Unfortunately, war is the daily media lead. We get the numbers of dead and injured for each conflict. You might consider those just injured as ‘lucky’ if you’re like me. Au contraire. Familiar issues are traumatic brain and spine injuries. Alongside lost limbs and wounds caused by bomb debris and emotional symptoms such as PTSD and depression that may persist for years, sometimes a lifetime. (Xaigham.com)

For life-saving technologies, war has unfortunately become a growth sector. I take no pleasure in saying that.

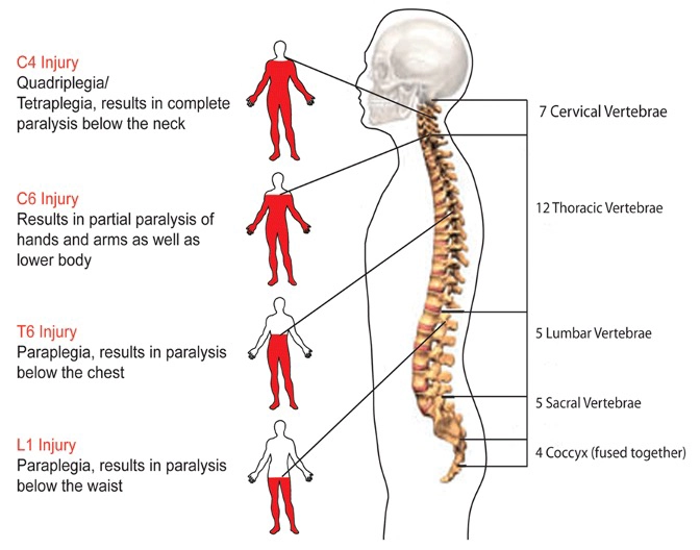

A sudden, traumatic blow to the spine (tSCI) can fracture, dislocate, crush or compress one or more of the vertebrae. A gunshot or knife wound that penetrates and cuts the spinal cord also can cause a spinal cord injury. Additional damage usually occurs over days or weeks.

The global Spinal Cord Trauma Treatment market was valued at US$ 2458.9 million in 2022 and is projected to reach US$ 3009.4 million by 2029, at a CAGR of 2.9% during the forecast period. The influence of COVID-19 and the Russia-Ukraine War were considered while estimating market sizes.

The current Middle East conflict was not included. Unfortunately, those projected growth numbers could rise significantly.

While I am using the wars and conflicts as examples of the growth of the traumatic injury market, it was already significant and this is just the US.

- A recent estimate of the annual incidence of traumatic spinal cord injury (CCI) is approximately 54 cases per one million people in the United States.

- The estimated number of people with tSCI living in the United States is approximately 302,000 persons, ranging from 255,000 to 383,000 persons.

- The average age at injury has increased from 29 during the 1970s to 43 since 2015.

- Traumatic brain injury (TBI) is defined as an alteration in brain function or other evidence of brain pathology caused by an external force. Examples of TBI include falls, assaults, motor vehicle accidents and sports injuries.

The question arises: how is this issue addressed? There are myriad companies, large and small, looking for answers.

TORONTO and HAIFA, Israel, Jan. 05, 2024 (GLOBE NEWSWIRE) — NurExone Biologic Inc. (TSXV: NRX) (FSE: J90) (NRX.V) (the “Company” or “NurExone”), a biopharmaceutical company developing biologically-guided exosome therapy for patients with traumatic spinal cord injuries.

How does it work? Stay with me; it’s pretty straightforward.

Part One: Active Ingredients

Exosomes: Exosomes, also known as extracellular vesicles, are nano-sized, naturally occurring particles in the body, secreted by cells. Exosomes, also known as extracellular vesicles, are nano-sized, naturally occurring particles in the body, secreted by cells. Can be administered non-invasively, intranasally

Part Two: Delivery

ExoTherapy: Exosomes, loaded with therapeutic molecules, cross the blood-brain barrier and reach cells and tissues for regeneration, rewiring and recovery.

Part Three: Effect

SiRNA-PTEN: The suggested PTEN inhibition-based therapeutic targets are nerve growth and regeneration after injury or damage, treatment of cardiac ischemia/reperfusion and associated disease, wound repair, and infertility.

The goal is to reverse this traumatic brain trauma as well as develop other health issues such as depression—no small accomplishment. The US FDA has granted NRX Orphan Drug Status.

The Orphan Drug Designation program provides orphan status to drugs and biologics for rare diseases that meet specific criteria. Orphan drug designation provides incentives, including:

- Tax credits for qualified clinical trials

- Exemption from user fees

- Potential for seven years of market exclusivity after approval

“Orphan-drug designation is expected to streamline our go-to-market, shorten our regulatory process, save the Company millions of dollars, and provide valuable market exclusivity. We appreciate the formal recognition of the potential impact of our therapy on the lives of patients suffering from acute spinal cord injuries,” said Dr. Shaltiel, CEO of NurExone Biologic, Ltd.

The Company also holds an exclusive worldwide license from Technion and Tel Aviv University for developing and commercializing the technology.

This technology is not only promising but appears well destined for success. In their totality, the current NRX out-front therapies could bring much relief to those seriously ‘injured’ patients who live with chronic pain and myriad challenges daily.

NurExome is a cutting-edge medical technology company. While trading has been modest, it paints a positive investment picture for the previously reasons stated. Will it pop tomorrow? No. That I can guarantee.

A savvy plan would to be to approach as a dollar-cost average investment. The deeper you dig, the more potential will become apparent.

