- SK Hynix raised $26.5B and opened 14% above its $149 ADR price.

- The listing gives U.S. investors direct exposure to AI memory and HBM demand.

- It could reprice memory stocks like Micron and Samsung as AI infrastructure spending expands.

The Big Picture

The semiconductor IPO market just received one of its strongest signals of the AI cycle.

SK Hynix, the South Korean memory-chip giant, raised about $26.5 billion through its U.S. ADR offering, pricing 177.9 million American Depositary Receipts at $149 each. The stock opened at roughly $170, about 14% above the offer price, making it one of the biggest foreign-company market debuts in U.S. history.

This matters because SK Hynix is not a small AI startup.

It is one of the world’s most important memory suppliers, with deep exposure to high-bandwidth memory, or HBM — the advanced memory used alongside AI processors in data centers.

For investors, the debut sends a clear message:

The AI trade is no longer only about Nvidia-style GPUs.

It is also about the memory, packaging, testing, and capacity expansion needed to make AI infrastructure work.

What Happened

SK Hynix listed ADRs on Nasdaq, giving U.S. investors easier access to one of the most important companies in the AI memory supply chain.

The key numbers were strong:

- Offer size: about $26.5 billion

- ADR price: $149

- Opening price: about $170

- First move: roughly +14%

- ADRs sold: about 177.9 million

- Ticker: initially SKHYV, moving to SKHY

The scale of the offering is important. A $26.5 billion raise is larger than many full semiconductor companies’ market capitalizations and shows how much demand still exists for AI-linked chip exposure.

This was not just a listing.

It was a major liquidity event for the global semiconductor sector.

Why SK Hynix Matters

SK Hynix matters because AI needs memory.

Modern AI systems require enormous amounts of fast data movement. GPUs do the computing, but HBM helps feed data into those processors at high speed. Without enough advanced memory, AI accelerators cannot operate at full efficiency.

That is why SK Hynix has become central to the AI supply chain.

The company is one of the leading HBM suppliers globally and is closely tied to demand from AI data centers. Its memory products are used in systems powering large AI models, hyperscale workloads, and next-generation server infrastructure.

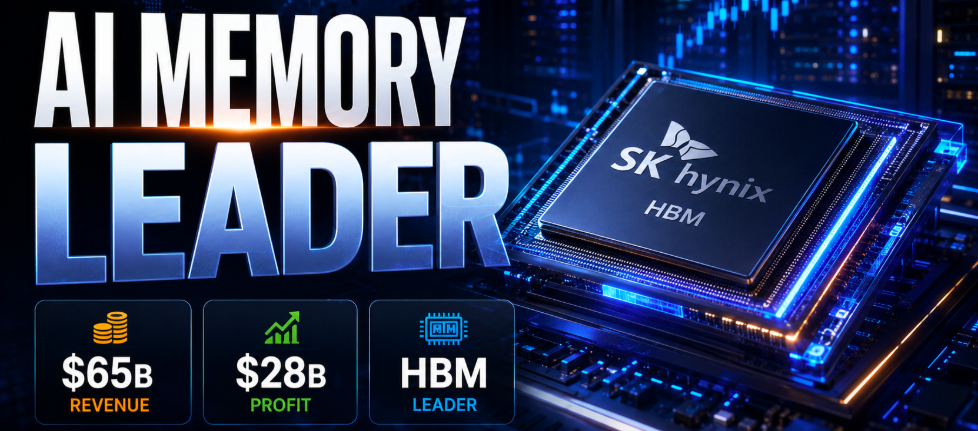

The company’s financial scale also shows why investors care. SK Hynix reportedly generated close to $65 billion in 2025 revenue and roughly $28 billion in profit, helped by the AI memory boom.

Those are not speculative numbers.

They show that AI memory has already become a major profit engine.

Why This IPO Is Bigger Than One Stock

The SK Hynix debut is important because it gives investors a new benchmark for the memory side of AI.

Over the past two years, the AI semiconductor trade has been dominated by:

- Nvidia

- Broadcom

- AMD

- TSMC

- ASML

- Micron

- semiconductor equipment stocks

But SK Hynix adds a different layer.

It brings direct public-market focus to the memory bottleneck.

That matters because AI infrastructure spending is not just about buying GPUs. It also requires:

- HBM supply

- advanced packaging

- DRAM capacity

- wafer testing

- power management

- data-center networking

- manufacturing equipment

A strong SK Hynix debut confirms that investors are willing to pay for the full AI supply chain, not just the most obvious winners.

What It Brings to the Semiconductor Sector

SK Hynix’s U.S. listing brings three important things to the sector.

First, it gives U.S. investors easier access to AI memory exposure.

Second, it increases the visibility of HBM as one of the most important growth markets in semiconductors.

Third, it creates a new valuation reference point for memory peers.

That could matter for Micron, Samsung Electronics, and semiconductor equipment companies. If SK Hynix trades at a premium because of HBM demand, investors may reassess whether other memory-linked stocks deserve higher multiples too.

A successful listing can also improve sentiment across the sector.

When a major chip company raises $26.5 billion and opens 14% higher, it tells the market that AI semiconductor demand remains strong.

Why This Matters for Micron

Micron is one of the most direct U.S.-listed comparisons.

Both Micron and SK Hynix are exposed to memory demand, DRAM cycles, HBM pricing, and AI server growth.

The key difference is perception.

