- Canadian junior mining stocks are gaining investor attention as gold prices, resource nationalism, and development-stage optionality move back into focus.

- This 10x Alerts screen focuses on Canadian-listed mining companies in the small-cap development and advanced-exploration range, roughly CAD $100M to CAD $250M.

- The broader opportunity is finding defined assets, credible jurisdictions, and visible catalysts before the market fully prices in the next re-rating phase.

Canadian mining stocks are becoming more interesting for investors who want exposure beyond the largest gold producers. Major producers are already widely followed, but the junior and small-cap development space is where valuation gaps can still appear.

That is especially true in the CAD $100M to CAD $250M market-cap range. Companies in this bracket are usually beyond the earliest exploration stage, but still small enough that a resource update, feasibility study, permitting milestone, financing package, strategic investment, or takeover speculation can materially change the market’s view.

- The sweet spot is not just “cheap mining stocks.”

- The better setup is a defined asset, a real jurisdiction, enough liquidity, and a clear next catalyst.

- The risk is that these companies are still pre-production or early-development names, which means funding, permitting, dilution, and execution risk remain high.

For this screen, Falco Resources is used as the reference point because it sits in the right valuation zone and owns a large, advanced project in Québec. The broader article compares Falco with other Canadian mining stocks trading in a similar size category.

Investor Snapshot

| Rank | Company | Ticker | Recent Price | Approx. Market Cap | Main Asset / Region | Investor Angle |

|---|---|---|---|---|---|---|

| 1 | Falco Resources | FPC.V | ~CAD $0.47-$0.48 | ~CAD $160M-$185M | Horne 5, Québec | Advanced polymetallic gold project in an established mining camp |

| 2 | Maple Gold Mines | MGM.V | ~CAD $2.70-$3.00 | ~CAD $190M-$210M | Douay-Joutel, Québec | Abitibi gold resource growth and district-scale optionality |

| 3 | Fury Gold Mines | FURY.TO | ~CAD $0.80-$0.83 | ~CAD $150M | Eau Claire, Québec | High-grade gold development and exploration upside |

| 4 | Wallbridge Mining | WM.TO | ~CAD $0.10-$0.11 | ~CAD $120M-$155M | Fenelon / Martiniere, Québec | Large land package in the Detour-Fenelon trend |

| 5 | Big Ridge Gold | BRAU.V | ~CAD $0.44-$0.49 | ~CAD $125M-$140M | Hope Brook, Newfoundland | Advanced-stage gold project with technical de-risking path |

Why This Market-Cap Range Matters

The CAD $100M to CAD $250M range is one of the more interesting places to look in Canadian mining.

Below that range, many companies are too early, too illiquid, or too dependent on constant equity financing. Above that range, a larger portion of the project value may already be priced in, especially if the company has a more advanced study or stronger institutional following.

- In this range, companies often have enough project definition to analyze.

- They may still trade at a discount to project value or resource potential.

- A single catalyst can still move the stock materially.

This is why the group matters. These are not producers, and they should not be treated like producers. They are development and exploration-stage mining equities. The investment case depends on whether the market starts assigning more value to the asset base, jurisdiction, technical work, and next financing path.

1. Falco Resources: Advanced Québec Development Exposure

Falco Resources is the most advanced project-driven name in this screen. The company is advancing the Horne 5 Project in Rouyn-Noranda, Québec, one of Canada’s most established mining districts.

The project gives Falco a different profile from a pure exploration company. Horne 5 has a feasibility-stage framework, meaningful scale, and exposure to gold plus copper, zinc, and silver by-products.

- Recent price: around CAD $0.47 to CAD $0.48.

- Approximate market cap: around CAD $160M to CAD $185M.

- Main project: Horne 5, Québec.

- Key investor catalyst: feasibility update, permitting, government decree, financing structure, and project advancement.

The main attraction is the gap between Falco’s market cap and the economic value outlined in the project’s feasibility work. In a stronger metals-price environment, that gap can become more visible.

The risk is that large development projects are capital-intensive. Even strong projects can trade at large discounts until investors see a clear permitting and financing path.

For investors, Falco is the advanced developer in the group: higher project definition, but also higher financing and permitting complexity.

2. Maple Gold Mines: Abitibi Resource Growth

Maple Gold Mines gives investors exposure to the Douay-Joutel Gold Project in Québec’s Abitibi Greenstone Belt. The Abitibi is one of Canada’s most important gold regions, which gives Maple Gold a strong jurisdictional angle.

