too strong, the Fed has less reason to cut. If inflation is too high, the Fed has less room to cut. If oil keeps rising, consumers get squeezed. If consumers get squeezed, earnings estimates become harder to defend. That is the chain reaction investors should be watching.

The Fed Is Trapped — And the Market Knows It

The Fed is now stuck in one of the worst possible setups. Cutting too early risks looking political and losing credibility while CPI is still above 4%. Holding rates too long risks crushing housing, small businesses, consumers, and rate-sensitive sectors. Hiking again would be explosive for stocks, especially after a market built around AI multiples and easy-money expectations.

Reuters reported that some analysts now expect the Fed to keep rates on hold into 2027, while strong jobs data recently pushed market pricing to show a 42.7% probability of a December rate hike. Whether that probability holds or not, the message is clear: the rate-cut narrative is not as safe as bulls want it to be.

The Fed is no longer just fighting inflation. It is fighting oil prices, Iran risk, Trump pressure, bond-market expectations, tariff uncertainty, and an equity market that has become addicted to the idea that every dip will eventually be rescued.

AI Stocks Are Powerful — But Not Untouchable

The bull case for AI is still real. Nvidia, Microsoft, Alphabet, Amazon, Meta, AMD, Broadcom, and Intel are sitting at the center of one of the largest capital-expenditure cycles in modern market history. Data centers, GPUs, cloud infrastructure, sovereign AI, enterprise automation, cybersecurity, and power demand are all long-term themes.

But inflation changes the valuation conversation.

Nvidia at nearly $5 trillion is not priced like a normal chip company. Alphabet near $4.34 trillion, Microsoft near $2.99 trillion, Amazon around $2.61 trillion, Meta around $1.48 trillion, and AMD around $759 billion are not tiny cyclical names that can ignore macro pressure. These companies now represent the center of the market.

That is the risk. If AI leaders wobble, the broader indices wobble. If semis sell off, the Nasdaq feels it. If higher oil keeps CPI hot, the Fed stays cautious. If the Fed stays cautious, the discount rate stays high. And if the discount rate stays high, investors may stop paying unlimited multiples for future AI growth.

The Consumer Is Still the Weak Link

Markets love to debate “headline versus core” inflation, but households do not live in core CPI. They live in rent, gasoline, groceries, insurance, credit-card rates, auto loans, electricity bills, and mortgage payments.

That is why the CPI report is politically dangerous. Even if economists say the data was “in line,” consumers hear something different: prices are still too high, relief is not here, and the Fed may not cut fast enough to make borrowing cheaper.

If inflation stays sticky because of energy, war, and policy uncertainty, the consumer could become the weak link in the market’s AI optimism. Companies can keep building data centers, but if households pull back, the earnings story becomes harder outside the AI winners.

The Debate Investors Should Be Having

The bullish view is that CPI met expectations, core inflation remains contained, semis can recover, and AI spending is strong enough to overpower macro noise. Under that scenario, oil stabilizes, the Fed stays patient, and the market eventually climbs the wall of worry.

The bearish view is that investors are being too complacent. Headline inflation is back at 4.2%, energy commodities are up 40.6%, oil is near $90, semis just lost over $1 trillion in market value during one selloff, and the Fed has no clean path to rate cuts. Under that view, the AI trade is still powerful but increasingly fragile.

The political view may be the most controversial. Trump wants stocks higher and rates lower, but Iran tensions are pushing oil higher, CPI gives the Fed cover to stay cautious, and the market is now trading a messy mix of inflation, war, AI, oil, and election-style political pressure.

What Investors Should Watch Next

Investors should watch oil first. If Brent stays above $90 or pushes back toward the levels seen during the worst Iran-war headlines, CPI pressure may remain sticky. Gasoline prices matter next because they feed directly into consumer sentiment and political pressure.

The second thing to watch is semiconductors. If NVDA, AMD, AVGO, INTC, and SMH continue weakening, the market may be signaling that AI leadership is no longer enough to ignore macro risk. If semis recover strongly, bulls will argue the CPI scare is another dip-buying opportunity.

The third thing to watch is the Fed. Any hint that officials are more worried about energy inflation than core disinflation could reset rate-cut expectations again. That is where the real market risk sits.

Bottom Line

The latest CPI report did not kill the bull market, but it made the “inflation is over” story much harder to defend.

With CPI at 4.2%, oil near $90, energy commodities up 40.6%, semiconductors under pressure, and Trump pushing for a stronger market while Iran risk keeps inflation alive, investors are facing a more explosive setup than the headline reaction suggests.

The market is betting that energy inflation fades, AI leadership holds, and the Fed eventually cuts. Maybe that works. But if oil stays elevated and semis keep wobbling, this CPI print may be remembered as the warning shot investors tried very hard to ignore.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}