- Gold already had its “everyone wants in” moment, pushing to record highs before pulling back sharply toward the $4,000/oz battleground.

- The gold commodity trade may now look less exciting than AI, space, defense, nuclear, and other high-beta sectors — but that does not mean the gold opportunity is dead.

- If investors still want gold exposure with maximum ROI potential, small-cap gold stocks and select smaller-platform producers may offer more upside torque than bullion, ETFs, or major producers.

Hot Take: Gold Itself May Not Be the Best Gold Trade Anymore

Gold had a monster run.

It became the inflation hedge, the geopolitical hedge, the central-bank hedge, the de-dollarization trade, and the “everything is broken” trade all at once.

But here is the uncomfortable part: when everyone already knows the story, the easy money may already be gone.

Gold recently pushed into record-high territory before pulling back hard. By late June 2026, spot gold was hovering around the $4,000/oz level after dropping 11.2% in June and heading for its steepest quarterly loss in 13 years.

That matters.

Gold may still be structurally strong, but from an investor psychology standpoint, the trade no longer feels as explosive as it did when the metal was breaking records.

Capital is now chasing other sectors with more obvious momentum:

- AI infrastructure

- space stocks

- defense tech

- nuclear energy

- grid power

- quantum computing

- data centers

- high-beta growth stocks

So the real question is not whether gold still matters.

The better question is: if gold remains relevant, where is the highest-upside version of the trade?

The answer may not be bullion.

It may be small-cap gold stocks and smaller gold platforms with company-specific catalysts.

Why Small-Cap Gold Stocks Can Beat the Commodity

If gold rises 10%, bullion rises roughly 10%.

But a small-cap gold stock can move 50%, 100%, 200%, or more if the company hits the right catalyst.

That is the entire appeal.

Small-cap gold stocks combine commodity exposure with company-specific upside:

- permitting progress

- drill results

- resource expansion

- feasibility updates

- mine restarts

- production ramp-ups

- takeover speculation

- capital market re-ratings

That is why small-cap gold names can offer more ROI potential than simply buying the metal.

The trade-off is obvious: risk.

These stocks are volatile, illiquid, capital-hungry, and often one bad update away from getting crushed. But if the goal is maximum upside and not maximum safety, this is where the leverage is.

This list focuses on five gold stocks with different kinds of torque:

- Falco Resources

- West Red Lake Gold Mines

- Nevada King Gold

- Lahontan Gold

- i-80 Gold Corp

Four are classic small-cap gold names.

One, i-80 Gold, is larger — but still offers leveraged exposure as a Nevada-focused platform aiming to scale toward mid-tier production.

Quick Watchlist Table

| Company | Ticker | Price | 1Y Performance | Market Cap | Main Upside Angle |

|---|---|---|---|---|---|

| Falco Resources | CVE: FPC | C$0.48 | +92.00% | C$166.55M | Massive feasibility-stage Québec project |

| West Red Lake Gold Mines | CVE: WRLG | C$0.63 | -25.88% | C$260.17M | Production ramp-up at Madsen |

| Nevada King Gold | CVE: NKG | C$0.73 | -8.75% | C$73.27M | Nevada drilling/resource growth |

| Lahontan Gold | CVE: LG | C$0.36 | +265.00% | C$157.75M | Nevada oxide-gold development |

| i-80 Gold Corp | TSE: IAU | C$2.03 | +141.67% | C$1.75B | Nevada platform / mid-tier producer path |

1. Falco Resources — CVE: FPC

Falco Resources may be the most controversial name on this list because the valuation gap looks almost absurd on paper.

The company’s flagship asset is the Horne 5 Project in Rouyn-Noranda, Québec.

This is not a tiny early-stage drill story. Horne 5 is a large underground gold-led polymetallic project in one of Canada’s best-known mining regions.

The stock recently traded at C$0.48, with a market cap of C$166.55M. Over the past year, Falco is up 92.00%, with a 52-week range between C$0.22 and C$0.64.

The updated 2026 feasibility study is the reason Falco stands out.

Using a base-case gold price of US$3,600/oz, Falco reported:

- after-tax NPV5% of C$3.35 billion

- after-tax IRR of 28.2%

- estimated cash flow of C$6.4 billion

- 15-year underground mine life

- payback period of 3.3 years

- initial capital cost of roughly C$1.75 billion

Now compare that with a market cap of C$166.55M.

That is the bull case in one sentence: a company valued around C$166M is sitting on a feasibility-stage project with a reported after-tax NPV of C$3.35B.

That does not mean the stock is automatically cheap. Large mining projects are expensive, complicated, and slow. Falco still needs permitting, financing, construction capital, and execution.

But for investors looking for gold exposure with real project scale, Falco is exactly the kind of name that can get attention if gold sentiment turns back up.

The controversial Reddit angle is simple: if Horne 5 was owned by a larger producer, would the market value it very differently?