Maple Gold is not the same kind of story as Falco. It is more of a resource-growth and district-scale exploration thesis.

- Recent price: around CAD $2.70 to CAD $3.00.

- Approximate market cap: around CAD $190M to CAD $210M.

- Main project: Douay-Joutel, Québec.

- Key investor catalyst: resource growth, drilling, high-grade underground potential, and future economic studies.

The appeal is that Maple Gold has a large land package and a resource base in a premium gold belt. If the company can improve grade, expand resources, and create a clearer development path, the market could begin to value the asset more aggressively.

The risk is that resource growth alone is not enough. Investors will eventually need to see economics, mineability, metallurgy, and a credible route toward development.

For this watchlist, Maple Gold is the Abitibi resource-growth pick.

3. Fury Gold Mines: High-Grade Québec Optionality

Fury Gold Mines is another Québec-focused gold company, with its flagship Eau Claire Project in the Eeyou Istchee James Bay region.

Fury’s appeal is high-grade gold exposure. In junior mining, grade matters because higher-grade projects can often support better margins, stronger economics, and more strategic interest if scale continues to improve.

- Recent price: around CAD $0.80 to CAD $0.83.

- Approximate market cap: around CAD $150M.

- Main project: Eau Claire, Québec.

- Key investor catalyst: drilling, resource conversion, economic updates, and project de-risking.

Fury is interesting because it gives investors a blend of exploration upside and development potential. It is not just a grassroots target, but it still has room to grow through drilling and technical work.

The risk is that high-grade projects still require scale, infrastructure planning, permitting, and funding. A strong deposit does not automatically become a mine.

For this watchlist, Fury is the high-grade Québec option.

4. Wallbridge Mining: Scale and Turnaround Potential

Wallbridge Mining gives investors exposure to the Detour-Fenelon gold trend in Québec. Its key assets include Fenelon and Martiniere, along with a broader district-scale land position.

Wallbridge has been on investor screens for years, which is both a strength and a weakness. The company has a known asset base and meaningful historical drilling, but the stock also needs a clearer catalyst to rebuild momentum.

- Recent price: around CAD $0.10 to CAD $0.11.

- Approximate market cap: around CAD $120M to CAD $155M.

- Main projects: Fenelon and Martiniere, Québec.

- Key investor catalyst: drilling, metallurgical work, updated technical studies, and a clearer development path.

The upside case is that the land package and resource base are still meaningful relative to the current valuation. If Wallbridge can simplify the story and show a more financeable path, the market may begin to re-rate it.

The risk is investor fatigue. The company needs to prove that the next technical steps can create fresh value.

For this watchlist, Wallbridge is the scale-and-turnaround pick.

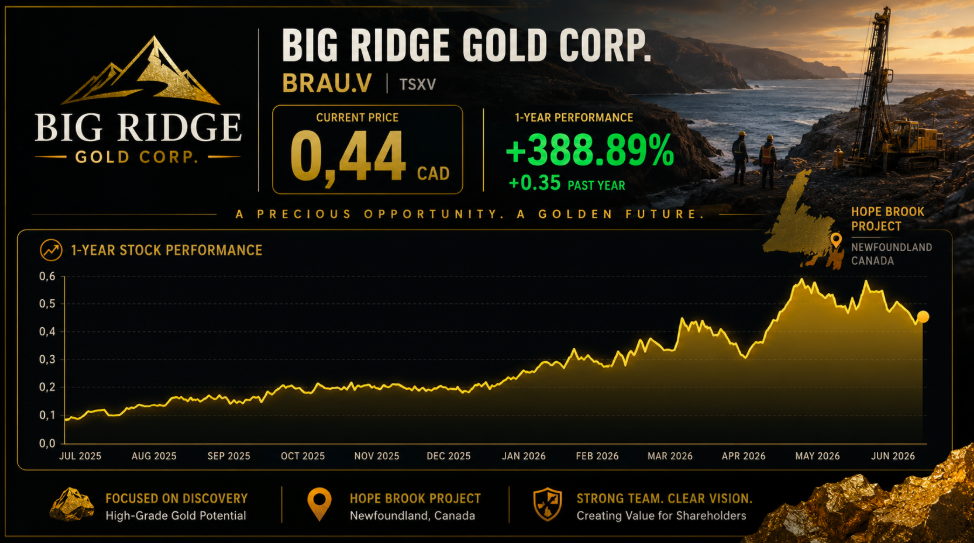

5. Big Ridge Gold: Newfoundland Advanced-Project Angle

Big Ridge Gold is focused on the Hope Brook Gold Project in Newfoundland and Labrador. Unlike the Québec-heavy names in this screen, Big Ridge offers a different Canadian jurisdiction and a different project angle.

