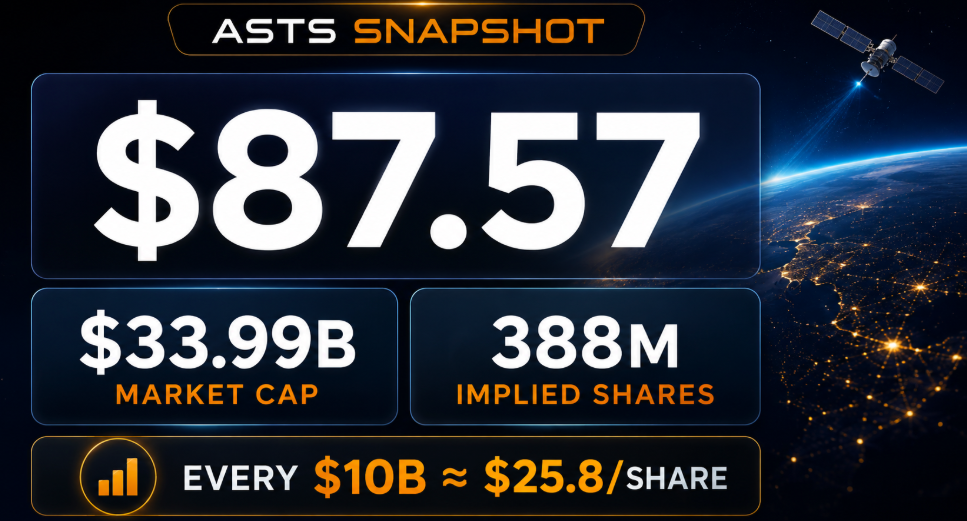

- ASTS is trading around $87.57, with a market cap near $34B.

- Tomorrow’s BlueBird 8-10 launch is the key near-term catalyst.

- Japan/Rakuten remains a major upside watch item for Q4 2026.

Why Tomorrow Matters

AST SpaceMobile is heading into a major catalyst window.

The company is expected to launch BlueBird satellites 8, 9, and 10 aboard a SpaceX Falcon 9 from Cape Canaveral. For investors, this launch is not just about adding three satellites. It is about proving that ASTS can keep deploying its constellation after recent launch-related concerns and delays.

ASTS is now a launch-cadence stock.

Every successful launch reduces execution risk, improves confidence in the satellite rollout, and brings the company closer to commercial direct-to-device service.

• The market wants proof that ASTS can turn satellite manufacturing into repeated launches, repeated deployments, and eventually repeated revenue.

Current Stock Snapshot

ASTS is trading around $87.57.

The most useful headline market-cap figure is around $33.99B, based on Google Finance’s latest visible market cap. Some data providers show a lower market cap near $25B–$26B, likely because of differences in share-count methodology. For investor-facing content, the cleaner approach is to use ~$34B as the headline valuation and note that reported market cap varies by data source.

At $87.57 and ~$33.99B, ASTS implies roughly 388M shares on an implied-market-cap basis.

That matters because every $10B of market value equals roughly $25.8 per share using this broader implied share count.

• ASTS is no longer a small speculative space stock. It is already valued like a serious future telecom-infrastructure platform.

What To Expect From The BlueBird 8-10 Launch

The first market reaction will likely depend on whether the launch is clean.

Investors will be watching for:

- successful Falcon 9 liftoff

- clean satellite separation

- early satellite health confirmation

- deployment commentary

- initial communication / testing timeline

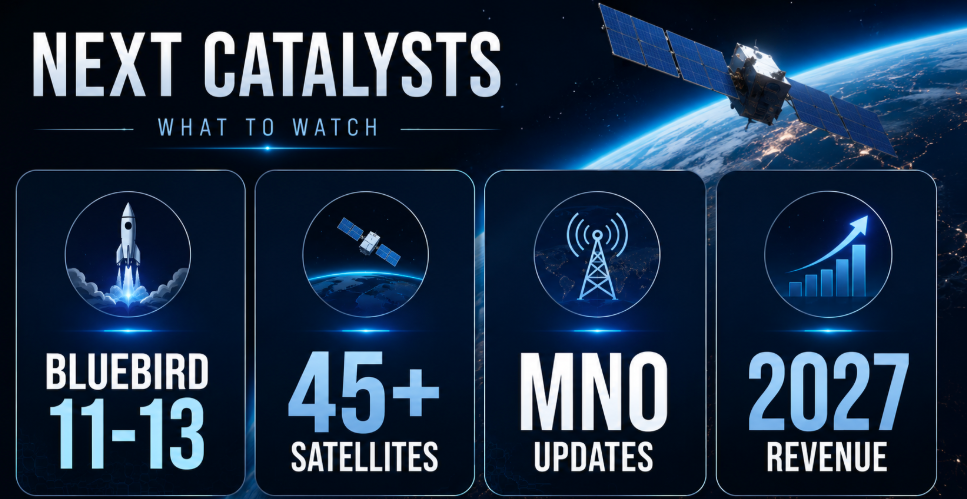

- update on BlueBird 11-13

- updated launch cadence

- management confidence around 2026 revenue guidance

A successful launch does not instantly unlock full commercial revenue.

But it does strengthen the bridge to commercialization.

The stock may react positively if investors see this launch as proof that ASTS can keep its constellation plan moving forward.

• The launch is a credibility catalyst. The real upside comes if it supports the revenue ramp.

Why BlueBird 8-10 Matters For Revenue

ASTS reported $14.7M of Q1 2026 revenue and has maintained full-year 2026 revenue guidance of $150M–$200M.

That means revenue needs to accelerate materially through the rest of the year.

The company’s near-term revenue sources are expected to come from:

- mobile network operator partners

- U.S. government work

- gateways and partner infrastructure

- engineering services

- early commercial-service activity

- future recurring direct-to-device service revenue

The current quarter alone does not justify the valuation.

The revenue ramp does.

If ASTS moves from $14.7M in Q1 toward $150M–$200M in 2026 revenue, the market can keep valuing the company as an emerging commercial network rather than a pure development-stage satellite company.

• The launch matters because satellites are the infrastructure behind the revenue model. No constellation, no commercial ramp.

The Japan Catalyst

Japan may become one of ASTS’s most important international markets.

Rakuten Mobile and AST SpaceMobile have already demonstrated a major technical milestone in Japan: a broadband video call between unmodified smartphones using a low Earth orbit satellite.

Rakuten and ASTS are targeting Q4 2026 for Rakuten Saikyo Satellite Service Powered by AST SpaceMobile, which is expected to support satellite-to-mobile broadband services across Japan.

This matters because Japan has several characteristics that make satellite-to-mobile service highly valuable:

- mountainous regions

- remote islands

- disaster-response needs

- earthquake and typhoon risk

- rural coverage gaps

- national resilience priorities

- strong mobile-operator distribution

The Japan angle is not only about consumer connectivity.

It is about emergency communication, resilient infrastructure, remote coverage, and national redundancy.

• If ASTS and Rakuten can turn Japan into a commercial rollout market, it could become one of the clearest international validations of the ASTS model.

The Potential Japan Contract Angle

There has been investor discussion around a potential high-value Japan opportunity, including speculation around a large satellite-connectivity contract or support program.

This should be handled carefully.

The official public information confirms that Rakuten and ASTS are working together, have completed a Japan video-call milestone, and are targeting Q4 2026 service launch. However, a specific $1B Japan contract award to ASTS has not been officially confirmed in the public sources I checked.

That does not make the Japan opportunity irrelevant.

It means investors should treat it as upside optionality, not as already-booked revenue.

A Japan win could matter in three ways:

- Commercial validation: proving ASTS can support a national mobile-network partner outside the U.S.

- Revenue visibility: adding partner-driven revenue or milestone payments.

- Strategic value: showing governments and operators that ASTS can support disaster-resilient mobile coverage.

• A confirmed Japan award would be a major catalyst. Until then, Japan should be treated as one of the biggest upside watch items, not a guaranteed contract.

Next Catalysts After The Launch

The market will quickly move from “Did BlueBird 8-10 launch?” to “What comes next?”

The next major catalysts are:

- satellite health and deployment updates

- BlueBird 11-13 launch timing

- further launch-provider announcements

- progress toward 45+ satellites

- commercial-service activation timeline

- U.S. mobile-network partner updates

- Verizon / AT&T / other MNO rollout commentary

- Rakuten Japan updates

- U.S. government contract expansion

- Q2 and Q3 revenue acceleration

- reaffirmation of 2026 guidance

- visibility toward 2027 revenue

The most powerful catalyst stack would be:

successful launch + next launch date + Japan progress + revenue acceleration.