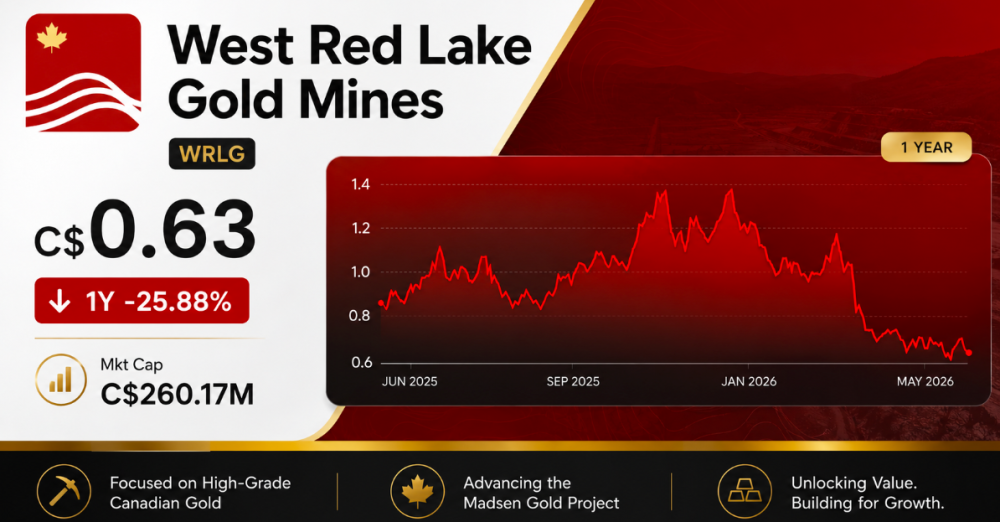

2. West Red Lake Gold Mines — CVE: WRLG

West Red Lake Gold Mines is not a pure exploration gamble.

That is what makes it interesting.

The company owns the Madsen Mine in Ontario’s Red Lake district, and Madsen reached commercial production in January 2026.

This gives West Red Lake something many juniors do not have: actual production.

The stock recently traded at C$0.63, with a market cap of C$260.17M. Over the past year, the stock is down 25.88%, with a 52-week range between C$0.59 and C$1.49.

That weak 1-year performance is important.

It makes West Red Lake more controversial than the obvious momentum names. The stock has sold off hard, but the underlying company is still trying to prove a production ramp-up at Madsen.

Key numbers:

- 2025 restart production of roughly 20,000 oz gold

- 2025 gold sales revenue of around US$73M

- average realized gold price of about US$3,650/oz in 2025

- 7,200 oz poured in Q4 2025

- Q4 gold sales revenue of around US$30M

- 2026 production guidance of 35,000 to 45,000 oz gold

- longer-term platform target of roughly 120,000 oz per year

- implied growth of around 300% from 2026 production levels if the platform target is reached

That is a very different setup from a drill-only explorer.

West Red Lake is a mine ramp-up story. The stock could re-rate if Madsen proves it can produce consistently, control costs, and grow into a larger Red Lake platform.

The upside is operational leverage.

The risk is also operational leverage.

Mine restarts can disappoint. Costs can surprise. Throughput can lag. Guidance can miss. Investors may punish the stock quickly if Madsen underdelivers.

But if gold stays strong and West Red Lake executes, it could be one of the more direct small-cap ways to play production growth.

The Reddit argument: this may be less “exciting” than a discovery stock, but real ounces can matter more than drill hype.

3. Nevada King Gold — CVE: NKG

Nevada King Gold is one of the cleaner exploration-growth stories in the group.

The company is focused on the Atlanta Gold Mine Project in Nevada, a past-producing open-pit oxide gold project located along the Battle Mountain Trend.

Nevada matters because the market tends to give premium attention to gold projects in mining-friendly U.S. jurisdictions.

The stock recently traded at C$0.73, with a market cap of C$73.27M. Over the past year, Nevada King is down 8.75%, with a 52-week range between C$0.60 and C$1.38.

That makes the setup interesting.

The stock is not at its highs. It has pulled back from a strong 52-week range, but the project still has a defined resource and a major drill program.

Nevada King reports:

- 1.02M oz gold measured and indicated

- 27.7M tonnes grading 1.14 g/t Au

- 99,000 oz gold inferred

- 3.6M tonnes grading 0.84 g/t Au

- Phase 4 drill program doubled to 40,000m

- prior plan was 20,000m

- recent financing of roughly C$16M

- strategic investment from Centerra Gold of roughly C$10M

That 40,000m drill program is the catalyst.

If Atlanta expands, Nevada King could move from “interesting oxide resource” to a much bigger district-scale story.

The bull case is resource growth.

The bear case is simple: the market has already seen a lot of gold explorers talk big, drill hard, and fail to create real scale.

Nevada King needs the drill bit to keep proving the story.

The controversial Reddit angle: if investors want high-upside gold exposure, a 40,000m Nevada drill program may be more exciting than buying a gold ETF after the metal already ran.

4. Lahontan Gold — CVE: LG

Lahontan Gold is the momentum name in this group.

The company is a Nevada oxide-gold development story with real numbers behind it.

The flagship asset is the Santa Fe Mine Project in Nevada’s Walker Lane.

This is not just a blank map with gold-colored arrows on a presentation.

