- SoFi is no longer just a story stock — it is now a scaling, profitable digital financial platform.

- Q1 2026 showed another step up, with record revenue, record members, and record product growth.

- The debate now is whether SOFI deserves to be valued like a lender — or like a higher-growth financial platform.

Why SOFI Still Feels Like an “Unloved” Stock

SoFi is one of those stocks that gets plenty of attention but still does not get universal respect.

Part of that is history. For years, many investors looked at SoFi as a flashy fintech story with strong branding but inconsistent profitability, heavy exposure to lending, and sensitivity to rates, credit, and the consumer cycle. Even now, despite clear growth and improving profitability, SOFI still tends to split opinion: bulls see a digital financial super-app with multiple growth engines, while skeptics still see a lender wrapped in a tech narrative.

That is why SoFi remains such a talked-about stock. It has already improved dramatically as a business, but the market still debates what it really is.

The Core Bull Case

The bull case on SOFI is pretty simple: this is a company still growing fast, still adding members and products at scale, and now doing it with real profitability.

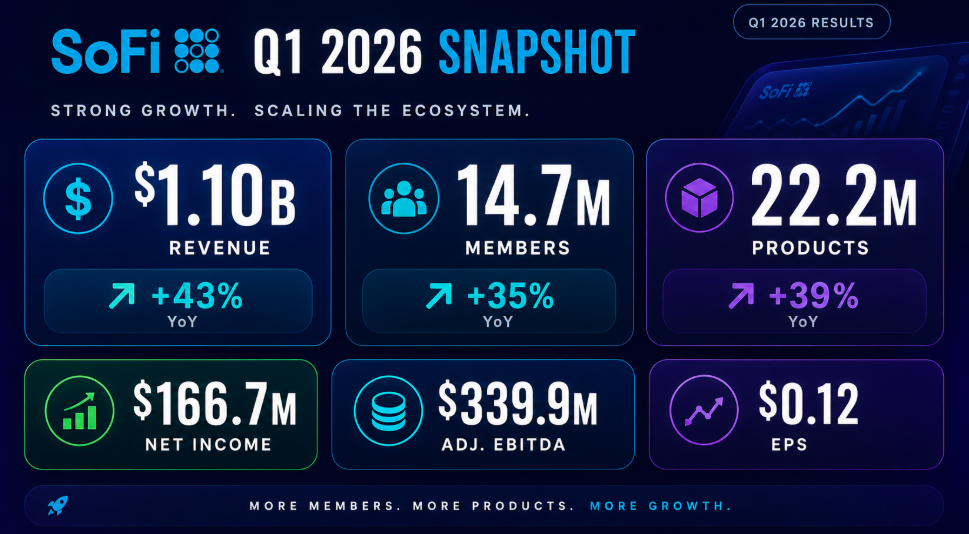

In Q1 2026, SoFi reported $1.10 billion in total net revenue, up 43% year over year, and $1.09 billion in adjusted net revenue, up 41%. Net income was $166.7 million, adjusted EBITDA was $339.9 million, and diluted EPS was $0.12. That is not the profile of a company just trying to survive — it is the profile of a company scaling into its model.

The other part of the bull case is the platform effect. In Q1, SoFi reached 14.7 million members, up 35%, and 22.2 million products, up 39%. It also said 43% of new products came from existing members, which supports the idea that SoFi is becoming more of a multi-product financial ecosystem, not just a one-product lender.

Recent Numbers That Matter

The recent numbers are what keep the SOFI story alive.

Q1 2026 was another record quarter. Besides the revenue and earnings growth, SoFi posted record total loan originations of $12.2 billion. Management also highlighted an 18th consecutive quarter above the Rule of 40, showing the company is combining growth and margin better than many fintech peers.

The quarter also showed that SoFi is not relying on one single lever. In Q1, Financial Services segment revenue rose 41% year over year, while the company’s Loan Platform Business contributed $140.8 million to adjusted net revenue. That matters because the broader the revenue base becomes, the stronger the argument that SOFI should trade as a diversified platform rather than as a pure lender.

