- Nickel is not just an EV metal — it is a strategic supply-chain choke point, with over 80% of global processing capacity located outside North America.

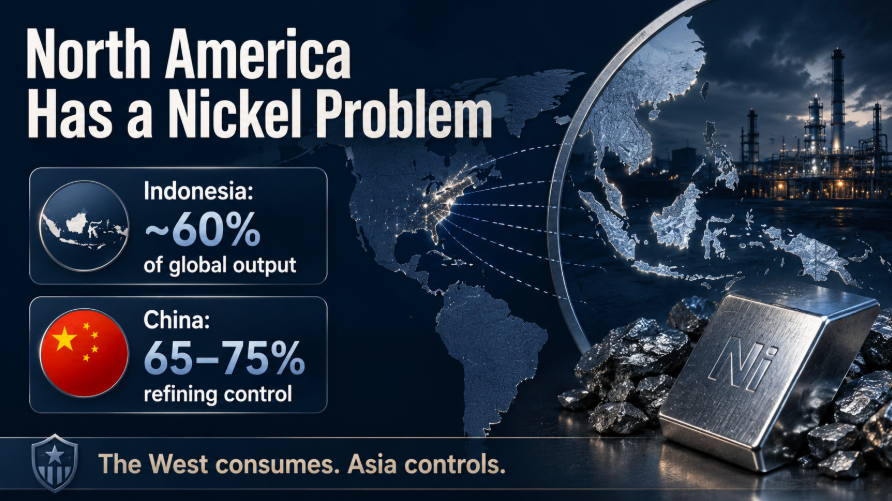

- Indonesia produces ~59–60% of global nickel (~2.3–2.4 million tonnes annually), while China controls an estimated 65–75% of refining capacity across key nickel products.

- Nusa Nickel is positioning itself as a rare North American-owned, revenue-generating operator and trader inside Indonesia’s core nickel ecosystem, where most global supply growth is occurring.

The Big Picture

North America has a critical minerals problem, and it’s not subtle—it’s structural.

The U.S. and Canada consume hundreds of thousands of tonnes of nickel annually across EVs, defense systems, aerospace, and industrial manufacturing, yet collectively account for less than 5–7% of global mine supply. Meanwhile, Indonesia produces roughly 2.3–2.4 million tonnes per year, representing ~59–60% of global output, and holds approximately 42% of global reserves, estimated at over 55 million tonnes.

China, on the other hand, dominates refining capacity across most critical minerals, including nickel processing chains such as nickel pig iron (NPI), mixed hydroxide precipitate (MHP), and Class 1 nickel. Estimates suggest China controls 65–75% of global nickel refining capacity, depending on the product category.

Put simply: the West consumes, Asia controls.

This is not just about supply shortages—it’s about who controls pricing, processing, and downstream leverage. North America talks about “friend-shoring,” but the reality is that a large portion—often 50–70%+—of nickel flowing into Western supply chains still passes through Chinese-controlled refining or Indonesian ecosystems heavily influenced by Chinese capital.

That’s the uncomfortable reality investors need to understand.

And it’s exactly where Nusa Nickel becomes controversial—and potentially interesting.

The company claims to be North America’s only revenue-generating nickel operator and licensed trader inside Indonesia’s core nickel district. If that holds up, it puts Nusa in a very small category: a Western-facing platform operating directly inside the most important nickel supply hub on the planet.

This matters because building a new mine in North America can take 10–15 years, cost $1–3 billion+, and face permitting delays, while Indonesia is already producing millions of tonnes annually and scaling faster than any other jurisdiction.

If the West wants leverage, it cannot wait a decade—it has to plug into existing supply.

Why Nickel Still Matters

Nickel sentiment has been volatile, but the fundamentals are still massive.

Prices have swung from over $30,000 per tonne in 2022 to below $20,000 per tonne in recent periods. Indonesia flooded the market with supply. EV battery chemistry shifted toward LFP, reducing nickel intensity in some segments. That narrative scared a lot of investors out of the space.

But the numbers tell a different story.

Roughly 68–72% of global nickel demand (~2.5–2.7 million tonnes annually) still goes into stainless steel, not EVs. Batteries account for roughly 10–15% of demand, with the remainder spread across aerospace alloys, defense systems, electronics, and infrastructure.

Even with LFP growth, high-performance batteries still rely on nickel-rich chemistries like NMC and NCA, which can contain 30–80 kg of nickel per EV, depending on battery design.

