- Markets sold off after President Trump said the interim Iran agreement was “over,” with the S&P 500 falling roughly 0.8% intraday and Nasdaq futures dropping about 1.1%.

- Oil prices jumped more than 5% to around $78 per barrel, while Treasury yields rose toward 4.35% on the 10-year, signaling renewed inflation concerns.

- Energy stocks gained between 2% and 4%, while airlines, tech, and consumer stocks declined, highlighting a clear sector rotation tied to oil and rates.

What Happened

President Trump said the memorandum of understanding with Iran was “over,” triggering a sharp shift in global markets.

The move came only weeks after markets had rallied on optimism that a preliminary U.S.-Iran agreement could reduce geopolitical risk and help stabilize energy markets. In mid-June, Brent crude had fallen to roughly $72 per barrel, its lowest level in three months, while the S&P 500 gained about 1.2% over two sessions following the deal announcement.

That relief trade has now reversed.

Following Trump’s latest comments, Brent crude rose more than 5% to approximately $78, while WTI crude climbed to around $74–$75 per barrel. U.S. stock futures weakened, with Nasdaq futures down about 1.1%, S&P 500 futures down roughly 0.7%, and Dow futures off about 0.5%.

At the same time:

- The 10-year Treasury yield rose to ~4.30%–4.35%

- The U.S. Dollar Index (DXY) gained about 0.4%

- European stocks (Stoxx 600) fell roughly 0.6%

The immediate market message was clear: investors are once again pricing in geopolitical risk and higher inflation expectations.

Why the Iran Deal Matters to Markets

Iran matters to markets primarily because of oil supply.

The country produces roughly 3.2 million barrels per day (bpd) and exports around 1.5 million bpd, making it a meaningful contributor to global supply. More importantly, Iran sits near the Strait of Hormuz, through which about 20% of global oil supply (roughly 20 million bpd) passes.

Any disruption—even perceived—can quickly move prices.

That is why the Iran deal mattered in the first place. It reduced the probability of supply disruption and lowered the geopolitical risk premium embedded in oil prices.

Now that risk premium is returning.

The Market Reaction

The reaction followed a classic inflation-driven risk-off pattern.

Oil surged. Stocks declined. Bond yields rose. The dollar strengthened.

But the details matter.

This combination suggests markets are reacting more to inflation risk than pure geopolitical fear.

Why Oil Is the First Asset to Move

Oil is the most direct transmission channel for Middle East risk.

Even a small perceived disruption can move prices because global spare capacity is limited—estimated at roughly 3–4 million bpd, mostly held by OPEC+.

When traders see rising tension, they immediately price in:

- potential supply loss (1–2 million bpd scenarios)

- higher shipping insurance costs (which can rise 20%–50% in conflict zones)

- tanker rerouting delays

- sanctions tightening

That is why oil can jump 5%–10% in a single session without any actual supply loss.

Why Stocks Sold Off

Stocks sold off primarily due to rising yields and inflation fears.

Higher oil prices feed directly into inflation. Gasoline prices in the U.S. typically rise about 2–3 cents per gallon for every $1 increase in crude oil. A $5 move in oil can therefore translate into a 10–15 cent increase at the pump, which affects consumer spending.

The impact on equities is uneven.

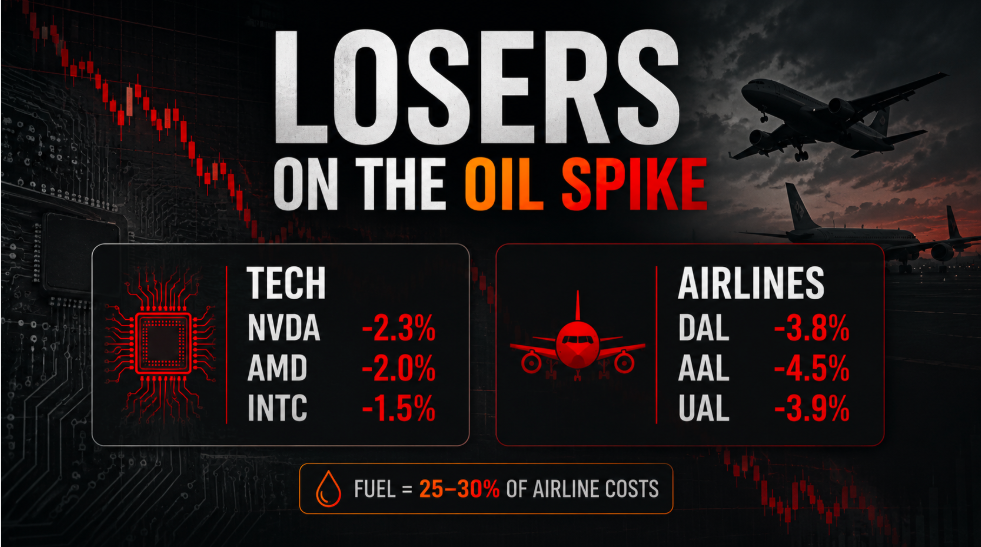

Tech and Growth Stocks (Losers)

- Nvidia (NVDA): -2.3%

- AMD (AMD): -2.0%

- Intel (INTC): -1.5%

These stocks are sensitive to interest rates. Higher yields reduce the present value of future earnings.

Airlines (Major Losers)

- Delta Air Lines (DAL): -3.8%

- American Airlines (AAL): -4.5%

- United Airlines (UAL): -3.9%

Fuel accounts for roughly 25%–30% of airline operating costs, making them highly sensitive to oil spikes.

