- Copper demand is being pulled higher by AI data centers, electrification, grid expansion, EVs, and defense.

- Smaller copper names can offer more upside torque than the commodity itself, but with much higher risk.

- Copper Quest, Faraday Copper, Trekor Metals, Ivanhoe Electric, and Surge Copper each offer a different way to play the copper cycle.

Why Copper Is Becoming One of the Most Important Metals Again

Copper is no longer just an old-school industrial metal.

It is becoming one of the key materials behind the next phase of infrastructure.

AI data centers need massive power systems. Power grids need upgrades. Electric vehicles need copper. Renewable energy needs copper. Transmission lines need copper. Defense systems need copper. New mines take years to permit and build.

That creates a simple but powerful setup: demand keeps rising, but new supply is difficult to bring online quickly.

This is why copper has become one of the most strategic metals in the market.

The biggest mining companies already understand this. Large-cap miners have been trying to add copper exposure through acquisitions, partnerships, and development projects. But for investors looking for more upside, the smaller copper names may be more interesting.

The trade-off is risk.

Copper juniors and developers can move much more than the copper price itself, but they also carry exploration, permitting, financing, construction, and execution risk.

This article looks at five copper stocks with different kinds of exposure:

- Copper Quest Exploration

- Faraday Copper

- Trekor Metals

- Ivanhoe Electric

- Surge Copper

Quick Watchlist Table

| Company | Ticker | Recent Price | 1Y Performance | Market Cap | Main Angle |

|---|---|---|---|---|---|

| Copper Quest Exploration | CNSX: CQX | C$0.090 | 0.00% | C$10.07M | Speculative junior copper-gold exploration |

| Faraday Copper | TSE: FDY | C$6.15 | +497.09% | C$1.8B | U.S. copper development with BHP validation |

| Trekor Metals | TSE: TKO | C$9.74 | +117.52% | C$3.56B | Producer + Florence Copper ramp-up |

| Ivanhoe Electric | NYSE American: IE | US$9.55 | +3.02% | US$1.51B | Advanced U.S. copper development |

| Surge Copper | CVE: SURG | C$0.57 | +185.00% | C$218M | Large-scale Canadian copper development |

1. Copper Quest Exploration — CNSX: CQX

Copper Quest Exploration is the most speculative name on this list.

That is also why it may offer the most torque if the company can execute.

The stock recently traded at C$0.090, with a market cap of C$10.07M and a 0.00% move over the past year according to the screenshot. That is important because Copper Quest has not had the same explosive move as some other copper names on this list.

Faraday Copper is up nearly 500% over the past year.

Surge Copper is up 185%.

Trekor Metals is up 117.52%.

Copper Quest, by contrast, is still sitting around C$0.090, making it the earlier-stage, more speculative catch-up candidate.

The company is focused on building a North American critical minerals portfolio, with copper and gold projects across Canada and the United States. Copper Quest’s website highlights more than 39,000 hectares of prime exploration territory, a projected 20% copper demand increase by 2030, and 70% ownership of strategic assets across key regions.

One of the key assets is the Kitimat Copper-Gold Project in northwestern British Columbia. Copper Quest recently expanded Kitimat by adding 3,847.41 hectares, increasing the project size by 130%. The Kitimat Copper-Gold Project now covers 6,801.41 hectares within the Skeena Mining Division.

That matters because Kitimat is located in a strong infrastructure region. The area is close to Kitimat, British Columbia, a deep-water port and industrial hub, which could matter if future exploration creates a more serious development story.

Copper Quest also has an AI angle, with the company using modern geological targeting tools to identify potential copper-gold systems more efficiently.

Key numbers and catalysts:

- recent price: C$0.090

- market cap: C$10.07M

- 1-year performance: 0.00%

- more than 39,000 hectares highlighted on company website

- Kitimat expanded by 3,847.41 hectares

- Kitimat project size increased by 130%

- Kitimat now covers 6,801.41 hectares

- copper-gold exploration focus

- North American critical minerals portfolio

- AI-driven geological targeting angle

- early-stage exploration upside

The bull case is simple: Copper Quest is still early, but it has multiple shots on goal.

The bear case is also obvious. Early-stage exploration companies can burn capital for years without creating a mineable discovery. Financing, dilution, commodity sentiment, and weak exploration results can all hurt the stock.