Nickel demand isn’t disappearing—it’s diversifying across sectors tied directly to GDP growth, industrial output, and military capability.

That makes nickel less of a “trend metal” and more of a backbone industrial commodity with strategic implications.

Why Indonesia Is the Center of the Nickel Story

Indonesia is not just important—it is dominant.

Global nickel mine production reached approximately 3.9 million tonnes in 2025, with Indonesia contributing roughly 2.3–2.4 million tonnes of that total. The country drove a ~13% year-over-year production increase, adding hundreds of thousands of tonnes of new supply.

Indonesia also holds around 42% of global nickel reserves, estimated at over 55 million tonnes, meaning its dominance is not temporary—it is structural and long-term.

Any serious nickel strategy that ignores Indonesia is fundamentally flawed.

North America can build domestic mines, fund refining projects, and sign bilateral agreements, but none of that changes the fact that the largest, fastest-growing, lowest-cost nickel supply base—often producing at costs below $10,000–$12,000 per tonne—is in Indonesia.

That is why Nusa Nickel’s positioning matters—it is not trying to create hypothetical exposure to nickel; it is operating inside the core supply region that actually moves the market.

The China Problem

This is where things get uncomfortable.

China has spent decades building dominance across critical mineral refining and downstream industrial capacity. In many cases, China controls 60–90% of global refining capacity across key energy-transition metals.

Nickel is slightly different because Indonesia is the primary source, but Chinese companies have been deeply involved in financing, building, and operating Indonesia’s nickel processing infrastructure—often accounting for 50%+ of major processing projects.

That creates a strategic bottleneck.

If North America wants secure supply for EVs, defense systems, aerospace, and grid infrastructure, it cannot rely entirely on supply chains controlled or financed by geopolitical competitors.

This is not about eliminating China—that’s unrealistic.

It’s about reducing dependency.

North America needs alternative access points into Indonesia’s nickel ecosystem that are not fully controlled by Chinese capital. It needs operators, traders, and platforms that allow Western capital to participate directly in supply.

That is exactly the niche Nusa Nickel is trying to fill.

What Nusa Nickel Actually Does

Nusa Nickel is not a typical early-stage mining junior.

The company focuses on the sourcing, production, and sale of lateritic nickel material, and it operates as a licensed nickel trader in Indonesia. That means it can source material not only from its own operations but also from third-party producers, giving it flexibility and scale potential beyond a single asset.

This creates two revenue pathways:

- Operating exposure (production)

- Trading exposure (third-party sourcing and sales)

That distinction matters because most junior mining companies are pre-revenue and dependent on a single project reaching production years down the line. Nusa claims it is already generating revenue, already operating, and already licensed to trade within Indonesia.

Key positioning points include:

- revenue-generating nickel operation

- licensed nickel trading platform

- exposure to Indonesia’s integrated nickel ecosystem

- access to Class 1 nickel and MHP supply chains

- Canadian-owned operating structure

- multiple pathways to scale production and trading volumes

This is less about “finding nickel” and more about building a platform inside an existing supply chain that already dominates global markets.

Why North America Should Care

North America’s critical minerals strategy cannot be purely domestic—it simply doesn’t scale fast enough.

Permitting timelines can stretch 10–15+ years, capital costs can exceed $1–3 billion per project, and local opposition can delay projects indefinitely. Meanwhile, Asia continues to build processing capacity at speed and scale, often completing projects in 2–5 years.

A realistic strategy has to include multiple layers:

- domestic mining development

- refining and processing capacity

- allied supply agreements

- recycling infrastructure

- diversification away from China-controlled supply chains

- direct participation in key producing regions

Nusa Nickel fits into the last category.

It provides a potential entry point for North American capital into Indonesia’s nickel ecosystem through a Canadian-owned platform that is already operating and trading.

That is fundamentally different from a typical exploration story.

Why This Is Bigger Than EVs

The biggest mistake investors make is treating nickel purely as an EV battery play.

That view ignores the fact that ~70% of global nickel demand (~2.5–2.7 million tonnes) comes from stainless steel, which is tied directly to construction, infrastructure, and industrial output.

Nickel is also critical for:

- aerospace alloys (high-temperature superalloys)

- defense systems (jet engines, armor plating)

- electronics manufacturing

- energy infrastructure

Even if EV demand fluctuates, these sectors continue to drive baseline demand.

Recent market data shows that nickel inventories have surged, with combined LME and Shanghai exchange inventories reaching 468,600 tonnes, the highest level since 2015. That represents roughly 12% of annual global demand, highlighting the scale of short-term oversupply.