Consumer Stocks (Moderate Losers)

- Amazon (AMZN): -1.2%

- Tesla (TSLA): -2.5%

Higher fuel costs reduce discretionary spending and increase logistics expenses.

Why Gold Did Not Rally

Gold fell despite geopolitical tension, declining about 0.6% to ~$2,320 per ounce.

The reason is interest rates.

Gold competes with yield-bearing assets. When the 10-year Treasury yield rises above 4.3%, holding gold becomes less attractive.

Additionally:

- A stronger dollar makes gold more expensive globally

- Rising real yields (inflation-adjusted) pressure gold prices

So instead of acting as a safe haven, gold reacted to macro conditions.

The Fed Problem

The Federal Reserve is central to this story.

Markets had been pricing in potential rate cuts later in the year. However, rising oil prices complicate that outlook.

Energy contributes roughly 7%–8% of CPI directly, but indirectly affects transportation, food, and services.

If oil stays above $80–$85, it could:

- push headline inflation higher by 0.3%–0.5%

- delay rate cuts

- keep real yields elevated

That is why bond yields rose instead of falling.

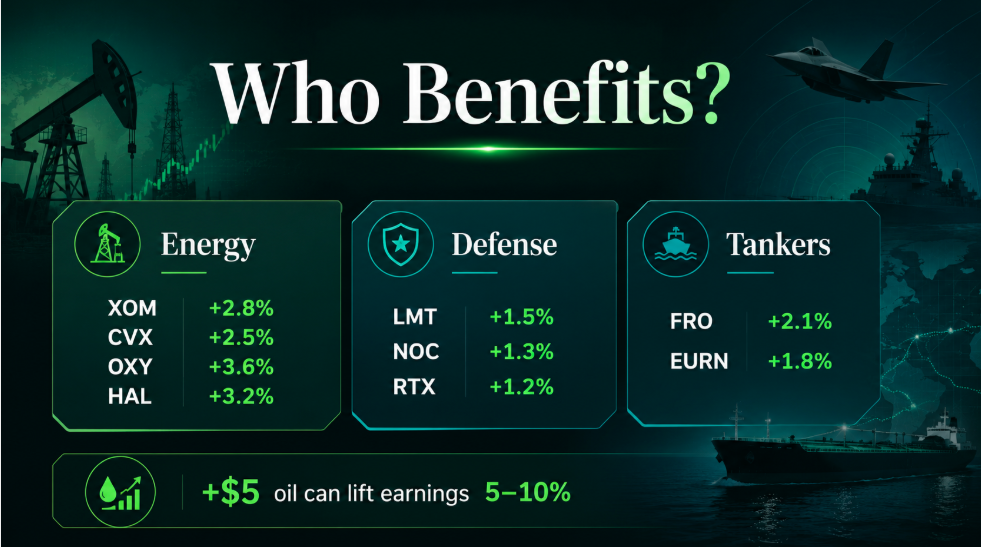

Sector Winners

Some sectors benefited immediately.

Energy Stocks (Clear Winners)

- ExxonMobil (XOM): +2.8%

- Chevron (CVX): +2.5%

- Occidental Petroleum (OXY): +3.6%

- Halliburton (HAL): +3.2%

Energy stocks typically gain leverage to oil prices. A $5 increase in crude can boost earnings expectations by 5%–10% for some producers.

Defense Stocks (Moderate Winners)

- Lockheed Martin (LMT): +1.5%

- Northrop Grumman (NOC): +1.3%

- Raytheon (RTX): +1.2%

Geopolitical tension often leads to increased defense spending expectations.

Shipping and Tankers

- Frontline (FRO): +2.1%

- Euronav (EURN): +1.8%

Higher risk can increase freight rates, though volatility remains high.

Why This Could Be Temporary

Markets often overreact to geopolitical headlines.

Historically, oil spikes tied to geopolitical events fade within 5–10 trading days if no actual supply disruption occurs.

For example:

- After prior Middle East tensions, oil spikes of 5%–8% often retraced 50%–70% within two weeks

- The S&P 500 typically recovers within 10–15 trading days if escalation does not occur

If negotiations resume or tensions cool, oil could fall back toward $72–$74, and equities could rebound.

Why This Could Get Worse

The downside scenario is more serious.

If oil rises toward $90–$100, the impact becomes systemic:

- Inflation could rise by 0.5%–1.0%

- Gasoline could exceed $4 per gallon nationally

- Consumer spending could slow by 0.5%–1% GDP impact

Markets would likely reprice:

- Fed policy (fewer or no rate cuts)

- earnings expectations

- equity valuations

What Investors Should Watch Next

Key indicators include:

- Brent crude: $80 is the first major threshold; $90 is critical

- 10-year Treasury yield: above 4.4% signals tightening financial conditions

- Gasoline prices: currently ~$3.50/gallon; rising toward $4 would pressure consumers

- Energy stocks vs. tech performance

- Strait of Hormuz developments

- Fed commentary and inflation data

Bottom Line

- Trump saying the Iran deal is “over” matters because it shifts the market’s inflation and risk outlook.

- Oil jumped more than 5%, stocks fell, and yields rose as investors priced in a renewed geopolitical risk premium.

- The key issue is whether oil stabilizes or continues rising.

- If crude remains below $80, markets may absorb the shock.

- If it moves toward $90–$100, the impact could extend to inflation, Fed policy, and equity valuations.

- That makes this more than a geopolitical headline—it is a macroeconomic event with direct implications for stocks, bonds, and commodities.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. Markets, commodities, geopolitical events, and policy decisions can change rapidly. Always conduct your own research and consult a licensed financial advisor before making investment decisions.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}