Copper Quest is not the safest copper name, but if investors want asymmetric exposure to a junior copper-gold exploration story that has not already run like some peers, this is where the risk/reward starts to look interesting.

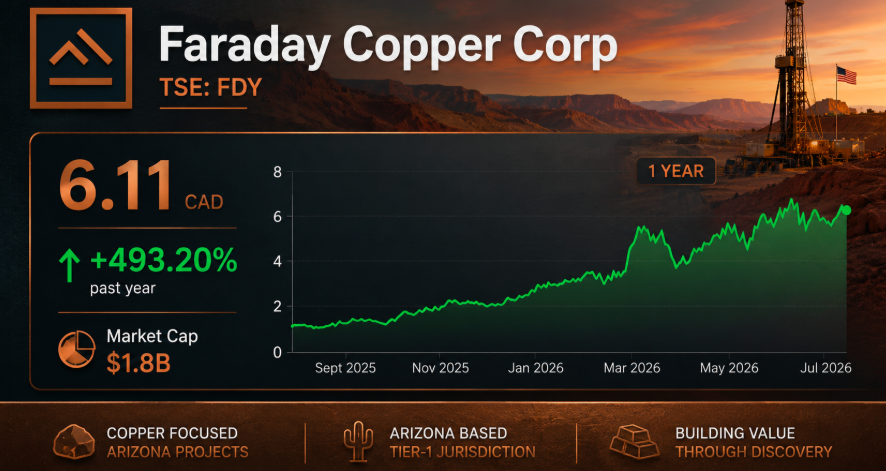

2. Faraday Copper — TSE: FDY

Faraday Copper is one of the strongest momentum names in this basket.

The stock recently traded at C$6.15, with a market cap of C$1.8B, up 497.09% over the past year according to the screenshot. That is a massive move, and it completely changes how investors should view the setup.

This is no longer an undiscovered copper story.

The market has already started rewarding Faraday.

The company’s flagship asset is the Copper Creek Project in Arizona, located in one of the most important copper jurisdictions in the United States. Copper Creek is a large project with serious exploration history.

Faraday reports that Copper Creek covers approximately 78 square kilometers, with a resource area around 3 kilometers long and open in all directions. The property hosts multiple breccia and porphyry copper deposits, with more than 560 drill holes and over 200,000 meters of drilling completed to date.

The exploration scale is one of the most interesting parts of the story.

More than 320 breccias have been identified across the property, but less than 15% have been drill-tested. Only 17 breccias are currently included in the mineral resource estimate.

That suggests Copper Creek still has exploration upside even though it is already an advanced project.

Faraday became even more interesting after BHP agreed to transfer its San Manuel property in Arizona to Faraday. In exchange, BHP will receive shares equivalent to a 30% equity interest in Faraday on a fully diluted basis, plus associated shareholder and offtake rights. Completion is expected in the quarter ending September 30, 2026, subject to customary conditions.

That is a huge validation signal.

BHP is one of the world’s largest miners. When a major miner takes this kind of position in a junior copper developer, the market pays attention.

Key numbers and catalysts:

- recent price: C$6.15

- market cap: C$1.8B

- 1-year performance: +497.09%

- Copper Creek Project in Arizona

- approximately 78 km² property

- approximately 3 km resource area

- more than 560 drill holes

- over 200,000m drilled

- more than 320 breccias identified

- less than 15% of breccias drill-tested

- 17 breccias currently included in the resource estimate

- BHP to receive 30% fully diluted equity interest

- transaction expected to close in quarter ending September 30, 2026

- potential Arizona copper hub strategy

The bull case is that Faraday becomes a strategic U.S. copper development platform backed by major-miner interest.

The bear case is valuation and execution. After a nearly 500% 1-year move, investors are no longer buying at the bottom. The project still needs permitting, financing, development work, and long-term execution.

The investor angle is clear: Faraday is not just a copper story — it is a U.S. copper story with major-miner validation.

3. Trekor Metals — TSE: TKO

Trekor Metals is the corrected name in the article.

This was formerly Taseko Mines Limited. The company changed its name to Trekor Metals Limited in late June 2026, while keeping its ticker symbols unchanged: TKO on the TSX, TGB on the NYSE American, and TKO on the LSE.

That means the business thesis from the earlier article still applies.

The name changed.

The copper exposure did not.