SK Hynix is widely viewed as a leader in HBM, while Micron is still trying to prove that it can capture a larger share of the AI memory market. If SK Hynix trades strongly in the U.S., Micron could benefit from a sector rerating.

The logic is simple:

If investors are willing to pay a high multiple for AI memory exposure, they may also look again at Micron.

But the risk goes both ways.

If investors start worrying about HBM oversupply, weaker pricing, or slowing AI capex, both SK Hynix and Micron could fall together.

Why This Matters for Samsung

Samsung is another key player.

Samsung remains one of the largest semiconductor companies in the world, but SK Hynix has taken a stronger investor narrative around HBM. The Nasdaq debut increases that pressure.

If SK Hynix becomes the global public-market benchmark for AI memory, Samsung may need to prove that it can close the HBM perception gap.

That creates a competitive dynamic across the sector:

- SK Hynix leads the AI memory narrative

- Samsung needs to regain momentum

- Micron tries to capture more U.S. investor interest

- equipment suppliers benefit if capacity expands

This is why the IPO is not just about one company.

It could shape how investors rank the memory leaders.

Why Equipment Stocks Could Benefit

A major AI memory cycle does not only help memory producers.

It can also benefit the companies that enable production.

If SK Hynix and its competitors expand HBM and DRAM capacity, that supports demand for:

- lithography tools

- etching systems

- deposition equipment

- metrology and inspection

- wafer testing

- advanced packaging

- burn-in and reliability testing

That is important because AI chips are becoming harder and more expensive to manufacture.

The more complex the chip stack becomes, the more valuable the equipment ecosystem becomes.

This is why investors may look beyond SK Hynix and into semiconductor equipment names after the IPO.

The AI Memory Supercycle

The bullish case is that AI memory is entering a supercycle.

AI servers require much more memory bandwidth than traditional servers. As hyperscalers build larger clusters, demand for HBM could remain structurally strong.

That could support:

- higher memory pricing

- stronger margins

- larger capex budgets

- tighter supply

- better earnings visibility

This is the core reason the SK Hynix debut was so strong.

Investors are betting that AI memory is not a one-year spike, but a multi-year infrastructure cycle.

The Risk: Memory Is Still Cyclical

The main risk is that memory has always been cyclical.

When pricing is strong, companies invest heavily in new capacity. Over time, too much capacity can create oversupply. When that happens, prices fall, margins compress, and stocks sell off.

That is the classic memory cycle.

The question now is whether AI demand is strong enough to absorb new supply.

If it is, SK Hynix could keep benefiting.

If it is not, the stock could become vulnerable after a major debut and large pre-listing enthusiasm.

That is why investors should watch HBM pricing and capex closely.

Why This Could Reprice the Sector

A strong IPO can shift investor psychology.

SK Hynix raised $26.5 billion, opened 14% higher, and gave U.S. investors direct access to one of the most important AI memory suppliers.

That could push investors to reassess:

- Micron’s valuation

- Samsung’s HBM execution

- equipment-stock exposure

- AI infrastructure spending

- memory-cycle duration

It could also widen the gap between true AI infrastructure winners and weaker semiconductor names.

This is not likely to lift every chip stock equally.

The winners will probably be companies with real exposure to AI memory, packaging, testing, and data-center demand.

What Investors Should Watch Next

Investors should focus on six signals.

- First, whether SK Hynix holds above its $149 offer price and $170 opening level.

- Second, whether Micron and Samsung rerate alongside it.

- Third, whether HBM pricing stays strong through the next few quarters.

- Fourth, whether hyperscaler AI capex remains elevated.

- Fifth, whether SK Hynix increases capacity too aggressively.

- Sixth, whether semiconductor equipment orders rise in response to memory expansion.

These signals will show whether this IPO is just a strong debut or the start of a wider semiconductor revaluation.

The Bull Case

The bull case is that SK Hynix becomes the public-market benchmark for AI memory.

If AI data-center spending remains strong, HBM supply stays tight, and memory pricing holds up, SK Hynix could become one of the most important AI infrastructure stocks globally.

In that scenario, the IPO could support a broader rerating across:

- memory stocks

- advanced packaging

- semiconductor equipment

- AI infrastructure suppliers

- data-center hardware names

The Bear Case

The bear case is that expectations are already stretched.

SK Hynix opened 14% above its offer price after raising $26.5 billion, and investor enthusiasm around AI memory is intense. If the market starts to price in perfection, even small disappointments could matter.

The risk is not that AI disappears.

The risk is that investors pay too much, too early, for the memory cycle.

Semiconductors remain cyclical, even during powerful growth themes.

Bottom Line

SK Hynix’s Nasdaq debut is a major moment for the semiconductor sector.

The company raised about $26.5 billion, sold roughly 177.9 million ADRs at $149, opened around $170, and gave U.S. investors direct exposure to one of the most important AI hardware bottlenecks: high-bandwidth memory.

This is not just an IPO story.

It is a memory story.

It is an AI infrastructure story.

It is a semiconductor-capex story.

And it may become a new valuation benchmark for the next phase of the chip cycle.

The strongest takeaway is simple:

The AI trade is moving beyond GPUs. SK Hynix’s debut shows investors are now chasing the memory infrastructure behind them.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. Semiconductor stocks can be highly volatile and are affected by demand cycles, pricing, capital spending, geopolitical risk, customer concentration, and broader market conditions.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}