Short-term oversupply does not eliminate long-term strategic importance.

The Indonesia Advantage

Indonesia’s dominance is not accidental—it is structural.

The country offers:

- ultra-low-cost production (often <$12,000 per tonne)

- aggressive industrial policy

- rapid infrastructure buildout

- integrated mining-to-processing supply chains

This combination has allowed Indonesia to scale faster than any other nickel-producing region, adding hundreds of thousands of tonnes of new capacity annually.

North America has capital, technology, and demand. Indonesia has the resource base and production capacity.

The opportunity is connecting those two systems.

That is the core Nusa Nickel thesis.

The Strategic Angle: North American Capital, Indonesian Nickel

Nusa Nickel sits in a unique position between two worlds.

It is North American-owned and investor-facing, but it operates and trades inside Indonesia’s nickel ecosystem. That combination could become increasingly valuable if Western governments and corporations push harder for supply-chain diversification.

This is not just about pricing—it is about:

- supply security

- jurisdictional diversification

- access to physical material

- participation in upstream supply

- reduced reliance on China-linked processing

- exposure to Class 1 nickel and MHP supply chains

The licensed trading component is particularly important because it allows Nusa to scale beyond a single asset and participate in broader market flows potentially measured in hundreds of thousands of tonnes annually.

The Bull Case

The bull case is straightforward and tied directly to geopolitics and supply chains.

If North America becomes more aggressive about securing critical minerals and reducing dependence on China-linked supply chains, then platforms operating inside Indonesia but aligned with Western capital could become strategically valuable.

Nusa already claims:

- revenue-generating operations

- licensed trading capability

- exposure to the world’s largest nickel district (~60% of global supply)

- Canadian ownership structure

- multiple scaling pathways

If the company can grow production, expand trading volumes, secure offtake agreements, and position itself as a preferred Western access point into Indonesian nickel, the upside could be significant.

The Bear Case

The risks are real and should not be ignored.

Indonesia is a complex jurisdiction with shifting policies, export controls, and regulatory risks. Environmental scrutiny is increasing, and Chinese capital is already deeply embedded in the ecosystem.

On top of that, nickel is a cyclical commodity.

The current inventory overhang of 468,600 tonnes—equivalent to roughly 10–12% of annual demand—shows how quickly supply can outpace demand, crushing prices and margins.

Nusa still needs to prove it can:

- scale production efficiently

- maintain margins in volatile markets

- navigate Indonesian regulatory dynamics

- build durable commercial relationships

This is not a risk-free story—it is a high-risk, high-reward positioning play.

Why Nusa Nickel Could Be Different

What makes Nusa stand out is not just nickel exposure—it is the combination of factors:

- North American ownership

- Indonesian operations

- revenue generation

- licensed trading capability

- positioning inside the world’s dominant nickel district (~60% of supply)

- exposure to key supply chains like Class 1 nickel and MHP

Most North American critical-minerals companies are either early-stage explorers or long-dated development projects that may take 10+ years to reach production.

Nusa is already inside the system that matters.

What Investors Should Watch Next

Key metrics that actually matter:

- production growth rates (% YoY)

- trading volumes (tonnes per year)

- revenue growth and margins (%)

- offtake agreements (contracted tonnes)

- expansion of third-party sourcing

- exposure to higher-value nickel products

- Indonesian partnerships and regulatory positioning

- validation of responsible sourcing claims

The core question is simple:

Can Nusa Nickel become a scalable bridge between North American capital and Indonesian nickel supply measured in hundreds of thousands of tonnes annually?

If yes, it becomes more than a niche operator—it becomes a strategic platform.

Bottom Line

North America needs nickel, but it does not control nickel.

Indonesia produces roughly 60% of global supply (~2.3–2.4 million tonnes annually). China dominates refining with 65–75%+ control across key processing stages. The West is structurally dependent on both.

That is the reality investors need to price in.

Nusa Nickel is attempting to build a North American-owned, revenue-generating operating and trading platform inside the world’s most important nickel district.

That is not just a mining story—it is a geopolitical supply-chain play.

If North America is serious about reducing dependency and securing critical minerals, it needs exposure where the supply actually exists.

Nusa Nickel is trying to be that exposure.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. Mining, critical minerals, and commodity-related investments are speculative and may involve substantial volatility, jurisdictional risk, financing risk, and loss of capital. Always conduct your own research and consult a licensed financial advisor before making investment decisions.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}