Recent News: More Than Just Earnings

SoFi has also stayed active on the product and innovation side.

On May 27, 2026, the company announced that SoFiUSD became available to members, calling it the first time a U.S. national bank-issued stablecoin was made available directly on a banking app. SoFi said the product was being expanded to its nearly 15 million members, which fits the broader strategy of using new financial products to deepen engagement inside the app.

Then on June 2, 2026, SoFi launched SoFi Coach, an AI-powered financial guide built into the app. Management positioned it as a tool to help members budget, save, invest, and plan, starting with SoFi Plus members. That may not move the numbers overnight, but strategically it fits the idea that SoFi wants to be the main interface through which users manage their financial lives.

Why the Growth Potential Is Still There

The growth potential comes from scale, cross-sell, and product expansion.

SoFi is still growing members at 35% and products at 39%, which is strong at its current size. It is also widening the platform: lending, deposits, investing, credit, business banking, crypto/stablecoins, and now AI-powered financial planning. The more products a member uses, the harder it becomes to view the company as a single-line business.

This is where SOFI gets interesting. If the company can keep growing members around 30%+ while lifting products per member and protecting margins, the valuation conversation could keep changing. The market tends to reward companies that move from “fast growth but messy” to “fast growth with visible earnings power,” and SoFi is trying to make that transition.

SOFI Timeline: What Has Happened Recently

January 30, 2026: SoFi reported Q4 2025 results with its first-ever $1 billion quarter, record adjusted EBITDA of $317.6 million, 13.7 million members, and issued its 2026 full-year guidance plus a medium-term outlook.

April 29, 2026: SoFi reported Q1 2026 with $1.1 billion revenue, $166.7 million net income, 14.7 million members, and 22.2 million products.

May 27, 2026: SoFi launched SoFiUSD on its platform.

June 2, 2026: SoFi launched SoFi Coach, an AI-powered financial guide.

Forecast: What Management Is Guiding To

Management’s 2026 outlook is one of the strongest reasons bulls stay interested.

For full-year 2026, SoFi said it expects:

- at least 30% member growth

- about $4.655 billion in adjusted net revenue

- about $1.6 billion in adjusted EBITDA

- about $825 million in adjusted net income

- about $0.60 in adjusted EPS

SoFi also previously laid out a medium-term framework calling for at least 30% compounded annual growth in adjusted net revenue from 2025 to 2028, along with 38% to 42% compounded annual growth in adjusted EPS over the same period, assuming no major macro changes. That is a big part of the long-term upside case.

Stock Snapshot

As of the latest market data available, SOFI was trading at $17.91, with a market cap of about $24.68 billion. That makes it far from a tiny fintech anymore, but still small enough that continued 30% growth and rising earnings could keep the rerating story alive if execution stays strong.

Analyst Rating Angle

One important point: SoFi maintains an official analyst coverage page for investors, but that page does not publish a visible company-endorsed consensus rating in the available text view. So while SOFI is clearly followed by Wall Street, the cleaner primary-source angle is to focus on management guidance and execution rather than quote a third-party consensus without source verification.

What Investors Are Really Debating

The real question is not whether SoFi is growing. It is.

The question is whether SOFI should eventually trade more like a bank, more like a fintech platform, or something in between. If investors keep seeing it primarily as a lender, the multiple may stay constrained. If they increasingly treat it as a scaled digital financial ecosystem with multiple monetization channels and recurring engagement, the upside case gets stronger.

That is why the stock keeps getting talked about.

Bottom Line

SOFI is still a debated stock, but the business keeps giving bulls more ammunition.

The company is growing quickly, it is profitable, it is cross-selling successfully, and it continues to launch new products that deepen the ecosystem. Q1 2026 reinforced that story with 43% revenue growth, 35% member growth, and 39% product growth, while management maintained a strong full-year outlook.

That does not mean the stock is risk-free. But if SoFi keeps executing anywhere close to its current pace, it becomes harder to dismiss it as just another overhyped fintech.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}