Trekor recently traded at C$9.74, up 117.52% over the past year according to the screenshot. The company had a market cap of C$3.56B.

This makes Trekor the most established and production-oriented name on the list.

Unlike Copper Quest, Faraday, Ivanhoe Electric, or Surge Copper, Trekor is not just a development or exploration story. It is already a mid-tier copper producer.

The company operates the Gibraltar Mine in British Columbia. Gibraltar has been described as the second-largest open-pit copper mine in Canada.

The key growth asset is Florence Copper in Arizona.

Florence is important because it is one of the newest sources of U.S. copper supply. The project began producing copper cathode in early 2026, with first copper cathodes harvested in late February. Florence Copper described this as the first new copper production from a greenfield facility in the United States since 2008.

The project uses in-situ copper recovery, where solution is used underground to recover copper without traditional open-pit mining or smelting. The copper solution is processed on site into copper cathode.

At full design capacity, Florence is expected to produce around 85 million pounds of copper cathode per year.

Key numbers and catalysts:

- recent price: C$9.74

- 1-year performance: +117.52%

- market cap: C$3.56B

- P/E ratio shown: 249.17

- formerly Taseko Mines Limited

- tickers unchanged: TSE: TKO / NYSE American: TGB / LSE: TKO

- operates Gibraltar Mine in British Columbia

- Gibraltar described as Canada’s second-largest open-pit copper mine

- Florence Copper in Arizona

- first cathode harvest in February 2026

- first new U.S. greenfield copper production since 2008

- Florence design capacity around 85 million lb/year

The bull case is that Trekor offers investors real copper production plus new U.S. copper supply growth.

The bear case is that the stock has already moved strongly, and production ramp-ups can still disappoint. Florence must prove recoveries, costs, volumes, and operational consistency.

Trekor may not be the smallest copper name, but it is one of the most tangible — real production, a major Canadian mine, and a new U.S. copper cathode asset ramping now.

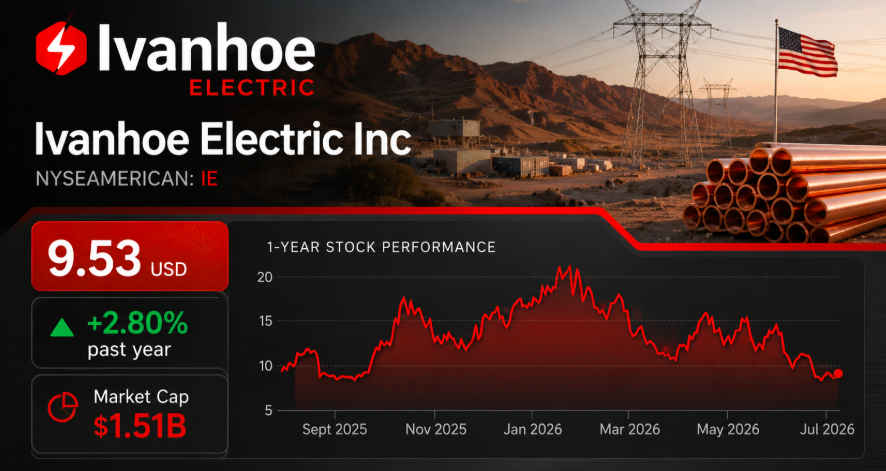

4. Ivanhoe Electric — NYSE American: IE / TSX: IE

Ivanhoe Electric is one of the most important U.S. copper development names to watch.

The stock recently traded at US$9.55, up 3.02% over the past year according to the screenshot. Its market cap was US$1.51B.

That is a very different setup from Faraday.

Faraday is up almost 500% over the past year.

Ivanhoe Electric is only up 3.02%, despite having a major U.S. copper development asset.

That makes Ivanhoe Electric more controversial. The stock has been much higher, but it is now trading much closer to its lower range than its former highs.

The flagship asset is the Santa Cruz Copper Project in Arizona.

Santa Cruz stands out because it is an advanced project in a strong jurisdiction with a clear domestic copper supply angle. The company is targeting construction in 2026 and first copper cathode production in 2028.

Ivanhoe Electric’s project economics are meaningful. The Santa Cruz pre-feasibility study outlined a project expected to produce approximately 1.4 million tonnes of copper cathode over a 23-year mine life, with an after-tax NPV of roughly US$1.4B and an IRR of approximately 20% at a base copper price of US$4.25/lb.