Hope Brook is an advanced-stage gold project with historical mining context and ongoing technical work. That gives Big Ridge a more defined asset base than a pure early-stage explorer.

- Recent price: around CAD $0.44 to CAD $0.49.

- Approximate market cap: around CAD $125M to CAD $140M.

- Main project: Hope Brook, Newfoundland and Labrador.

- Key investor catalyst: technical work, geotechnical drilling, hydrogeological studies, PEA progress, and project de-risking.

Big Ridge’s setup is about moving Hope Brook toward a more complete development framework. Investors will likely watch for technical work that can support future economics and permitting.

The risk is that the project still needs more de-risking before the market values it like a more mature development asset.

For this watchlist, Big Ridge is the Newfoundland advanced-project pick.

Key Comparison Table

| Company | Ticker | Main Metal Exposure | Project Stage | Jurisdiction | Why It Fits the Screen | Risk Level |

| Falco Resources | FPC.V | Gold, copper, zinc, silver | Feasibility-stage development | Québec | Large advanced project, clear valuation gap | High |

| Maple Gold Mines | MGM.V | Gold | Resource growth / exploration | Québec | Abitibi district-scale resource story | High |

| Fury Gold Mines | FURY.TO | Gold | PEA / exploration-development | Québec | High-grade Québec optionality | High |

| Wallbridge Mining | WM.TO | Gold | Resource / technical studies | Québec | Large Detour-Fenelon land package | High |

| Big Ridge Gold | BRAU.V | Gold | Advanced exploration / development | Newfoundland | Hope Brook technical de-risking path | High |

What Could Re-Rate These Stocks

The common thread across the group is not current production. It is project advancement.

These companies are still valued like junior developers and advanced explorers. That means the market is waiting for evidence that their projects can become more valuable, more financeable, or more strategic.

- Resource growth: more ounces, better grade, or higher-confidence categories.

- Economic studies: updated PEA, PFS, feasibility study, or sensitivity to stronger gold prices.

- Permitting: movement toward government approvals and lower regulatory uncertainty.

- Financing: strategic partners, royalty deals, debt packages, or non-dilutive funding options.

- M&A potential: larger miners looking for Canadian gold development pipelines.

The best junior mining setups usually combine three things: a real asset, a credible jurisdiction, and a catalyst that can force the market to re-price the stock.

10x Alerts Takeaway

This is not a list of low-risk mining stocks. It is a watchlist of Canadian junior and small-cap mining names that trade in a similar valuation zone and could benefit if investors continue rotating into gold developers and advanced explorers.

- Falco Resources is the advanced feasibility-stage Québec developer.

- Maple Gold Mines is the Abitibi resource-growth story.

- Fury Gold Mines is the high-grade Québec optionality play.

- Wallbridge Mining is the scale-and-turnaround candidate.

- Big Ridge Gold is the Newfoundland advanced-project angle.

The common thread is market-cap asymmetry. Each company is still small enough that a major technical, permitting, financing, or strategic milestone could move the stock. But each also carries real junior-mining risk.

Bottom Line

Canadian small-cap mining investors do not need to focus on one name alone. A stronger approach is to compare a basket of developers and advanced explorers with defined assets, credible jurisdictions, and visible catalysts.

Falco Resources, Maple Gold Mines, Fury Gold Mines, Wallbridge Mining, and Big Ridge Gold each offer a different angle on the Canadian gold-development trade. For 10x Alerts investors, the opportunity is selective asymmetry: the next winners will likely be the companies that turn project potential into clearer economics, lower permitting risk, better financing visibility, or strategic interest from larger mining groups.

Disclaimer: This article is for informational purposes only and is not financial advice. Junior mining stocks can be volatile, illiquid, speculative, and highly sensitive to commodity prices, financing conditions, permitting outcomes, and project execution.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}