• ASTS needs launch cadence and revenue conversion to move together.

Revenue Path: Why The Stock Still Has Upside

ASTS is expensive on current revenue.

But the market is not buying ASTS for current revenue. It is buying the possibility that ASTS becomes a global direct-to-device satellite broadband infrastructure layer.

The company’s revenue bridge looks like this:

- Q1 2026 revenue: $14.7M

- 2026 guidance: $150M–$200M

- 2026 midpoint: ~$175M

- 2027 upside case: approaching $1B if commercial service activates

- longer-term case: recurring revenue from MNOs, governments, enterprise, public safety, and international rollouts

This is why the stock can still move higher.

If the market becomes more confident in 2027 revenue, the valuation may shift from “too expensive on 2026 numbers” to “early premium for a scarce direct-to-device leader.”

• The stock is trading on whether ASTS can move from launch story to revenue platform.

Valuation Framework

Using ~$33.99B market cap and $87.57 share price, ASTS has an implied share count of roughly 388M shares.

Illustrative valuation scenarios:

| Scenario | Implied Market Value | Approx. Share Price |

|---|---|---|

| Execution risk remains high | $25B | ~$64 |

| Current valuation zone | $34B | ~$88 |

| Clean launch + better revenue confidence | $40B | ~$103 |

| Strong 2027 revenue visibility | $50B | ~$129 |

| Japan + U.S. partner momentum | $60B | ~$155 |

| Global D2D leader premium | $75B | ~$193 |

| Large-scale telecom-infrastructure case | $100B | ~$258 |

These are not price targets.

They are scenario math.

The important point is that ASTS can still show meaningful upside if the market starts believing in a larger 2027–2028 revenue ramp.

• The stock is already priced for success, but not necessarily for global direct-to-device leadership.

Revenue Multiple Framework

At a ~$34B market cap, ASTS looks very expensive against 2026 revenue guidance.

But the multiple compresses quickly if revenue scales.

| Revenue Base | Market Cap | Implied Revenue Multiple |

| 2026 midpoint: ~$175M | ~$34B | ~194x |

| 2027 potential: ~$1.0B | ~$34B | ~34x |

| Larger-scale case: ~$1.6B | ~$34B | ~21x |

| $2.0B network case | ~$34B | ~17x |

| $3.0B network case | ~$34B | ~11x |

This explains the stock.

If revenue stays near 2026 levels, the valuation looks stretched.

If ASTS moves toward $1B+ revenue, the valuation becomes easier to defend.

If the company becomes a recurring global telecom-infrastructure platform, investors may continue assigning it a premium.

• ASTS is not cheap. The bull case is that it can grow into the valuation faster than skeptics expect.

What Could Push The Stock Higher

The strongest upside catalysts are:

- BlueBird 8-10 successful launch

- clean satellite health confirmation

- BlueBird 11-13 launch date

- progress toward 45+ satellites

- commercial-service timeline confirmation

- stronger-than-expected Q2 or Q3 revenue

- 2026 guidance reaffirmation or raise

- more government contract wins

- Japan / Rakuten commercial launch progress

- confirmed Japan contract or support program

- more MNO rollout details

- proof of recurring service revenue

The Japan piece is especially important because it could show that ASTS is not only a U.S. telecom story.

It could become a global infrastructure story.

• A real Japan contract win would likely be one of the most important non-U.S. validation catalysts for ASTS.

Bottom Line

ASTS is heading into a critical catalyst window.

The BlueBird 8-10 launch is important because it can restore confidence in deployment cadence and bring the company closer to commercial service. But the bigger story is what comes after: revenue acceleration, partner rollouts, government work, and international expansion.

The current stock price around $87.57 and market cap around $34B already reflect major expectations.

But ASTS can still have upside if the company proves that its satellite network can generate real revenue at scale.

The Japan opportunity adds another layer.

Rakuten and ASTS are targeting satellite-to-mobile broadband service in Japan in Q4 2026, and a confirmed major Japan contract or national connectivity win would be a serious re-rating catalyst.

The key takeaway: ASTS is expensive on today’s revenue, but tomorrow’s launch, Japan optionality, and 2027 revenue visibility could determine whether the market keeps treating it as a future global direct-to-device infrastructure leader.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}