Ivanhoe Electric also received a Letter of Interest from the Export-Import Bank of the United States for potential debt financing of up to US$825M for Santa Cruz.

That is a major number.

It shows how strategic domestic copper supply has become in the U.S.

Key numbers and catalysts:

- recent price: US$9.55

- 1-year performance: +3.02%

- market cap: US$1.51B

- Santa Cruz Copper Project in Arizona

- targeting construction in 2026

- first copper cathode projected by 2028

- approximately 1.4M tonnes copper cathode over mine life

- 23-year mine life

- after-tax NPV of approximately US$1.4B

- IRR of approximately 20%

- base copper price assumption of US$4.25/lb

- potential US$825M EXIM Bank financing indication

The bull case is that Ivanhoe Electric becomes one of the key public market names tied to rebuilding U.S. copper supply.

The bear case is that even advanced copper projects can face financing, construction, cost, and permitting risk. The stock’s weak performance versus other copper names shows that investors are still waiting for more proof.

The investor angle: if the market keeps rewarding domestic critical-mineral projects, Ivanhoe Electric belongs on the copper watchlist.

5. Surge Copper — CVE: SURG

Surge Copper is the Canadian development story in this basket.

The stock recently traded at C$0.57, with a market cap of C$218M, up 185.00% over the past year according to the screenshot. That is a major move, though still less extreme than Faraday’s 497.09% run.

The company’s flagship asset is the Berg Copper Project in central British Columbia, supported by its broader district-scale portfolio that also includes the Ootsa Project.

Berg is now at the pre-feasibility stage, which makes it more advanced than an early exploration story but still earlier than a producing mine.

The June 2026 pre-feasibility study is the key catalyst.

Surge reported after-tax economics for Berg, including an after-tax NPV8% of approximately C$4.6B and an after-tax IRR of approximately 24%. The PFS also outlined a 2.9-year payback, average annual revenue of around C$1.9B, and life-of-mine free cash flow of C$16.9B on an unlevered basis.

The project itself is a large-scale, stand-alone open-pit mine and concentrator concept. Surge says Berg is supported by regional road infrastructure and planned connection to British Columbia’s low-carbon hydroelectric power grid.

That last point matters.

Copper projects with access to lower-carbon power may become more attractive as miners and investors increasingly care about emissions, ESG pressure, and project-level operating costs.

Key numbers and catalysts:

- recent price: C$0.57

- market cap: C$218M

- 1-year performance: +185.00%

- Berg Copper Project in British Columbia

- 100%-owned flagship project

- June 2026 pre-feasibility study completed

- after-tax NPV8% of approximately C$4.6B

- after-tax IRR of approximately 24%

- payback of 2.9 years

- average annual revenue of approximately C$1.9B

- life-of-mine free cash flow of approximately C$16.9B

- stand-alone open-pit mine and concentrator concept

- planned connection to low-carbon hydroelectric power

- Ootsa Project adds district-scale exposure

The bull case is that Surge has a large copper development story with serious economics in Canada.

The bear case is that big projects require big capital. The market may discount the economics until Surge shows a clearer path to permitting, financing, strategic partnerships, and development.

Surge may be one of the more obvious “valuation gap” copper juniors if investors start hunting for large-scale copper development stories again.

Bottom Line

Copper is becoming one of the most important metals in the world economy.

The problem is that new supply is hard to build.

That creates opportunity for companies positioned across the copper development curve.

Copper Quest, Faraday Copper, Trekor Metals, Ivanhoe Electric, and Surge Copper each offer a different way to play the copper cycle — from early-stage exploration to U.S. production ramp-up.

The stock charts also show very different setups.

Faraday is already up 497.09% over the past year.

Surge is up 185.00%.

Trekor is up 117.52%.

Ivanhoe Electric is only up 3.02%.

Copper Quest is flat at 0.00% over the past year.

That makes the basket more interesting because not every name has already moved the same way.

This is not a low-risk basket.

Copper juniors and developers can be volatile, capital-intensive, and highly sensitive to commodity prices.

But if copper demand continues to rise and strategic capital keeps moving into the sector, these are the kinds of names investors may start watching more closely.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. Copper exploration and development stocks are speculative and may involve substantial risk, including loss of capital. Always conduct your own research and consult a licensed financial advisor before making investment decisions.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}