The stock recently traded at C$0.36, with a market cap of C$157.75M. Over the past year, Lahontan is up 265.00%, with a 52-week range between C$0.095 and C$0.52.

That is the kind of move that makes Reddit split in two.

Bulls will say the market is finally waking up to a Nevada oxide-gold development story.

Bears will say the easy move may already have happened.

Santa Fe has:

- 1.539M oz AuEq indicated resource

- 411,000 oz AuEq inferred resource

- nearly 2M oz AuEq total resource base

- 48.393M tonnes grading 0.92 g/t Au and 7.18 g/t Ag in indicated resources

- 16.76M tonnes grading 0.74 g/t Au and 3.25 g/t Ag in inferred resources

- 0.99 g/t AuEq indicated grade

- 0.76 g/t AuEq inferred grade

- historic production of 359,202 oz gold

- historic production of 702,067 oz silver

- 2,569m geotechnical drill campaign completed in 2026

- 11 drill holes in that geotechnical campaign

This is why Lahontan is interesting.

The company has a meaningful resource, historical production, and a development pathway in Nevada.

It is not as speculative as a tiny microcap explorer, and not as massive in project economics as Falco, but it sits in the middle: a more advanced small-cap Nevada gold development play.

The risk is that development stories take time and capital. Investors need permitting progress, mine planning, metallurgical confidence, and eventually financing.

But if gold remains elevated, oxide-gold development stories in Nevada could continue to attract attention.

The Reddit question: after a 265% 1-year move, is Lahontan still early — or already crowded?

5. i-80 Gold Corp — TSE: IAU

i-80 Gold is the bigger and more serious name in the basket.

It is not a tiny exploration lottery ticket. It is a Nevada-focused gold company trying to build itself into a mid-tier producer through a multi-asset development plan.

The company’s portfolio includes several Nevada assets, including:

- Granite Creek

- Cove

- Ruby Hill

- Lone Tree

- Mineral Point

The stock recently traded at C$2.03, with a market cap of C$1.75B. Over the past year, i-80 is up 141.67%, with a 52-week range between C$0.76 and C$3.04.

That means i-80 is not really a small cap in the same way as Falco, Nevada King, Lahontan, or West Red Lake.

But it still belongs in this article because it offers leveraged gold exposure through a Nevada platform that is trying to scale.

The most important recent number is financing.

i-80 secured a financing package of up to US$500M to advance its development plan. The company also reported that its fully funded development plan remains on track after Q1 2026.

That changes the risk profile.

Many junior gold stocks have good projects but no money. i-80 has a large Nevada asset base and a major financing package designed to move the plan forward.

Key numbers:

- up to US$500M financing package

- US$250M Franco-Nevada royalty financing completed in Q1 2026

- US$50M allocated to Mineral Point infill drilling, engineering, and early-stage pre-permitting

- Mineral Point pre-feasibility study expected in 2027

- roughly US$133.5M trailing twelve-month revenue

- C$1.75B market cap

- multi-asset Nevada portfolio across Granite Creek, Cove, Ruby Hill, Lone Tree, and Mineral Point

This is why i-80 fits the article.

The stock is no longer a tiny moonshot, but it still offers leveraged gold exposure because the company is trying to scale into a larger Nevada producer.

The bull case is that i-80 converts its financed development plan into rising production, stronger cash flow, and a higher market valuation.

The bear case is execution. A US$500M financing package helps, but mine development, permitting, technical studies, cost control, and production ramp-ups are still difficult.

The Reddit angle is simple: if investors want gold exposure with more upside than bullion but less pure lottery-ticket risk than a tiny explorer, i-80 may be one of the cleaner Nevada platform plays.

What Investors Should Watch Next

For Falco, the key catalyst is the Québec ministerial decree and movement toward construction readiness.

For West Red Lake, investors should watch Madsen production rates, cost performance, throughput, and whether the company stays on track for 35,000–45,000 oz in 2026.

For Nevada King, the key is the 40,000m Phase 4 drill program and whether Atlanta’s oxide resource expands.

For Lahontan, investors should watch Santa Fe permitting, resource growth, mine-plan optimization, metallurgical work, and development milestones.

For i-80 Gold, the market will watch execution of the fully funded Nevada development plan, progress at Granite Creek, Cove, Ruby Hill, Lone Tree, and Mineral Point, and whether the company can convert its financing package into meaningful production growth.

Bottom Line

Gold is not dead.

But the easy gold commodity trade may be less exciting than it was when the metal was breaking records.

For investors who want safe exposure, bullion or ETFs make sense.

For investors who want maximum ROI potential, small-cap gold stocks and smaller gold platforms may be the more aggressive play.

Falco Resources, West Red Lake Gold Mines, Nevada King Gold, Lahontan Gold, and i-80 Gold each offer a different version of leveraged gold exposure.

This is not the safest way to own gold.

It is the higher-upside, higher-risk way to play the sector.

And that may be exactly why the setup is worth watching.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. Small-cap and exploration-stage mining stocks are highly speculative and may involve substantial risk, including loss of capital. Always conduct your own research and consult a licensed financial advisor before making investment decisions.

Marc has been involved in the Stock Market Media Industry for the last +5 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website.

{kind=link}