Note Hyperlinks below.

| Stock stats Jan 5 2024 | |

| 52 Week Range | 0.1000 0.4200 |

| Volume | 7,000 |

| Avg. Volume | 4,511 |

| Market Cap | 14.475M |

| Beta (5Y Monthly) | N/A |

| PE Ratio (TTM) | N/A |

| EPS (TTM) | -0.1100 |

| Earnings Date | N/A |

| Forward Dividend & Yield | N/A (N/A) |

| Ex-Dividend Date | N/A |

| 1y Target Est | 4.01 |

| In-depth Corporate Presentation Litchfield Research |

August 30

Marc ZERBOLA CHALLANDE

Latin Metals Inc. (“Latin Metals” or the “Company”) – (TSXV: LMS) OTCQB: LMSQF) is a mineral exploration company acquiring a diversified portfolio of assets in South America utilizing a Prospect Generator model.

Using a “Prospect Generator” describes a junior mining exploration company that employs a particular business model to de-risk the exploration approach. A Prospect Generator will stake and/or acquire future mineral rights to an area they believe has significant ore-bearing potential.

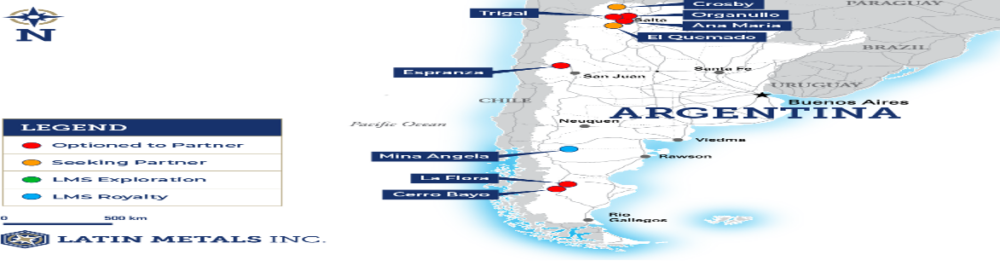

Latin Metals properties are primarily Copper and Gold in Peru and Argentina. There are detailed Corporate videos for those wishing for a quick video picture.

Peru is the world’s second-largest producer of copper, silver, and zinc and Latin America’s largest producer of gold. Peru is among the primary producers of mineral commodities in the world. Abundant mineral resources such as copper, gold, silver, and lithium are found mainly in the mountains. The mining industry in Peru has been historically significant to the nation for over 500 years and has been home to many high-grade gold and copper projects. In 2019, Peru tied with Ghana as the seventh largest gold-producing country.

Latin Metals has several properties in Peru. The Map:

The Company is very good at keeping investors informed. The most recent news announced results at its Auquis property.

Keith Henderson, the CEO, commented, “Our recent follow-up sampling program has outlined a large 1km x 1km area of consistent mineralization where 101 samples returned copper values of up to 2.37% copper and 236 ppm molybdenum, with a mean value of 0.13% copper and 6.4 ppm molybdenum. We are excited about these initial results, with many areas of this large 4,000-hectare property still unsampled.” (July 20th PR)

For closeology fans, significant players in the area are Newmont and Vale, not exactly small potatoes in the copper sector. Speaking of Copper, it appears the outlook is one of growth.

Demand for copper will double by 2035, opening up a supply gap that threatens climate goals and poses severe challenges to the Net-Zero Emissions by 2050.

This demand growth during the energy transition — a pathway toward transforming the global economy to Net-Zero Emissions by 2050 — will be particularly pronounced in the United States, China, and Europe. India will also exhibit strong copper demand growth, more from traditional copper applications than from the energy transition. (S&P Global)

It appears that good-quality copper assets could well make sense in a diversified portfolio.

LMS has a like number of properties in Argentina. Somewhat more advanced than its Peru properties. In 2021, the Company concluded deals with Libero Copper and Gold, Patagonia Gold and most recently, AngloGold Ashanti.

Most recent news announced in June 2022:

“We are delighted to welcome AngloGold as an option partner. AngloGold Ashanti is the fourth largest gold producer globally, with operations across four continents,” said Keith Henderson, President and CEO of Latin Metals. “AngloGold’s investment of up to USD 12.575 million for a 75% ownership interest in the Projects is a significant investment, and, if AngloGold were to exercise its top-up right for an aggregate 80% ownership, additional investments by AngloGold would include delivery of a Mineral Resource estimate and further cash payments commensurate with defined ounces to Latin Metals.” (June 6/22 PR)

One can see the importance of the ‘Project Generator’ approach to property/asset acquisition.

You may well be thinking. Another Gold/Copper company? And you’d be right. However, LMS has excellent properties, a business approach to monetizing properties and impressive management. Over the last 52 weeks, the share price range doubled from CDN$0.08 to CDN$0.175. Shares are now CDN$0.10 a piece.

So whether as a straight copper/gold investment, a metals proxy or a growth play, Latin Metals is worth more research while drinking an excellent South American Dark Roast.

There’s more to come on this quality junior.

Marc has been involved in the Stock Market Media Industry for the last +4 years. After obtaining a college degree in engineering in France, he moved to Canada, where he created Money,eh?, a personal finance website. He then contributed to building Guerilla Capital, a Capital Markets company and FirstPhase Media where he was head of research. At10xAlerts, he writes articles and conducts interviews on many sectors, including technology, metals & mining markets.

-

Marc ZERBOLA CHALLANDEhttps://10xalerts.com/author/marcchallande/

-

Marc ZERBOLA CHALLANDEhttps://10xalerts.com/author/marcchallande/

-

Marc ZERBOLA CHALLANDEhttps://10xalerts.com/author/marcchallande/

-

Marc ZERBOLA CHALLANDEhttps://10xalerts.com/author/marcchallande/

All Articles

The latest

Gold Prices in 2024: A Robust Upward Trend

Canada’s GDP Experienced a Modest Increase of 0.2%

VistaGen Therapeutics (NASDAQ : VTGN) Analysis

Subscribe

©2024 10xAlerts